What 87740 Homes Cost Right Now, and Why Three Sources Disagree

A buyer checking three different portals for this zip code will see three different “median price” figures, and none of them is wrong. Redfin’s $174,895 median sale price reflects actual closed transactions reported through the MLS in May 2026. Zillow’s $140,894 estimate is a model applied across the entire housing stock, occupied or not, listed or not. The Census Bureau’s $134,300 figure comes from owners self-reporting what they think their home is worth in the 2020–2024 American Community Survey, a lagging, survey-based number that predates the most recent price movement.

For a buyer, the closed-sale figure matters most, since it reflects what people actually paid. For a seller pricing a listing, the $40,595 spread between the Redfin and Census figures is a reminder that an owner’s sense of value and a buyer’s demonstrated willingness to pay can diverge sharply in this market.

| Metric | Current value | Source | As of |

|---|---|---|---|

| Median sale price (closed transactions) | $174,895 (+6.8% YoY) | Redfin | May 2026 |

| Typical home value (model estimate) | $140,894 (−1.1% YoY) | Zillow | June 2026 |

| Median owner-occupied value (owner survey) | $134,300 | U.S. Census Bureau | 2020–2024 ACS |

| Median days on market | 164 days | Movoto | June 2026 |

Days on market ran more than double the roughly 50-to-77-day range reported for New Mexico statewide over the same period. Two variables specific to 87740 explain most of that gap: financed sales in this price range move slower because manufactured and older housing stock triggers extra underwriting steps, covered below, and acreage parcels routinely sit longer than in-town listings because they draw a smaller buyer pool. A listing priced near the Redfin median that is in-town, on a conventional foundation, and correctly disclosed tends to sell faster than the headline figure suggests; an acreage parcel priced above it can sit for six months or more without that signaling a pricing mistake. One more wrinkle worth checking before comparing inventory counts across sites: portals reference more than one MLS feed for this market, so a listing count or DOM figure on one site will not always match another for the same address.

How long do homes typically sit on the market in 87740?

A median of 164 days as of June 2026, more than double the New Mexico statewide median of roughly 50 to 77 days over the same period. In-town, conventionally financeable homes typically sell faster than that figure; acreage and manufactured-home parcels typically sell slower.

The Zip Code Isn’t One Market: Three Sub-Areas

A single citywide median treats a $95,000 in-town fixer and a $650,000 highway-frontage parcel as one market, and buyers who search only by zip code miss that these are functionally different products with different financing paths and different buyer pools.

Historic Downtown Core

Built mostly before 1950 – the citywide median construction year is 1959, per Census housing data referenced by Point2Homes’ rendering of the ACS figures – these are small-lot, walkable properties near the Amtrak depot and Shuler Theater. Active listings here range from roughly $80,000 for homes needing work to $250,000 for restored properties, based on the active-listing price spread Realtytrac reports for the zip code.

Edge-of-Town Residential and Small Acreage

One-to-five-acre parcels with utilities nearby but not always connected, priced from roughly $30,000 to $150,000 for land alone, based on the active land listings surveyed for this page.

Highway 72/87 Corridor

Larger acreage, 20 to 200-plus acres, mixing residential, ranch, and commercial-zoned parcels along the two highways feeding I-25. Several active listings in this corridor carry C-2 or C-3 commercial zoning rather than residential, which changes both financing and resale pool.

| Sub-area | Typical price range | Dominant property type | Best-suited buyer |

|---|---|---|---|

| Historic Downtown Core | $80,000 to $250,000 | Pre-1950 single-family, small lot | First-time buyer or owner-occupant wanting walkability |

| Edge-of-Town Residential/Acreage | $30,000 to $150,000 (land only) | 1 to 5-acre parcels, mixed utility access | Buyer wanting space without a full off-grid setup |

| Highway 72/87 Corridor | $30,000 to $1,100,000+ | 20+ acre land, ranch, mixed commercial zoning | Rancher, land investor, commercial developer |

The three ranges barely overlap, which is the concrete reason to ask a listing’s sub-area before comparing its price to the zip code’s median: a downtown price of $220,000 is expensive for that sub-area, while the same figure is inexpensive for a Highway 72/87 acreage parcel.

