What counts as “new construction” here, and why the count changes by source

New construction covers three different products that get lumped under one label: a builder-community home sold directly by a production builder, a spec home built on an individually owned infill lot and listed like any resale, and a to-be-built or pre-construction contract where the buyer selects finishes before the slab is poured. Livabl’s community-level count finds 7 active new-home communities in New Smyrna Beach, split between 1 townhome community with 2 floorplans and 7 single-family communities with 31 floorplans, and names D.R. Horton as the most active developer in the city (Livabl). That is a narrower definition than Redfin’s 57-listing MLS count, which also captures independent spec homes and to-be-built contracts outside any named community. Neither number is wrong; they are answering different questions. If a builder’s own website count and a portal’s count don’t match, this is almost always why.

Is there active new construction for sale in New Smyrna Beach right now? Yes: 57 MLS-listed new-construction homes as of the June 30, 2026 snapshot, spread across roughly 7 to 8 builder communities plus independent spec listings, at a $499,000 median (Redfin).

Who’s building now: communities and current prices

Three builders account for the pricing spread visible in current listings. D.R. Horton is the most active developer in the city by community count (Livabl) and currently lists its Aria floorplan from $361,990 (Zillow), spread across communities including Coastal Woods, Sandalwood, Oak Leaf Preserve, Old Mission Cove, and Waywater. Ryan Homes lists from $430,000, though no published incentive terms for that listing turned up in this search (Zillow). Maronda Homes builds in New Smyrna and Edgewater with no HOA and no CDD, offering plans up to 4,700 square feet, 6 bedrooms, and a 3-car garage, from $345,990 (Trulia; Maronda Homes).

| Builder | Communities found | Entry price | Notable term |

|---|---|---|---|

| D.R. Horton | Coastal Woods, Sandalwood, Oak Leaf Preserve, Old Mission Cove, Waywater | from $361,990 | Occupation-based closing-cost credit, see below |

| Ryan Homes | NSB listing(s) | from $430,000 | No incentive terms published for this listing |

| Maronda Homes | New Smyrna & Edgewater | from $345,990 | No HOA, no CDD; buyer can supply own homesite |

The spread from $345,990 to $430,000 at entry level tracks lot type and HOA/CDD structure more than square footage alone. Maronda’s no-CDD community undercuts Ryan Homes’ entry price by roughly $84,000 while offering comparable bedroom counts, which is a starting point for the fee math covered later on this page.

Builder incentives: what they reduce, and what to watch for

Not every builder incentive works the same way, and the differences change what a home costs you at closing versus over the life of the loan.

| Incentive type | What it reduces | What to watch for | Worked example |

|---|---|---|---|

| Closing-cost credit | Cash needed at closing | Often restricted by buyer eligibility and a hard contract deadline | D.R. Horton’s Main Street Stars: up to $1,000 toward closing costs for military, law enforcement, fire, healthcare, and education buyers; must contract by September 30, 2026 and close by October 31, 2026 (D.R. Horton) |

| Rate buydown | Monthly payment, usually for a set initial period | Payment typically rises to the note rate once the buydown period ends | No New Smyrna Beach buydown terms were published at the time of this search; get the exact post-buydown schedule in writing from the builder’s lender |

| Design-center or upgrade credit | Out-of-pocket cost for selected options | Does not reduce the loan amount or the appraised base price | Terms vary by community; confirm which options qualify |

| Straight price reduction | Purchase price and loan amount together | Lowers your future equity basis along with the price | Compare directly against a credit or buydown’s total value before choosing |

D.R. Horton’s Main Street Stars credit is a useful case because it shows what a real, currently active incentive looks like: modest, dated, and restricted to specific occupations, distinct from a large blanket rate buydown. Buyers who don’t qualify for an occupation-based program should ask the sales office directly what’s currently offered broadly, since published terms change by community and by month.

Is a builder incentive worth more than a straight price cut? It depends on which one moves your total cost more: a $10,000 price cut lowers your loan amount permanently, while a temporary rate buydown of similar value may cost less monthly for a year or two, then revert. Ask for both quotes side by side before deciding.

What changes when you buy new instead of resale

New construction carries a builder warranty and current Florida wind-resistance code compliance that an older resale home may not. Resale offers established landscaping and, in many mature communities, a CDD bond further into repayment or already retired. That is the extent of the comparison this page can source with confidence at the individual-community level.

