Neighborhood prices, flood zones, and who each one fits

Every figure below is a Redfin-reported, MLS-derived median for its own neighborhood boundary, not a citywide average stretched across a name.

| Neighborhood | Median price (2026) | FEMA flood zone | STR posture | Best fit |

|---|---|---|---|---|

| Historic Old Northeast | $825,000 | Mixed: waterfront blocks AE, inland/ridge blocks X | Mostly RS/RT, STR not allowed by right | Families, walkable-lifestyle buyers |

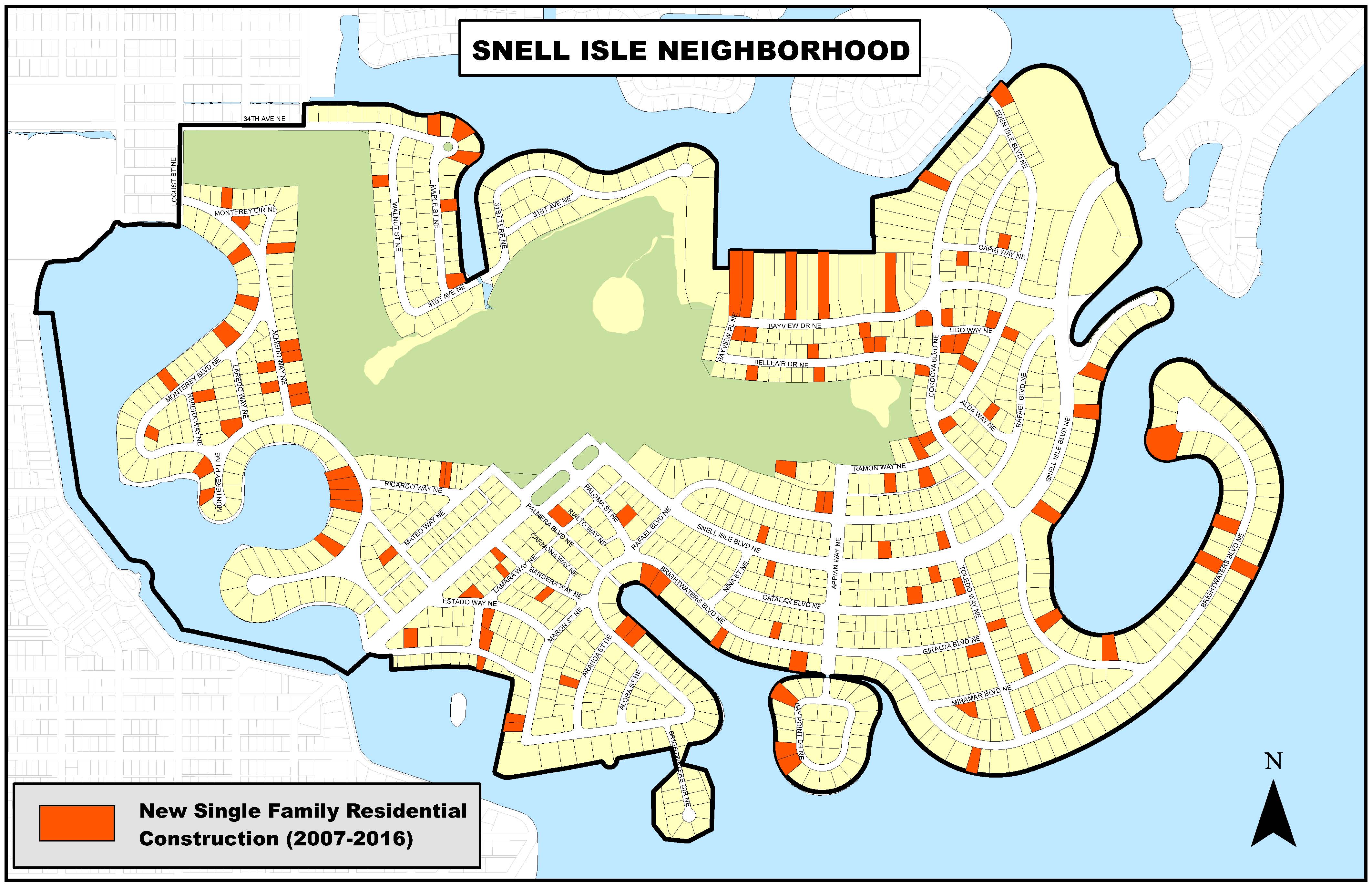

| Snell Isle | $1.5M | Mostly AE; some VE-adjacent canal lots | RS, STR not allowed by right | Waterfront/boating buyers, cash-heavy purchasers |

