Current Market Snapshot

The county-level numbers below are a starting point, not a ceiling or floor for any one city. Newport Beach and Irvine sit well above the median; Santa Ana and Anaheim sit well below it, a gap covered in the city guide further down.

| Metric | Figure | As of | Source |

|---|---|---|---|

| Median sale price, Orange County | $1.3M (up 4.7% year over year) | May 2026 | Redfin |

| Median days on market | 37 (34 a year earlier) | May 2026 | Redfin |

| Average home value index | $1,197,200 (up 1.2% year over year) | May 31, 2026 | Zillow |

| Months of supply | Approximately 2.6 (3.5 U.S., 3.2 statewide) | Nov 2025 | California Association of Realtors |

| 30-year fixed mortgage rate | 6.43% | Jul 2, 2026 | Freddie Mac |

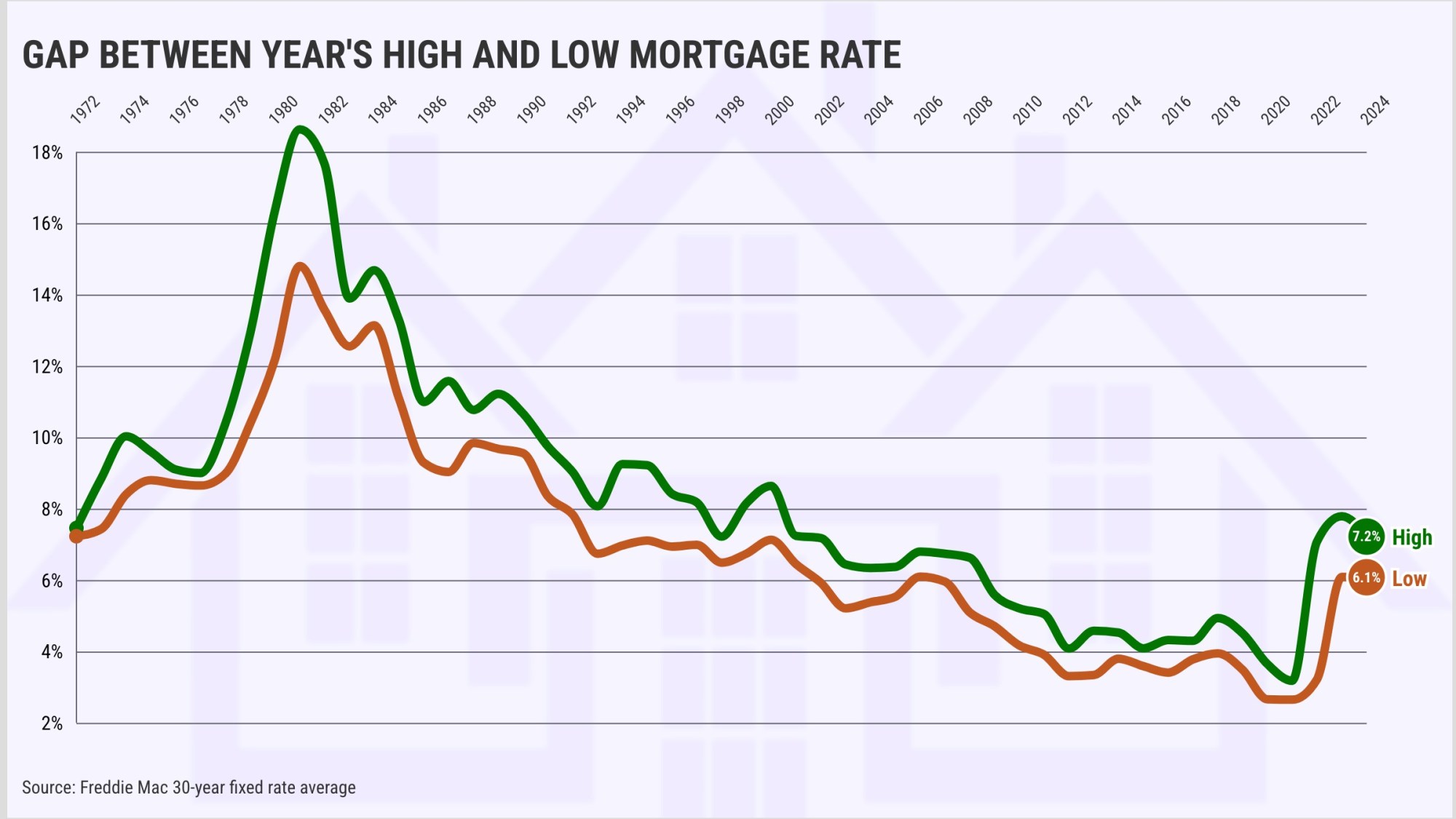

Fannie Mae’s June housing forecast expects the 30-year fixed to hold near 6.4% for the rest of 2026, while the Mortgage Bankers Association’s forecast runs slightly higher at 6.5% for the third and fourth quarters, per U.S. News’s roundup of both forecasts. The two numbers sit close enough together that neither points to a sharp move in either direction before year-end.

