Where in New York – City, Suburbs, or Upstate

Most guides answering “buy property in New York” quietly mean Manhattan. The tax code doesn’t.

| New York City | Westchester / Long Island | Upstate NY | |

|---|---|---|---|

| Mansion tax | 1% to 3.9%, progressive above $2M | Flat 1% at $1M+ | Flat 1% at $1M+ |

| Dominant property type | Co-op, roughly 70% to 75% of stock per market reports | Single-family, some condo | Single-family |

| Co-op board approval | Common, often decisive | Rare | Rare |

| Recent median price | $1.4M, Manhattan, three months to May 2026 (Redfin) | $750K, Westchester County, March 2026 (Redfin) | No single county benchmark |

A $5M purchase in Manhattan owes $112,500 in mansion tax at the 2.25% tier. The identical price in Westchester owes $50,000 at the flat 1% rate. The gap comes from the tax structure itself, not from a difference in home value.

Can You Legally Buy, and Is Any Land Off-Limits?

No New York State law currently restricts foreign ownership of residential real estate. Three bills addressing foreign land ownership sit in the Assembly Judiciary Committee as of early 2026, A3440 and A6154, both targeting agricultural and industrial-zoned land only, plus A1452, broader in scope. None has passed, and none of the pending bills would touch a residential condo, co-op, or house purchase even if enacted.

Do I need a visa or green card to buy property in New York? No. Property ownership in the US carries no citizenship or immigration requirement. Financing, tax withholding, and, for co-ops, board approval are separate questions with their own rules, covered below.

Condo or Co-op: What You Can Actually Get Approved For

Condos transfer by deed. Co-ops sell shares in a corporation plus a proprietary lease, and roughly 70% to 75% of NYC’s owned housing stock is co-op, concentrated in Manhattan’s older buildings. That share matters because co-op boards routinely reject the exact profile many foreign buyers present.

| Factor | Condo | Co-op |

|---|---|---|

| Legal ownership | Real property, deed at closing | Shares plus proprietary lease |

| Board approval | None | Required, can take 30 to 90 days |

| Foreign-buyer approval odds | High | Low to moderate, building-dependent |

| LLC or entity ownership | Generally allowed | Frequently barred by bylaws |

| Financing flexibility | Wide range of lenders | Narrower; many boards cap financed share |

Common co-op rejection triggers for foreign applicants: no US-based income a board can verify against its debt-to-income floor, often 25% to 30%; ownership proposed through an LLC or trust the bylaws don’t permit; and reluctance to disclose full net worth on the REBNY financial statement co-op boards require. None of this is discriminatory under fair-housing law. Boards can reject for almost any non-protected reason, and financial opacity is the most common one.

Can I buy with an LLC, and will a co-op allow it? Condos generally permit LLC ownership without issue. Co-ops frequently prohibit it in the proprietary lease or house rules; some allow it only with a personal guarantee from a natural person, which undercuts much of the liability-shielding purpose of the LLC in the first place.