| Historic Kenwood | $563,000 | Largely X (inland ridge) | Mostly RS/RT, some NT pockets with conditional owner-occupied STR | First-time buyers, value-and-character buyers |

| Coquina Key | $472,000 | AE (tidal outfalls per city drainage study) | Mostly RS/RT, STR not allowed by right | Budget waterfront access, boat owners |

| Downtown St. Petersburg | $1.7M median (luxury-tower-skewed); resale condos more commonly $425,000 to $575,000 | Mixed, mostly AE near the waterfront | DC/CG, STR generally allowed | Investors, lock-and-leave buyers |

Sources: Old Northeast, Snell Isle, Kenwood, Coquina Key, Downtown (Redfin); flood zones from Pinellas County and the city’s 2023 Repetitive Loss Area Analysis.

The Downtown figure needs a flag: its three-month median is inflated by a handful of luxury-tower closings, so resale condo shoppers should anchor to the $425,000 to $575,000 resale range instead of the headline number. Kenwood sits furthest from flood exposure of the five and carries the lightest insurance load as a result; Snell Isle and Coquina Key carry the most.

Is St. Petersburg in a flood zone? Parts of it, unevenly, and the map moves at the block level, not the neighborhood level. Homeowners who believe a FEMA letter is wrong for their specific parcel can request a Letter of Map Amendment, which can shift a property out of a mapped high-risk zone and lower its insurance requirement, so a neighborhood-wide answer is always a starting point, not a final one.

The real cost of coastal ownership

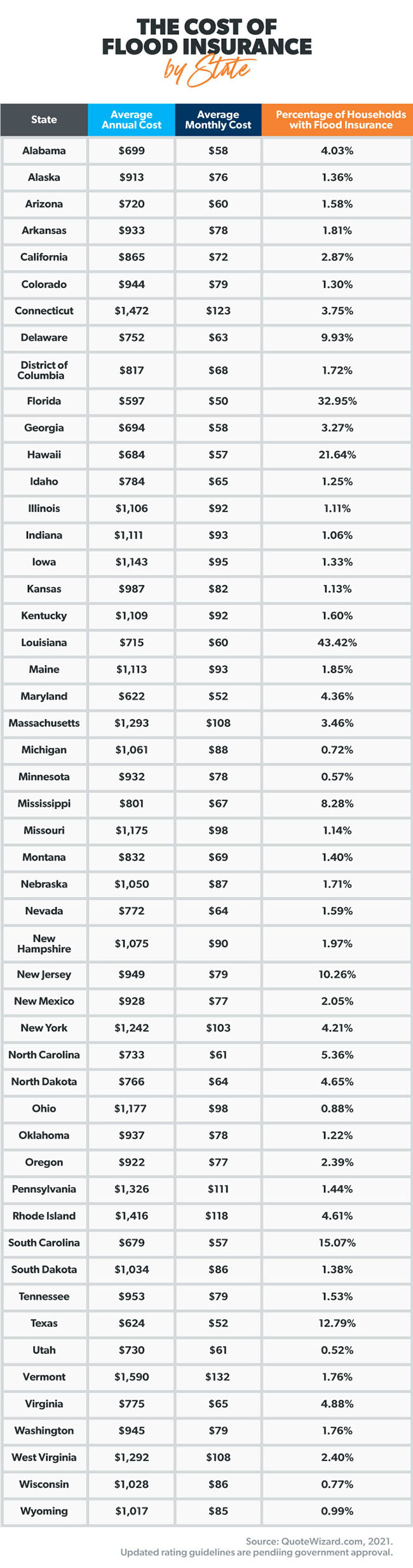

Flood insurance in Florida costs anywhere from $400 to $1,200 a year in a minimal-risk Zone X property, $2,000 to $10,000 in an AE zone, and $5,000 to $20,000-plus for VE-zone barrier-island frontage (Harbour Insurance Agency). Pinellas County’s flood-management practices earn it FEMA’s second-highest Community Rating System class, which knocks 40% off standard NFIP premiums countywide (NerdWallet, citing FEMA data).

