Washington’s Housing Market by County Right Now

Home prices in Washington vary more by county than a single statewide figure suggests. King County leads the state, with Snohomish close behind. Spokane County, on the state’s east side, runs roughly half the King County figure, and Pierce County sits between the two.

That spread is the first thing a state assistance program has to clear before it means anything to a specific buyer, and the next section works through exactly where that line falls.

What Financing Requires

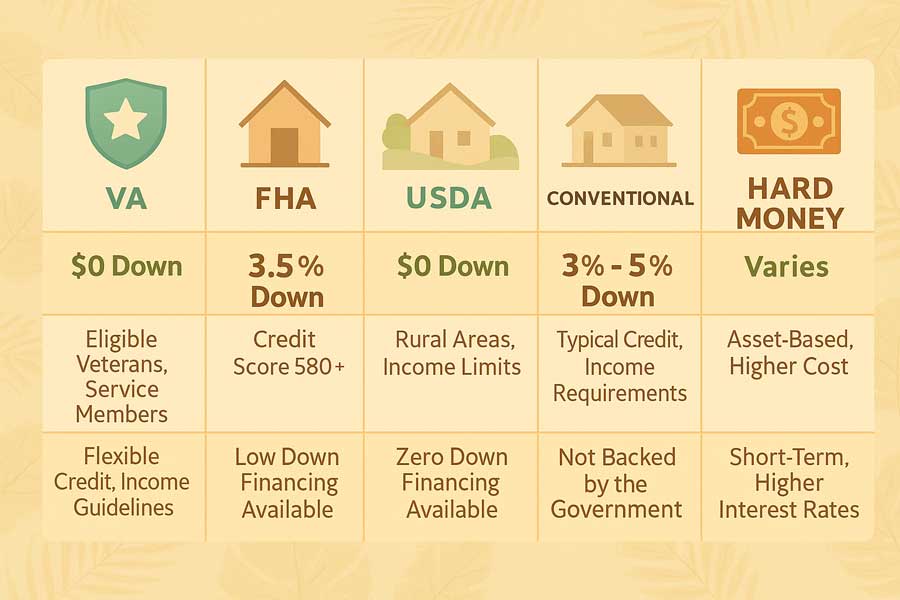

Three federal loan types cover most Washington purchases, and each sets a different floor for down payment and credit before any state assistance layers on top.

| Loan type | Minimum down payment | Minimum credit score | 2026 loan limit, King/Pierce/Snohomish |

|---|---|---|---|

| FHA | 3.5% | 580 | $1,063,750 |

| Conventional conforming | As low as 3% for qualifying first-time buyers | Set by lender, commonly 620 or higher | $1,063,750 |

| VA (full entitlement) | 0% | Set by lender | No VA-imposed limit since 2020 |

The 2026 limit for King, Pierce, and Snohomish counties is $1,063,750, per LendingTree’s loan-limit data, roughly double the national floor of $541,287 that applies to most other Washington counties, including Spokane. That gap exists because these three counties share a single high-cost metro designation; it isn’t a separate application, it’s a formula the lender applies once they know the property’s county.

Washington’s Assistance Programs, County by County

Washington’s primary state assistance vehicle runs through the Washington State Housing Finance Commission, working through two first-mortgage programs, Home Advantage and House Key Opportunity, plus a Down Payment Assistance second mortgage layered on top. The DPA is a deferred, zero percent second loan, typically 3% to 5% of the first mortgage amount, repaid only when the home is sold, refinanced, or paid off. None of that matters until the purchase price clears the program’s cap for the buyer’s county, and that’s where most coverage of this topic stops short.

WSHFC raised its House Key Opportunity acquisition cost limits effective September 15, 2025, with the increase applied unevenly by county:

| County group | Non-target area cap | Target area cap | Current county median | Program reaches the median? |

|---|---|---|---|---|

| King, Pierce, Snohomish | $725,000 | $775,000 | King $887,000 / Pierce $564,000 / Snohomish $758,000 | No for King; yes for Pierce; borderline for Snohomish |

| Whatcom | $600,000 | $675,000 | Not sourced for this page | Verify locally |

| Clark, Island, Kitsap, Skagit, Skamania, Thurston | $550,000 | $625,000 | Not sourced for this page | Verify locally |

| All other counties, including Spokane | $500,000 | $550,000 | Spokane $429,000 | Yes, comfortably |

Pierce and Spokane buyers get a program that covers their county’s typical purchase. A King County buyer targeting the median needs roughly $112,000 to $162,000 of purchase price above what the program supports, pushing that buyer toward FHA, conventional, or VA financing without the state DPA layered in, unless they’re buying below median in a lower-cost pocket of the county.