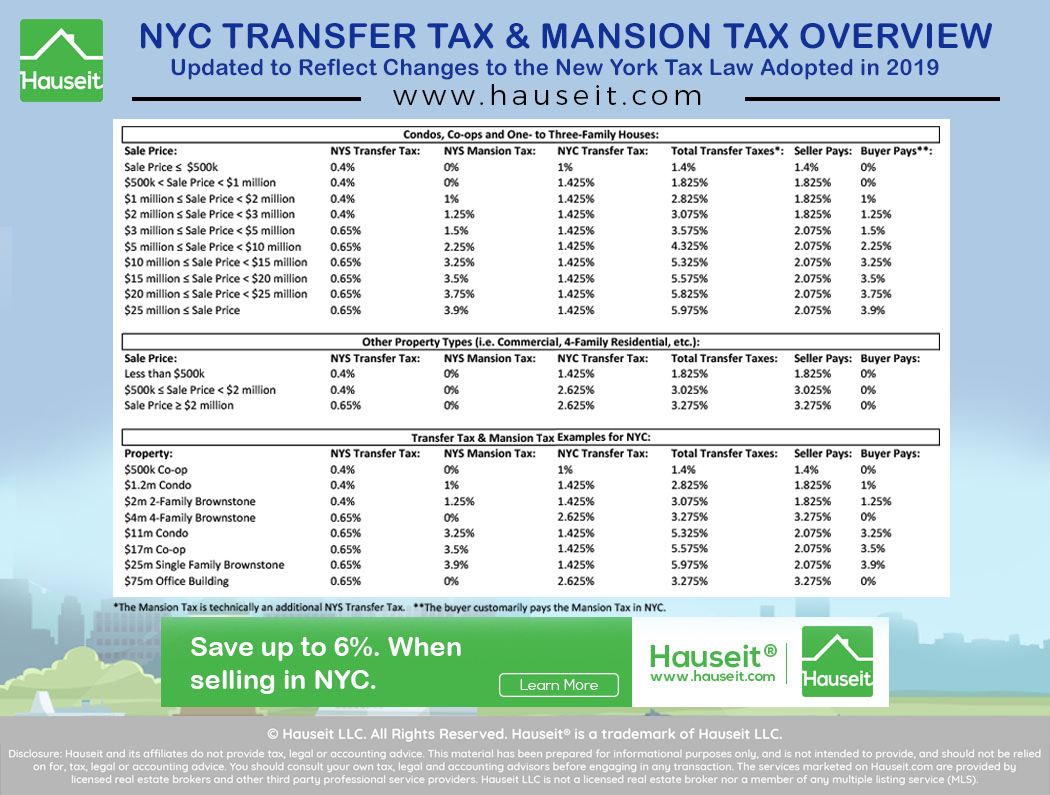

What It Costs to Close

The mansion tax applies to the entire purchase price once you cross a threshold, not just the amount above it. A $1,999,999 sale owes 1% on the full price; add one dollar and the whole price is taxed at 1.25%.

| Purchase price, NYC | Mansion tax rate | Tax at that tier’s top |

|---|---|---|

| $1,000,000 to $1,999,999 | 1.0% | $19,999 |

| $2,000,000 to $2,999,999 | 1.25% | $37,499 |

| $3,000,000 to $4,999,999 | 1.5% | $74,999 |

| $5,000,000 to $9,999,999 | 2.25% | $224,999 |

| $10,000,000 to $14,999,999 | 2.5% | $374,999 |

| $15,000,000 to $19,999,999 | 2.75% | $549,999 |

| $20,000,000 to $24,999,999 | 3.0% | $749,999 |

| $25,000,000 and above | 3.9% | Uncapped |

Outside NYC, every tier collapses to a flat 1%, with no upper bracket at all. The mechanism is set out by the NYS Department of Taxation and Finance; the tier amounts above are compiled from current 2026 closing-cost calculators including Hauseit.

A co-op wrinkle catches buyers under the $1M line off guard: the taxable price for mansion-tax purposes includes your proportional share of the building’s underlying mortgage, not just what you pay the seller. A co-op priced at $950,000 with $80,000 of allocated underlying debt has a taxable price of $1,030,000. The tax applies even though the negotiated price looks safely under the threshold.

Financing vs. Cash – What Foreign Buyers Qualify For

A foreign national with no US credit history and no US residency status typically needs 25% to 40% down for a specialist foreign-national mortgage program; a handful of programs go as low as 20% with strong reserves, and pure cash purchases remain common. Nationally, 47% of foreign buyers paid entirely in cash in the most recent full year of data, against 28% of the general US buyer population, and the median foreign-buyer purchase price reached $494,400, above the $408,500 median for all US buyers. These figures come from the National Association of Realtors’ 2025 International Transactions Report as cited in America Mortgages’ 2026 handbook, the most complete current compilation found for this topic. Green Card holders and valid work-visa holders qualify for standard conventional programs with down payments as low as 3% to 3.5%, since lenders classify them differently from non-resident foreign nationals.