Remodeling inside AE or VE zones runs into a stricter local trigger than most buyers expect, and it’s worth stating once, plainly: FEMA’s standard substantial-improvement threshold is 50% of a home’s value before full elevation compliance kicks in, but the City of St. Petersburg caps it tighter, at 49% (City of St. Petersburg). One extra point of renovation budget is the difference between a standard remodel and a full elevation project.

Buying resets the property’s assessed value to full market value the year after closing, whatever the seller’s own tax bill showed while they held homestead protection. This is the county appraiser’s office’s own account of its most common buyer complaint: online listings display the seller’s tax bill, buyers budget against it, and the actual bill the following year can run double or triple that figure once the prior owner’s Save Our Homes cap disappears (Pinellas County Property Appraiser). Once a buyer files for and qualifies for homestead exemption, 2026’s benefit is $51,411 off assessed value: the first $25,000 applies to all levies, and up to $26,411 more applies to non-school levies on value between $50,000 and $75,000. Future assessment growth then caps at 3% a year or the Consumer Price Index, whichever is lower, 2.9% for the 2025 cycle (Pinellas County Property Appraiser, Save Our Homes). Sellers moving within Florida can port up to $500,000 of accumulated Save Our Homes benefit to a new homestead within three tax years (Portability).

| Cost type | Typical range | Who’s affected | Source |

|---|---|---|---|

| Flood insurance, Zone X | $400 to $1,200/yr | Inland Kenwood, Crescent Lake buyers | Harbour Insurance Agency |

| Flood insurance, Zone AE | $2,000 to $10,000/yr | Snell Isle, Coquina Key, waterfront Old Northeast | Harbour Insurance Agency |

| Flood insurance, Zone VE | $5,000 to $20,000+/yr | Barrier-island and open-bay frontage | Harbour Insurance Agency |

| Homestead exemption (2026) | Up to $51,411 off assessed value | Owner-occupants filing by March 1 | Pinellas County Property Appraiser |

| Post-sale assessment reset | Assessed value jumps to full market value the year after purchase | All buyers of previously homesteaded property | Pinellas County Property Appraiser |

The gap between what a listing implies about carrying costs and what a new owner actually pays is real, specific, and worth pricing before writing an offer rather than after closing.

Do I need flood insurance if I’m not directly on the water? Possibly, and it’s worth pricing regardless. Zone X properties aren’t required to carry it for a federally backed mortgage, but roughly one in five NFIP claims nationally comes from moderate- or low-risk zones, and inland streets a few blocks from Zone AE can still sit inside a “shaded X” 500-year floodplain where lenders often recommend coverage anyway.

Renting it out: short-term rental rules by zone

St. Petersburg regulates rentals under 30 days by zoning district, not citywide. Downtown Center and Commercial General zones allow them by right; Residential Suburban and Residential Traditional zones do not, defaulting to a 30-day minimum stay instead. Owner-occupied properties in Neighborhood Traditional and Neighborhood Established zones get more flexibility and can qualify for STR permits where a non-owner-occupied investment property in the same zone would not; some residential parcels also carry a narrower exception allowing up to three short stays in any 12-month period (strprofitmap.com; hometeamluxuryrentals.com; stayvello.com). Compiled guides disagree on the edge cases, so verify any specific parcel against the official Municode ordinance text before underwriting a purchase on STR income.

| Zone/jurisdiction | STR allowed? | Stay minimum/frequency | Licensing |

|---|---|---|---|

| DC, CG (city) | Yes, by right | No 30-day minimum | City Business Tax Certificate plus state DBPR |

| RS, RT (city) | No, by default | 30-day minimum | N/A for STR use |

| NT, NE, owner-occupied (city) | Conditional | Case-by-case permit | City conditional-use permit plus DBPR |

| Unincorporated Pinellas County | Yes, with Certificate of Use | Inspection-dependent | COU: $450 annual renewal, $100 re-inspection every two years |

Downtown’s STR demand has a real seasonal spike attached to it: the Firestone Grand Prix of St. Petersburg closes downtown streets and part of the Albert Whitted Airport runway for a three-day festival weekend every year, most recently February 27 through March 1, 2026 (official event site). Every property in every jurisdiction still layers Florida’s DBPR vacation-rental license and Pinellas County’s Tourist Development Tax on top of local zoning approval.