One eligibility detail gets buried in most program pages: “first-time buyer” under WSHFC’s rules doesn’t mean never owned a home. It means not having owned and occupied a home in the past three years, so a previous owner who sold or lost a home more than three years ago still qualifies.

Will WSHFC assistance actually help me buy in King County? For a home at or near the King County median of $887,000, the House Key Opportunity cap of $725,000 to $775,000 falls short. The program is a stronger fit for South King County, Auburn, Federal Way, or a condo or townhome purchase below the cap.

Finding an Agent Under the New Agency Law

Washington’s real estate agency law, RCW 18.86, changed on January 1, 2024, under Senate Bill 5191, as summarized by Stokes Lawrence. Before that date, brokerages only needed a written agreement with the seller; a buyer could tour homes with an agent on a handshake. Since then, a broker must enter into a written brokerage services agreement with a buyer before, or as soon as reasonably practical after, starting to provide real estate brokerage services, and that agreement carries a 60-day default term unless the parties agree otherwise.

That interacts directly with a second, older concept many buyers have never had explained alongside it: limited dual agency, where one broker or firm represents both sides of the same transaction. The 2024 revision didn’t create dual agency, it tightened consent around it. A buyer must specifically consent, in writing, to a broker acting in that limited capacity, and separately to that broker’s managing broker doing the same. If you’re signing a services agreement anyway, that’s the moment to read the dual agency clause instead of skipping to the signature line.

Does Washington require a signed agreement before my agent shows me homes? Yes, since January 1, 2024. A broker must have a written brokerage services agreement in place before, or as soon as reasonably practical after, beginning to provide services such as touring homes.

Making a Competitive Offer

An escalation clause lets a buyer’s offer rise automatically above a competing bid up to a stated ceiling, and appraisal gap coverage commits the buyer to pay some or all of the difference if the home appraises below the contract price. Both are negotiated per offer, not set by any statewide formula, so the right numbers depend on your lender, your cash reserves, and how many other offers are on the table that week.

What Closing Costs, and Who Pays for It

Washington’s Real Estate Excise Tax is a seller-paid state tax on the sale price, using a graduated structure set by the Washington State Department of Revenue.

| Portion of sale price | State REET rate |

|---|---|

| Up to $525,000 | 1.10% |

| $525,001 to $1,525,000 | 1.28% |

| $1,525,001 to $3,025,000 | 2.75% |

| Above $3,025,000 | 3.00% |

Most cities and counties add a local REET of 0.25% to 0.50% on top of the state rate, and the seller is responsible for the combined total at closing. This is the tax that confuses buyers who see “real estate excise tax” on a closing statement and wonder why they’re not the one paying it: they aren’t, unless the purchase agreement specifically shifts it. Buyer-side closing costs run separately: loan origination and underwriting fees, appraisal, title insurance, and escrow fees, all negotiated with the lender and title company rather than set by the state.

Who pays closing costs in Washington? Sellers pay the state and local Real Estate Excise Tax. Buyers separately cover their own loan, appraisal, title, and escrow fees, negotiated individually rather than fixed by any single formula.

Inspections Worth Paying For in an Older Home

Washington sits along the Cascadia Subduction Zone, and homes built before roughly 1980 often lack the foundation bolting and cripple wall bracing that later codes require. Two retrofits cover most of that gap:

- Foundation bolting anchors the wood sill plate to the concrete foundation with steel bolts, typically running $1,000 to $5,000.

- Cripple wall bracing reinforces the short wood-framed wall between the foundation and the first floor with structural plywood, typically running $1,000 to $3,000.

During the 2001 Nisqually earthquake, a magnitude 6.8 event, homes that slid even a few inches off an unbolted foundation saw structural damage exceeding $100,000, according to a Washington insurance broker’s retrofit cost breakdown. A pre-purchase inspection that flags an unbolted, pre-1980 foundation is pointing at a five-figure gap between what a retrofit costs and what skipping it can cost later.

Do I need earthquake insurance in Washington? It’s optional and separate from a standard homeowners policy, and most insurers require a completed seismic retrofit before they’ll write a policy on an older home.

Sewer scope inspections and moisture assessments matter too, particularly for homes on older municipal sewer lines or in wetter western Washington microclimates, though this page didn’t find sourced, dated cost figures for those specific inspections strong enough to publish as fact.

Leave a Reply