Which part of 87740 fits a first-time buyer vs. a rancher or investor?

A first-time or owner-occupant buyer is generally better served by the Historic Downtown Core, where lot sizes and financing paths are conventional. A rancher, land investor, or anyone planning acreage-based use fits the Highway 72/87 Corridor, where zoning and parcel size vary block to block and need to be checked individually with Colfax County.

Financing a Sub-$150,000, Rural, and Sometimes Manufactured Housing Stock

Roughly one in five housing units in Raton is a mobile or manufactured home – 19.7% of the city’s 3,375 housing units, per Point2Homes’ Census-derived housing breakdown – and the median owner-occupied home value citywide sits at $134,300. Both facts push a meaningful share of 87740 transactions into financing territory that a standard 20%-down conventional loan on a stick-built home doesn’t cover cleanly.

Two frictions recur. Several lenders apply practical minimum loan amounts in the $50,000-to-$75,000 range, so a $30,000-to-$45,000 house, common in the Downtown Core, often has to be a cash purchase or seller-financed rather than conventionally mortgaged, whatever the buyer’s credit looks like. Separately, a manufactured home only qualifies for a standard mortgage once its vehicle title has been deactivated by the Motor Vehicle Division and the county assessor has placed it on the tax roll as real property – a two-step process documented in the MVD’s manufactured-home titling chapter. A home still carrying an active MVD vehicle title, however permanently it sits on its foundation, remains legally personal property, financed with a chattel loan instead of a mortgage.

| Property type | Typical financing path | Main friction point |

|---|---|---|

| Site-built, in-town, over roughly $75,000 | Conventional or FHA mortgage | Standard; appraisal timing tracks the market’s slower days-on-market |

| Site-built, under roughly $50,000 | Cash or seller financing | Falls below many lenders’ practical minimum loan amount |

| Manufactured, retitled as real property | Conventional or FHA mortgage | Requires MVD title deactivation and county assessor real-property listing before closing |

| Manufactured, still on MVD vehicle title | Chattel (personal-property) loan | Higher rate, shorter term; ineligible for a standard mortgage until retitled |

Can I get a mortgage on a $30,000 house in this zip code?

Usually not through a standard mortgage lender, because most lenders set a practical minimum loan amount well above that price. Cash purchase or seller financing is the typical path for properties in that range.

Water Rights and Well Permits for Land Buyers

Any 87740 parcel outside city water service draws from a domestic well, and a standard New Mexico domestic well permit caps use at one acre-foot of water per year under state administrative rule 19.27.5.14 NMAC, unless the buyer separately acquires and transfers in additional water rights. That cap covers ordinary household use but can constrain irrigation, livestock watering, or a second dwelling on the same parcel, which matters directly for several Highway 72/87 Corridor listings marketed for exactly that kind of use. New Mexico’s Office of the State Engineer also lets a city deny a new domestic well application when a city water line runs within 300 feet of the property, per the New Mexico Groundwater Association’s summary of the state’s domestic-well framework, which matters for edge-of-town parcels that look rural but sit close to Raton’s service boundary.

A currently listed 3.8-acre parcel on Cherokee Hills Road off Highway 72, near Lake Maloya, is marketed as having utilities available, with no well or water right mentioned in the listing. That is the kind of gap a buyer needs to resolve with the county and the State Engineer’s office before assuming the land is build-ready.

The area’s coal-mining legacy adds a related, narrower check. Raton was once ringed by roughly eight coal mines employing more than 2,000 workers, an industry that wound down in the late 1990s, according to reporting on the town’s post-mining economic recovery. Land buyers on the Highway 72/87 Corridor or near former camp sites like Van Houten should confirm with Colfax County whether a parcel sits over historic underground workings, since old mine subsidence is a foundation and insurance question a general title search does not automatically surface.