Can I legally run an Airbnb in St. Petersburg? It depends entirely on the parcel’s zoning district. A condo in a DC or CG zone downtown can typically operate one; a single-family home in an RS or RT residential zone typically cannot, without qualifying for the narrower owner-occupied or three-stays-a-year exceptions.

Common buyer mistakes in this market

- Waiving the flood or elevation contingency to compete. In a market where single-family inventory is tightening, buyers sometimes skip the elevation certificate to move faster; that number drives almost every flood-mitigation and insurance decision downstream and is expensive to obtain after closing.

- Budgeting off the seller’s tax bill instead of the post-sale reset described above. Run the county’s own tax estimator against the purchase price, not the listing sheet.

- Assuming STR income before checking the zoning district, not just the HOA. Even where an HOA allows short-term rentals, city or county zoning can still prohibit them outright.

- Treating “waterfront” as one insurance category. AE and VE carry meaningfully different premium ranges; a canal lot and open-bay frontage two streets apart can differ by thousands of dollars a year.

A three-bedroom bungalow on 7th Avenue North in Historic Old Northeast sold for $992,000 on March 24, 2026, at 1,782 square feet. Its listing led with “NOT in a flood or evacuation zone,” underlining how directly flood status gets priced into marketing in this market, not just insurance quotes (Redfin).

Is now a good time to buy?

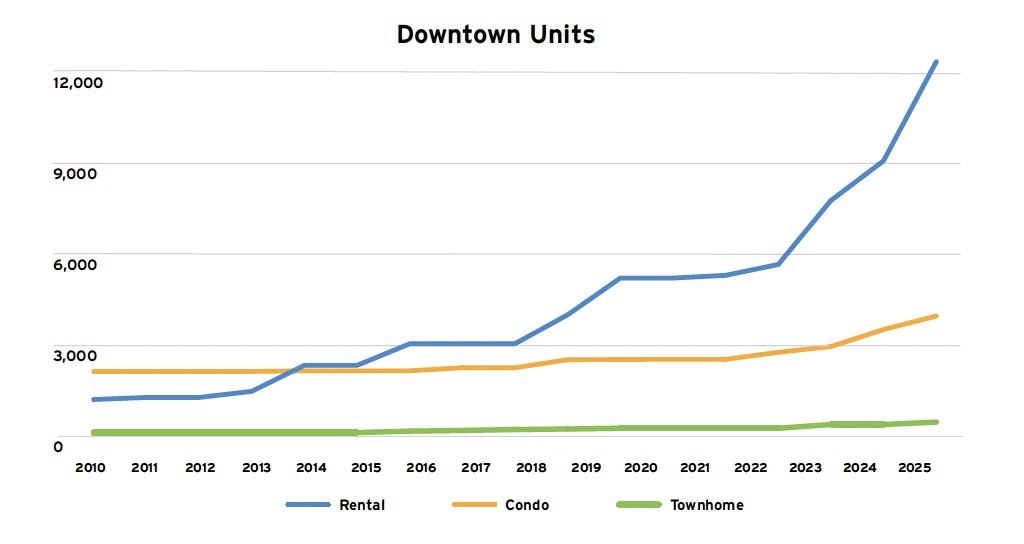

Single-family inventory in Pinellas County sat at 3.8 months in February 2026, tightening from prior-year levels, while the condo segment carried 8.3 months of supply, comfortably favoring buyers. The two segments of this market are answering “is now a good time” differently right now.

Is 2026 a buyer’s or a seller’s market in St. Petersburg? Segment-dependent. Single-family is edging back toward sellers as inventory tightens, while condos remain a buyer’s market, driven largely by luxury-tower closings that skew the headline price numbers and by older buildings absorbing higher post-reform insurance and reserve costs.

Schools, commute, and daily life

Florida Department of Education grades by individual attendance zone for the five neighborhoods above were not verified with a citable source in time for this piece; check a specific address against the state’s own school-grades database or GreatSchools before treating any neighborhood as “the good schools area.” Walkability is easier to pin down: Historic Old Northeast carries a Walk Score of 66, well above the citywide 43 (Redfin/Walk Score). Coquina Key and Snell Isle, by contrast, are car-dependent peninsula and island layouts where daily errands mean a drive.

Leave a Reply