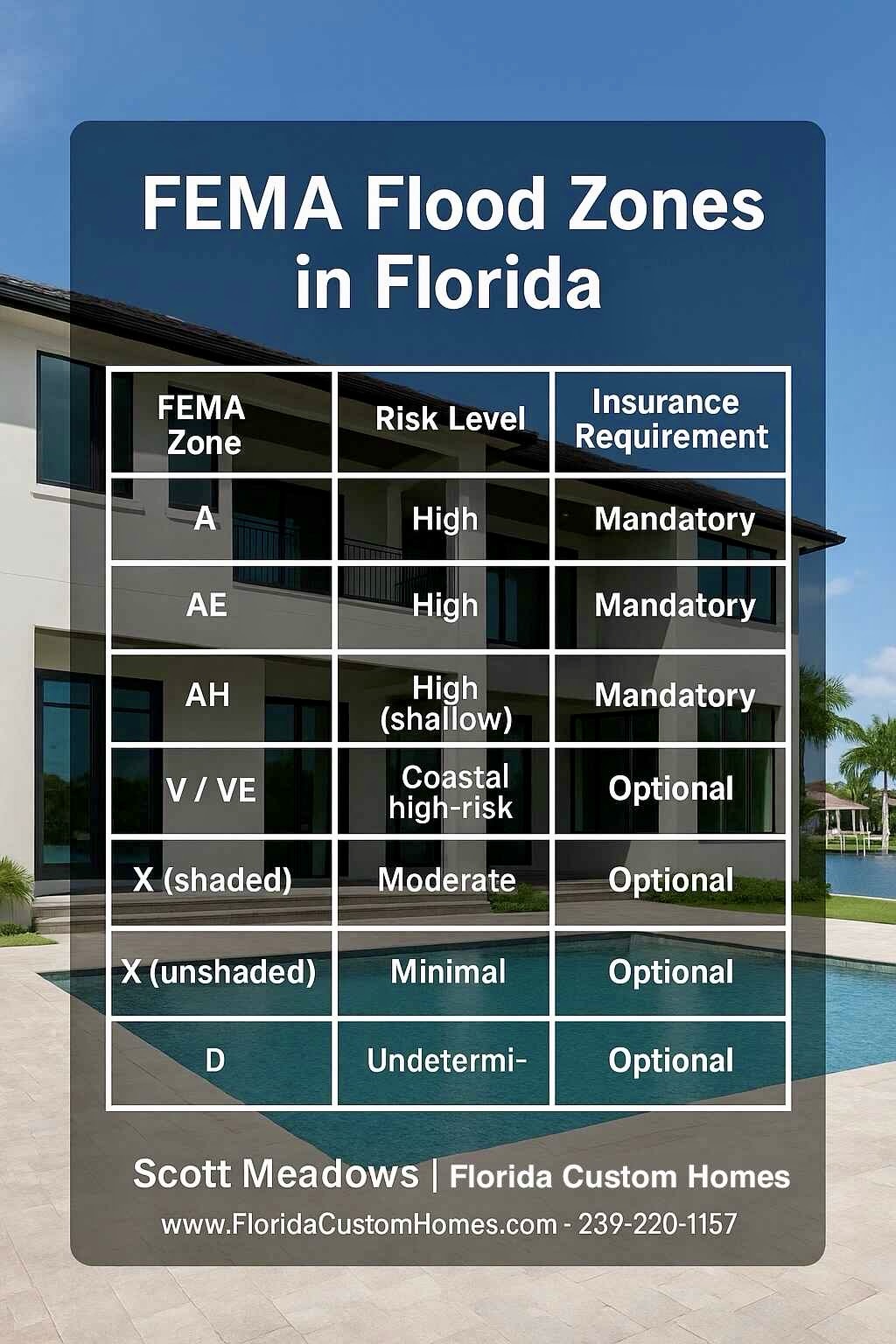

Barrier peninsula vs. mainland: how location moves your flood insurance

New Smyrna Beach sits partly on the mainland and partly on the barrier peninsula across the Indian River, and FEMA’s flood zone maps, which the city applies directly under its floodplain regulations, treat those two geographies very differently (City of New Smyrna Beach; FloodSmart.gov). Zone AE means FEMA has calculated a specific base flood elevation and mandates flood insurance for any federally backed mortgage; Zone VE adds wave-action risk on top of that and is the costliest designation; Zone X carries no federal insurance mandate. Canal-front and Intracoastal-adjacent Volusia County parcels are commonly mapped AE, with typical premiums for a $300,000 to $500,000 home estimated at $1,500 to $3,500 a year by one Volusia-focused real estate advisory source (Coastal Volusia Homes). Direct oceanfront and barrier-island parcels elsewhere in coastal Florida are commonly mapped VE, with premiums estimated at $4,000 to $10,000-plus a year by a separate Florida coastal advisory source (Ben Laube Homes). Both figures are named, dated trade estimates for the broader region, not confirmed New Smyrna Beach rates; the only way to know a given parcel’s zone and premium is to pull its FEMA flood map before writing an offer.

| Area type | Typical FEMA zone | Insurance signal | Who it suits |

|---|---|---|---|

| Inland mainland parcels | Zone X (moderate/low risk) | No federal insurance mandate; optional coverage still worth considering | Buyers prioritizing lower carrying cost over water proximity |

| Canal-front / Intracoastal-adjacent | Zone AE (high risk, mandatory insurance) | Estimated $1,500 to $3,500/yr for a $300,000 to $500,000 home (Coastal Volusia Homes) | Buyers who want water access and can budget the mandatory premium |

| Direct oceanfront / barrier peninsula | Zone VE (high risk, wave-action, mandatory insurance) | Estimated $4,000 to $10,000-plus/yr (Ben Laube Homes) | Buyers prioritizing beach proximity who confirm the premium in writing first |

The gap between the inland and oceanfront estimates above is large enough to offset most of the price difference between a mainland and a beachside new-construction home. Run the insurance quote before comparing listing prices, not after.