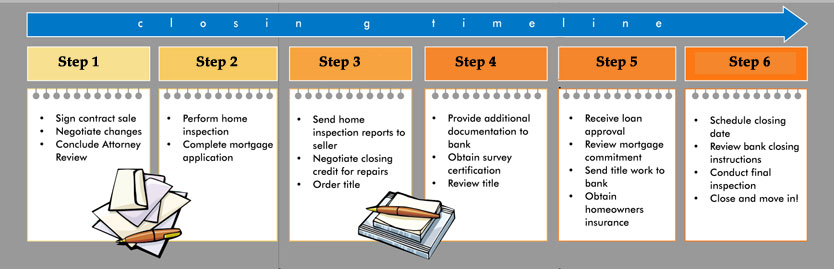

The Realistic Timeline

No single published source lines up cash, financed, and co-op timelines side by side; the ranges below are synthesized from the process stages described in the sections above.

| Stage | Cash condo | Financed condo | Co-op, cash or financed |

|---|---|---|---|

| Offer to signed contract | 1 to 2 weeks | 1 to 2 weeks | 1 to 2 weeks |

| Due diligence, title search | 2 to 3 weeks | 2 to 4 weeks | 2 to 3 weeks |

| Loan underwriting | n/a | 4 to 6 weeks | 4 to 6 weeks if financed |

| Board approval | n/a | n/a | 4 to 12 weeks |

| Total to closing | 4 to 6 weeks | 8 to 12 weeks | 12 to 20 weeks |

The co-op column is the one most guides compress into a single line about board approval taking time. The spread above is wide enough to change whether a co-op purchase fits a relocation deadline at all.

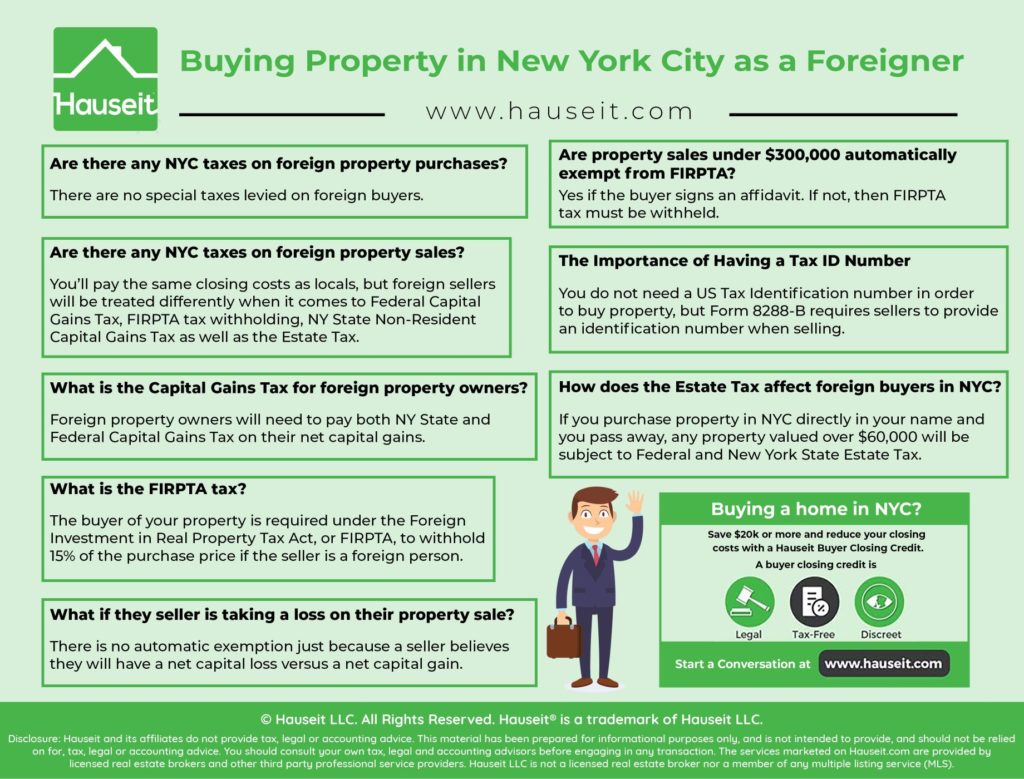

What Happens After You Own – FIRPTA, Gains, and Estate Exposure

Buying triggers no FIRPTA obligation for you as the purchaser. FIRPTA applies only when you later sell: the buyer of your property must withhold 15% of the gross sale price and send it to the IRS within 20 days, dropping to 10% on sales between $300,000 and $1,000,000 where the buyer will use it as a residence, and to zero below $300,000 under the same condition, per the IRS’s FIRPTA withholding page and its exceptions page.