Does buying land in Raton, NM involve water rights issues?

Often, for any parcel relying on a domestic well rather than city water. New Mexico’s standard domestic well permit caps use at one acre-foot per year, and buyers should confirm existing well permits and water rights with the county and the Office of the State Engineer before closing.

Wildfire Risk and Insurability

FEMA’s National Risk Index rates Colfax County’s overall natural-hazard risk as “Relatively Moderate” against the rest of the country, but rates the county’s community resilience, its capacity to prepare for and recover from a hazard event, as “Relatively Low.” For a buyer, that combination changes the insurance conversation: a moderate hazard score paired with low recovery capacity behaves differently underwriting-wise than a moderate score in a well-resourced county. Buyers on wooded or mesa-edge parcels, particularly toward Sugarite Canyon and Johnson Mesa, should get a homeowners-insurance quote before writing an offer, since wildland-urban-interface pricing and availability can shift a property’s real annual cost by thousands of dollars.

The Mechanics of Closing in New Mexico

New Mexico does not require an attorney at closing, and title insurance premiums are set statewide by the Superintendent of Insurance rather than shopped between companies, so switching title companies will not lower that line item. By local custom the seller pays for the owner’s title policy and the buyer pays for the lender’s policy, per a review of New Mexico’s closing-cost statute and practice, though either can be renegotiated in the purchase contract. New Mexico charges no state real-estate transfer tax.

Rental Yield for Investors: What the Census Numbers Support

Raton’s median gross rent is $741 a month citywide, per the Census Bureau’s 2020–2024 estimate, a single citywide figure rather than an 87740-specific or property-type-specific one, so any yield built on it is a starting range rather than a verified return. Paired against the Redfin median sale price of $174,895, a straightforward gross-yield calculation lands around 5.1% before taxes, insurance, and vacancy; paired against the lower Census-reported median value of $134,300, the same math produces roughly 6.6%. Neither number accounts for a specific property’s condition, financing cost, or achievable local rent, which an investor still has to verify directly.

| Price band | Estimated monthly rent | Estimated gross yield | Caveat |

|---|---|---|---|

| ~$134,300 (Census median value) | ~$741 (Census median gross rent) | ~6.6% | City-wide averages, not property-specific |

| ~$174,895 (Redfin median sale price) | ~$741 (Census median gross rent) | ~5.1% | Higher-priced homes don’t necessarily rent for proportionally more |

| Sub-$75,000 in-town fixer | Unverified locally | Not calculable from public data | Requires a local rent-roll comparison before underwriting |

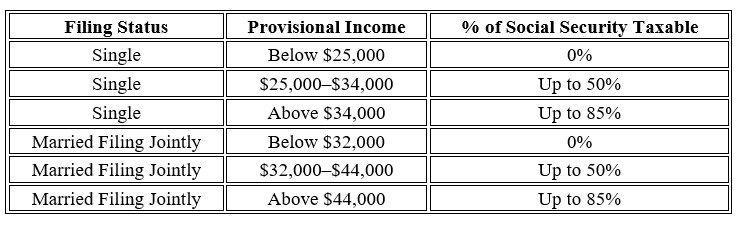

Is Raton’s “No State Income Tax” Retiree Pitch True?

For a retired couple whose income is mostly Social Security and stays under $150,000 combined, the practical effect is close to what the “no tax” pitch implies. For a higher-income retiree, or one relying heavily on pension or IRA income, it does not hold, and budgeting a retirement move in 87740 around the blanket version of the claim risks a real planning error.

Is Raton, NM tax-friendly for retirees?

For most retirees under the income thresholds, yes: Social Security is exempt below $100,000 (single) or $150,000 (joint) AGI. New Mexico still taxes pensions and IRA withdrawals, and levies a general state income tax, so it is not a blanket no-tax state.

Leave a Reply