Is Orange County a buyer’s or a seller’s market right now?

Neither cleanly. Tight supply still favors sellers on well-priced homes. Slower days on market and a rate environment that has stopped climbing give buyers more room to negotiate repairs and credits than they had two years ago.

What a Purchase Costs Beyond the List Price

Standard homeowners insurance in the county averages $1,400 to $1,800 a year, per PowerRE Team’s 2026 cost analysis. Properties non-renewed by an admitted carrier and placed on the state’s insurer of last resort pay far more: the FAIR Plan averages roughly $3,000 to $3,200 a year statewide, and $5,000 to $12,000 a year in high-wildfire ZIP codes, according to Latent Insurance’s 2026 guide. Effective property tax runs 1.05% to 1.5% or more of assessed value once local additions and any Mello-Roos district are counted, according to Opelon’s Prop 19 calculator.

Mello-Roos and HOA dues vary by parcel and community too widely to state a single county figure honestly; a no-CFD inland condo and a Ladera Ranch or Rancho Mission Viejo single-family home can carry entirely different loads even at the same purchase price. The only reliable check is the specific address, not the neighborhood’s reputation.

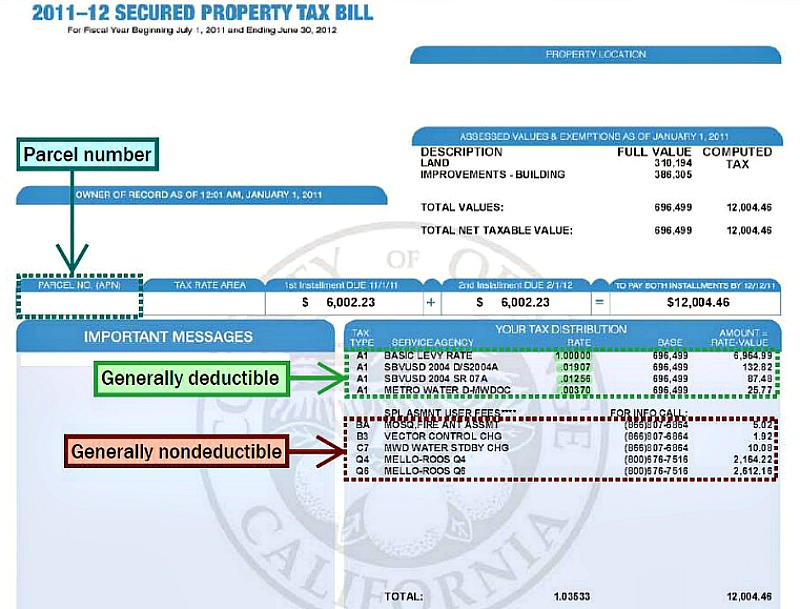

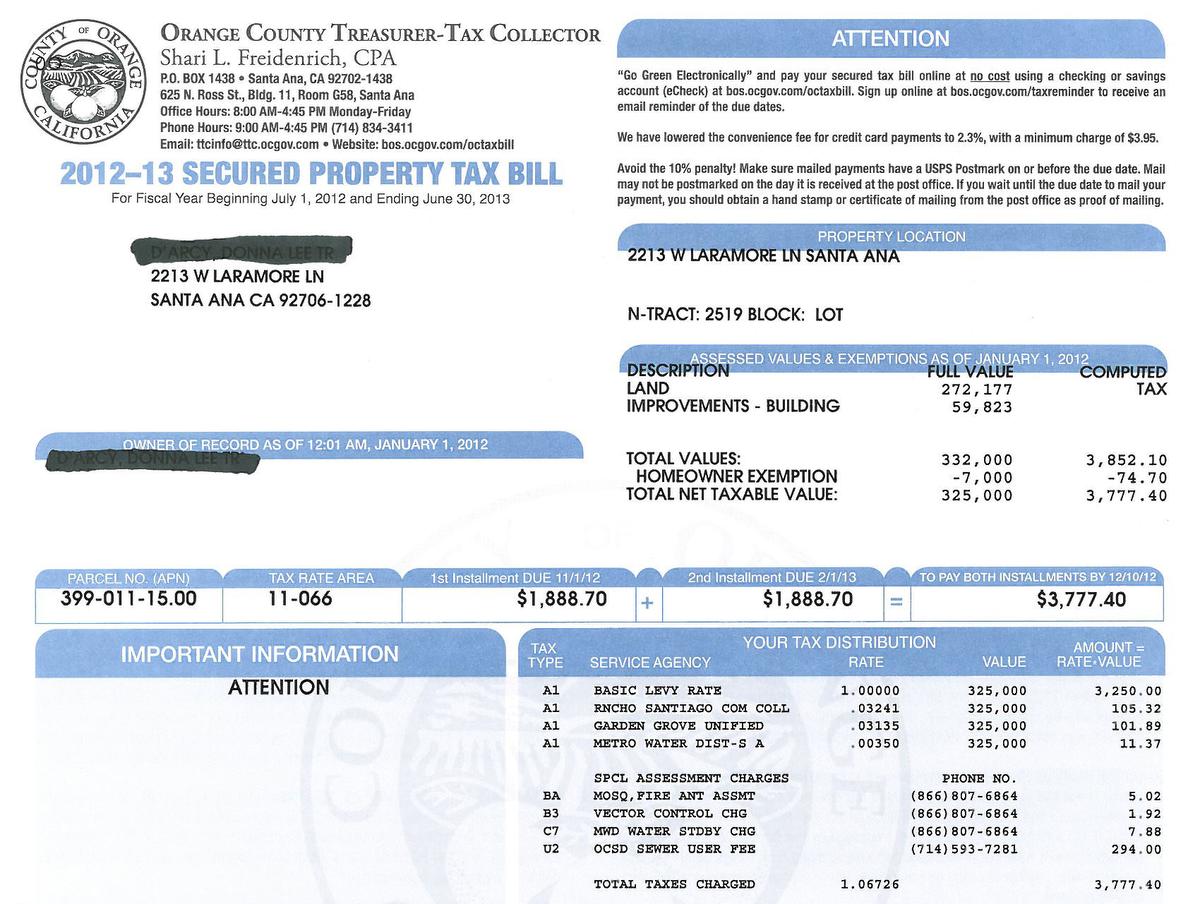

Mello-Roos does not show up on a listing photo or a Zillow estimate. It shows up on the seller’s current secured property tax bill, under the “Special Assessment Charges” section, and California Civil Code Section 1102.6b requires the seller to disclose it before close. Before writing an offer on anything built after the early 1990s in a master-planned area, request the current tax bill or ask escrow to run the parcel through the Orange County Treasurer-Tax Collector’s CFD lookup.

How do I check for Mello-Roos before I make an offer?

Ask for the seller’s current secured property tax bill and look under “Special Assessment Charges,” or search the parcel through the county Treasurer-Tax Collector’s tools. The bill also lists a phone number for the issuing agency if you want the payoff schedule or expiration year before you write the offer.

Buyer-Agent Commission and Offer Practice in 2026

Since August 17, 2024, an MLS-participant agent must have a signed written buyer representation agreement in place before touring a home with a buyer, per NAR’s own summary of the settlement practice changes. That agreement states the buyer’s agent compensation and confirms it is fully negotiable and not set by law. California’s average total commission runs about 5.47% of sale price, split between the two sides, per usrealtytraining.com’s 2026 commission report.

Nothing requires a seller to offer buyer-agent compensation. Most OC sellers still do, negotiated off the MLS rather than published on it, because a listing with no offered buyer-side compensation narrows the pool of agents willing to show it.

Do I have to pay my own buyer’s agent in Orange County now?

Only if the seller declines to offer compensation and your written agreement isn’t amended to route a concession through the deal. Most OC sellers still cover it; put the question to your agent in writing before you tour, not after you make an offer.

