Why one Brooklyn number can’t answer your question

Every borough-wide figure blends co-ops, condos, and houses, which PropertyShark’s own segmentation shows trading $760,000 apart at the median. Layer in neighborhood, and the range widens further.

| Segment | Median price | Source, date |

|---|---|---|

| Brooklyn, all sale types | $915,000 | PropertyShark, May 2026 |

| Brooklyn houses | $960,000 | PropertyShark, May 2026 |

| Brooklyn condos | $1,200,000 | PropertyShark, May 2026 |

| Brooklyn co-ops | $442,000 | PropertyShark, May 2026 |

| Brooklyn Heights | approx. $1,700,000 | Robert DeFalco Realty, 2026 |

| Downtown Brooklyn (asking) | approx. $1,150,000 | Robert DeFalco Realty, 2026 |

| Zip 11229 (Sheepshead Bay / Gerritsen Beach) | $750,000 | Robert DeFalco Realty, Nov. 2025 |

The gap between a $442,000 co-op median and a $1.2 million condo median isn’t a rounding difference. It reflects two different products with different financing rules, covered in the next section.

Reusing a citywide or upstate figure as if it describes Brooklyn specifically is a common and avoidable mistake, and so is reusing a rent or sale figure from 2022 as if it still holds in a market that has moved since.

Is Brooklyn currently a buyer’s market or a seller’s market? Neither cleanly. Howard Hanna’s Brooklyn Leverage Index, which blends supply, demand, price per square foot, and listing discounts, moved only modestly toward buyer territory in March 2026, even as price per square foot rose 13.4% year over year to $1,074. Supply and discounts favor buyers; price momentum favors sellers. Treat a flat “buyer’s market” claim with no data behind it skeptically.

Co-op, condo, or townhouse: what actually changes

Roughly one in four purchase agreements in this market is for shares in a corporation, not a deed. That distinction changes financing, approval speed, and resale flexibility.

| Dimension | Co-op | Condo | Townhouse |

|---|---|---|---|

| Typical down payment | 20% minimum, commonly 25% to 30%, some boards 40%+ or cash-only | 10% possible, 20% common to avoid PMI | 20% typical for best terms |

| Approval | Full board review and interview; may reject for any lawful reason | Board holds mainly a right of first refusal | No board |

| Target debt-to-income | Often 25% to 35% of gross income, building-specific | Standard conventional mortgage underwriting | Standard conventional mortgage underwriting |

| Closing-cost note | No title insurance or mortgage recording tax; flip tax of 2% to 3% common at resale | Title insurance plus mortgage recording tax (1.8% to 1.925% of loan amount) | Same deed-transfer costs as a condo |

| Resale friction | Subletting often restricted; buyer needs board approval too | Fewer restrictions on renting or resale | Fewest restrictions |

If your plan involves renting the unit out within a few years, a co-op board’s subletting rules can make that plan unworkable regardless of what a lender approves.

What’s the real difference between buying a co-op and a condo in Brooklyn? A condo purchase transfers a deed and is judged mainly by your lender. A co-op purchase transfers shares in a corporation and is judged separately by a board, which can reject an applicant without giving a reason.