Is FIRPTA a tax I pay when I buy? No. FIRPTA withholding is triggered on the sale, and it’s the buyer’s obligation to withhold, not the seller’s obligation to pay upfront. As a purchaser today, FIRPTA is a future-sale mechanic to plan around, not a closing cost.

Estate exposure is where the numbers get severe and rarely get explained in practical terms. A non-domiciled foreign owner gets a $60,000 US estate tax exemption on US-situated assets, a figure set in 1976 and never adjusted for inflation, against a $15,000,000 exemption for US citizens and domiciled residents starting January 1, 2026, per the IRS’s estate-tax-for-nonresidents page. Above that $60,000 line, rates run up to 40% of the property’s full fair market value, and the estate can’t transfer clear title until the US estate tax return, Form 706-NA, is resolved. Heirs in multiple countries can face a genuine delay before the property is theirs to sell or occupy. About 15 countries have estate tax treaties with the US that can raise the exemption; absent one, direct personal ownership is the highest-exposure structure available.

What happens to my property if I die owning it directly? The estate owes US tax on the value above $60,000, at rates up to 40%, and an executor must file Form 706-NA within nine months before heirs can clear title. Ownership through a trust or foreign corporation changes this exposure enough that it deserves its own conversation with a cross-border estate planner before you close, not after.

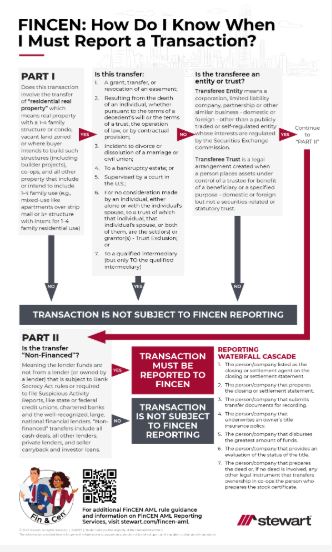

Reporting Rules for Cash and LLC Purchases

If you buy in cash through an LLC or trust, a federal reporting rule may or may not apply to your closing right now, and the answer has changed twice in 2026. FinCEN’s Residential Real Estate Rule took effect March 1, 2026, requiring title companies to report the beneficial owners behind non-financed entity or trust purchases.

On March 19, 2026, a federal court in the Eastern District of Texas vacated the rule nationwide in Flowers Title Companies, LLC v. Bessent. FinCEN’s own reporting-rule page currently states that reporting persons are not required to file while that order stands, and FinCEN has appealed to the Fifth Circuit, per FinCEN.gov.

Do I have to report large wire transfers to the US government? Banks already file currency and suspicious-activity reports on large wires under existing anti-money-laundering rules, regardless of the FinCEN real estate rule’s status. The real estate-specific beneficial-ownership report is the piece currently unenforceable; a closing attorney can confirm the live status at contract, since an appellate stay could reinstate it without notice.

Where the Common Advice Breaks Down

- “Cash is always simpler” ignores the compliance layer. An all-cash LLC purchase is precisely the transaction type the currently vacated FinCEN rule targets, simpler at the closing table but not necessarily simpler on the paperwork if the rule is reinstated mid-transaction.

- “Under $1M avoids the mansion tax” fails for co-ops with underlying debt, as the share-of-mortgage add-back described above can push a nominally sub-threshold co-op over the line.

- “An LLC protects you the same way everywhere” fails inside most co-op buildings. Board bylaws frequently require a personal guarantor, which unwinds the liability shield the LLC exists to provide.

- “Board approval just takes a few weeks” undercounts the real range, which runs 4 to 12 weeks and can sink a purchase timed to a visa or lease expiration.

Leave a Reply