City-by-City Price and Character Guide

| City | Character | Short-term rental rule |

|---|---|---|

| Newport Beach | Coastal, high visitor demand | 1,550-permit cap (1,475 residential, 75 mixed-use); R-1 zones prohibited |

| Huntington Beach | Coastal, family-oriented | Hosted rentals in Zones 1 and 2 only; unhosted limited to Sunset Beach, permitted by March 1, 2022 |

| Irvine | Inland, master-planned | All residential-zone short-term rentals prohibited |

| Fullerton | Inland, older housing stock | 45-day moratorium adopted May 20, 2025 after 173 unpermitted listings identified |

| Santa Ana | Inland, most accessible entry point | Subject to Uniform Transient Occupancy Tax rules; verify current permit status with the city |

| Laguna Beach | Coastal, artist-colony character | Permit cap system under Municipal Code Chapters 5.84 and 25.23 |

Every row above is a starting point for due diligence, not a purchase decision on its own; permit eligibility inside a single city can vary block by block, and an HOA can prohibit what the city zoning allows.

The clearest current example of new coastal supply working through the pipeline sits in Huntington Beach: the owner of a 92-acre former oil field between Goldenwest and Seapoint wants to build up to 800 residential units and up to 350 hotel rooms there, and the City Council is expected to take up the required coastal-program amendment in mid-2026, per the city’s own project status page.

For Relocating Buyers

Anyone moving in from out of state should confirm homeowners insurance eligibility for a specific address before waiving an inspection or appraisal contingency. A property that looks unremarkable on a listing photo can already be non-renewed by the standard market, and finding that out after removing contingencies is the single most expensive mistake a relocating buyer can make.

Should You Buy Now or Wait for Rates to Drop

Fannie Mae’s forecast holds the 30-year fixed near 6.4% for the rest of 2026; the Mortgage Bankers Association’s is 6.5%. On a $1,040,000 loan (80% of the $1.3M county median), the monthly principal and interest payment at 6.43% runs about $6,530. At a hypothetical 5.9%, the same loan runs about $6,180, a difference of roughly $350 a month. Closing six months later to chase that difference also means six more months of the county’s 4.7% year-over-year appreciation working against the buyer, an effect of comparable size to the rate gap itself.

Should I wait for mortgage rates to drop before buying in Orange County?

Both major forecasters expect the 30-year fixed to stay in the 6.3% to 6.5% range through the rest of 2026. Waiting for something meaningfully lower is a bet against both forecasts, not a near-certain payoff.

Selling in Orange County: Pricing, Disclosure, and Closing Costs

Orange County sellers customarily pay the county documentary transfer tax and the owner’s title insurance policy; buyers customarily pay the lender’s title policy and their own loan-related fees. None of this is fixed by law, only by local custom, and every item is subject to negotiation in the purchase contract.

| Item | Typical payer | Typical OC amount |

|---|---|---|

| County documentary transfer tax | Seller (by custom) | $1.10 per $1,000 of sale price |

| Owner’s title insurance policy | Seller (by custom) | Varies with sale price; a standard cost of sale |

| Lender’s title policy | Buyer | Additional to the owner’s policy |

| Escrow fee | Split by custom | Flat fee plus a per-thousand-dollar rate, set by the escrow company |

The transfer tax figure above is set by the Orange County Clerk-Recorder and applies countywide; unlike Los Angeles, most Orange County cities do not layer a separate city-level transfer tax on top of it.

Investor and Landlord Rules for 2026

Homeowners 55 or older, or severely and permanently disabled, can transfer their Proposition 13 base year value to a replacement primary residence anywhere in California, up to three times in a lifetime, per the California State Board of Equalization. A replacement of equal or lesser value carries the old base with no adjustment; a costlier replacement adds the difference between the two values to the transferred base. The separate parent-child exclusion, which some investors confuse with the age-55 portability rule, is capped at the parent’s factored base year value plus $1,044,586 through February 2027, per Opelon’s calculator.

What short-term rental rules should an investor check before buying in Orange County?

Zoning eligibility, permit caps, and transferability all vary by city and sometimes by block within a city. Newport Beach and Laguna Beach both cap total permits; Irvine bans short-term rentals outright in residential zones; an HOA can prohibit what the city otherwise allows.

Risks Worth Watching

California’s Sustainable Insurance Strategy requires carriers that want to use forward-looking catastrophe models in their rate filings to commit to writing at least 85% of their statewide policy share in wildfire-distressed areas, per the California Department of Insurance. Non-renewal for wildfire risk requires at least 75 days’ written notice under state law. The FAIR Plan’s dwelling coverage cap was raised to $3 million for single-family homes in late 2024, closing much of the gap that once forced high-value coastal owners into a layered FAIR-Plan-plus-surplus-lines structure.

Leave a Reply