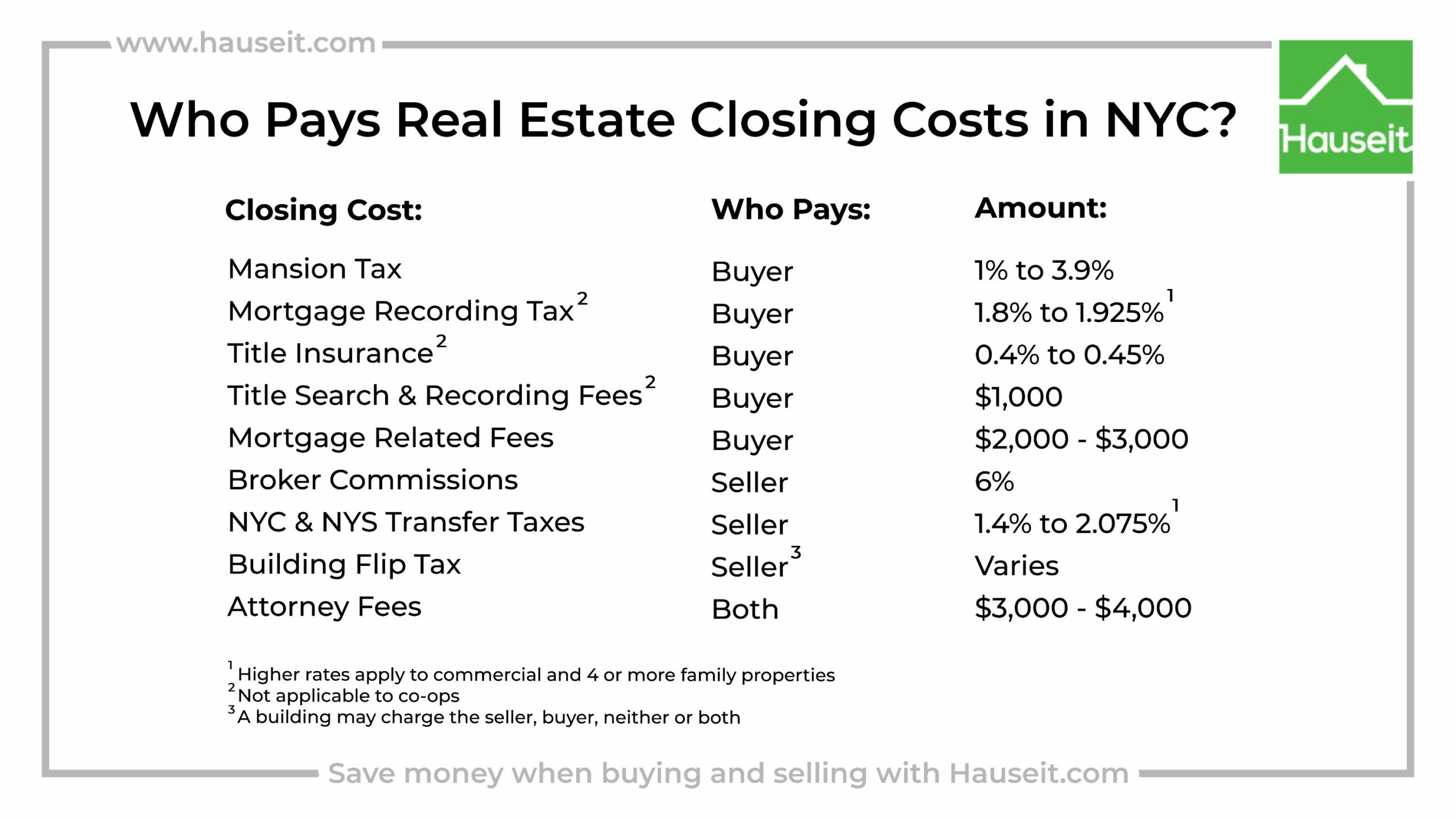

What a purchase or sale costs beyond the price tag

None of the four cost layers below shows up in a listing price, and all four apply in Brooklyn.

| Cost | Who pays | Rate or threshold | Source |

|---|---|---|---|

| NYS mansion tax | Buyer | 1% at $1,000,000, rising in tiers to 3.9% at $25,000,000+ | NYS Dept. of Taxation and Finance |

| NYC RPTT | Seller | 1.0% under $500,000; 1.425% at or above | NYS Dept. of Taxation and Finance |

| NYS base transfer tax | Seller | 0.4% under $3,000,000 | NYS Dept. of Taxation and Finance |

| NYC mortgage recording tax | Buyer, if financing | 1.8% under $500,000; 1.925% at or above, on loan amount | Avenue Law Firm |

| NYC property tax, Class 1 (1–3 family) | Owner, annually | 19.8% to 20.6% of assessed value; assessed value is 6% of market value | NYC Department of Finance |

| NYC property tax, Class 2 (condo, co-op) | Owner, annually | 12.3% to 12.4% of assessed value; assessed value is 45% of an income-based estimate | NYC Department of Finance; worked example, StreetEasy Blog |

A $1.4 million Brooklyn purchase crossing the mansion-tax line owes $14,000 in buyer-side tax alone, per a worked example a mortgage-data site published in May 2026. Add the seller’s transfer-tax obligations on the same deal and the combined closing-day tax burden runs to roughly $39,550, before title insurance, broker fees, or a mortgage recording tax if the buyer finances.

Because Class 2 condos and co-ops are assessed as if they were rental buildings, rather than valued off actual sale prices, the effective property-tax rate on a mid-market Brooklyn condo often lands closer to 1% of market value than the headline 12% rate suggests. A $1.2 million Brooklyn house doesn’t get that same cushion. It pays close to its full 20% rate on a 6% assessed base, landing in a similar effective range but arriving there by a completely different calculation.

Do I pay the mansion tax if I buy in Brooklyn? Yes, on any residential purchase of $1,000,000 or more, condo, co-op, or house alike. The buyer owes it, the rate applies to the full price rather than the amount above the threshold, and it climbs in eight tiers up to 3.9% at $25 million and above.

Buying as an investor: multifamily financing and yield math

Investors buying 2 to 4 unit Brooklyn buildings increasingly use DSCR loans, which qualify the loan against the property’s rental income rather than the borrower’s tax returns. Current DSCR pricing sits at 5.80% to 8.50% as of early July 2026, per PeerSense’s market note, against a Freddie Mac 30-year conventional benchmark of 6.43% for the week of July 2, 2026, per the Freddie Mac Primary Mortgage Market Survey. Typical DSCR terms run 20% to 25% down, with lenders generally wanting the property’s rent to cover its debt service at a ratio of 1.0 or higher, and 1.25 or higher for the best pricing. Unlike conventional financing, which caps most borrowers at 6 to 10 financed properties, DSCR loans carry no such limit, the main reason investors scaling past a first or second Brooklyn rental switch to them.

One limitation worth knowing before you shop for a multifamily deal: DSCR lenders generally will not finance co-ops at all. Condos, 1 to 4 family homes, and small multifamily buildings qualify; shares in a co-op corporation typically don’t. If your investment plan depends on rental income, a co-op board’s subletting restrictions and DSCR ineligibility together rule the category out for most buy-and-hold investors, regardless of price.

Buying as a foreign national

No federal or New York law requires citizenship, a visa, or residency status to buy real estate in Brooklyn. Foreign nationals can hold title to a condo, co-op, or house without immigration consequences. The mechanics that do apply arrive on sale, not purchase.

Under the Foreign Investment in Real Property Tax Act, a buyer purchasing from a foreign seller must generally withhold 15% of the amount realized and remit it to the IRS on Form 8288 within 20 days of the transfer. A reduced 10% rate can apply when the buyer intends to occupy a property sold for $1 million or less as a residence, and no withholding is required at all on a $300,000-or-under residence purchase. The buyer, not the seller, carries the withholding obligation and the personal liability if it’s missed.

Can a foreign national buy a house in Brooklyn? Yes, without a citizenship, visa, or residency requirement. FIRPTA withholding becomes relevant only when that buyer later sells, and only if the seller at that point qualifies as a foreign person for U.S. tax purposes.

Reading the current market: days on market by segment

A single citywide days-on-market figure, 68 days for 2025, hides how sharply that number splits by price tier and property type. Robert DeFalco Realty’s Spring 2026 report breaks it down for Brooklyn specifically.

| Segment | Typical days on market | Source |

|---|---|---|

| Single-family homes under $1M, southern Brooklyn | 18 to 28 days | DeFalco Realty, Spring 2026 |

| Mid-tier condos, $900K to $1.4M | 60 to 75 days | DeFalco Realty, Spring 2026 |

| Co-ops above $700K | 90+ days, some premium buildings 120+ | DeFalco Realty, Spring 2026 |

| Brownstones, realistically priced | 30 to 45 days | DeFalco Realty, Spring 2026 |

| Brownstones, aspirationally priced | 100+ days | DeFalco Realty, Spring 2026 |

Southern Brooklyn’s under-$1M single-family segment sells fundamentally faster than a premium co-op, and no borough-wide average communicates that.

How fast these numbers go stale

Every price, tax rate, and days-on-market figure above carries a publication date because Brooklyn’s market moves month to month, and property-tax rates are set annually by the City Council. Treat the figures here as a July 2026 snapshot, not a permanent reference, and confirm current rates against the NYC Department of Finance and NYS Department of Taxation and Finance before closing.

Leave a Reply