How do I check my flood zone before I make an offer? Pull the address on FEMA’s Flood Map Service Center, linked from floodsmart.gov, before writing an offer, and ask the builder or listing agent for the parcel’s flood zone in writing rather than relying on the community’s general reputation.

CDD and HOA fees: the cost the payment calculator skips

A Community Development District is a special-purpose local government created under Chapter 190 of the Florida Statutes, empowered to issue bonds for infrastructure like roads, drainage, and amenities, with the debt repaid through an annual assessment on the property tax bill (Fla. Stat. Ch. 190). That assessment sits separate from, and in addition to, any HOA dues. Not every New Smyrna Beach new-construction community carries one: Maronda’s New Smyrna and Edgewater community is marketed specifically as no HOA and no CDD (Maronda Homes), a real, checkable counterexample to the assumption that all new construction here comes with a CDD attached. No New Smyrna Beach-specific CDD fee schedule turned up in this search; get any figure a sales office quotes you in writing against the community’s own CDD disclosure and the Volusia County property appraiser’s records.

- Ask directly whether the community has an active CDD, since it will not always be volunteered before you ask.

- Request the current assessment amount in writing, separate from the HOA quote, before comparing total monthly cost across communities.

- Check whether the bond is prepayable, since some CDDs allow early payoff of the capital assessment.

What’s a CDD fee, and will I pay one in New Smyrna Beach? It depends on the specific community. CDDs are legal under Chapter 190, F.S., and fund infrastructure through a bond repaid via your property tax bill; some New Smyrna Beach builders explicitly market no-CDD communities, so ask before you assume either way.

Buying without your own agent: what Florida law requires

Under Florida law, a real estate licensee defaults to operating as a transaction broker, providing limited duties to both sides instead of full fiduciary loyalty to either, unless a buyer signs a written single-agent agreement establishing that fiduciary relationship (Fla. Stat. §475.278). A builder’s on-site sales representative is typically compensated by and working for the builder throughout the transaction. Buyers who want full fiduciary representation, meaning undivided loyalty and confidentiality, need to arrange it themselves in writing before touring a model home.

Do I need my own real estate agent to buy directly from a builder? No law requires it, and Florida defaults every licensee involved to limited transaction-broker duties unless a buyer signs a separate single-agent agreement securing full fiduciary representation (Fla. Stat. §475.278).

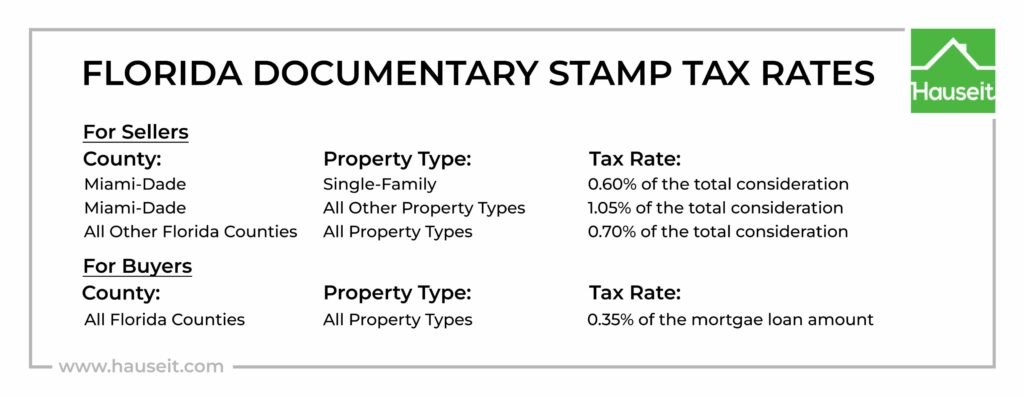

Closing costs: doc stamps, intangible tax, and who typically pays

Florida charges a documentary stamp tax of $0.70 per $100 of the sale price on the deed, customarily paid by the seller, plus a separate $0.35 per $100 stamp on the mortgage note and a 0.2% intangible tax on the new loan amount, both customarily paid by the buyer (Florida Department of Revenue; Barnes Walker). On a $400,000 purchase, that works out to roughly $2,800 in deed stamps for the seller and, on a $320,000 loan, roughly $1,120 in note stamps plus $640 in intangible tax for the buyer, before any lender or title fees. These are statutory rates, applying the same way whether the home is new or resale.

Common mistakes, and a note for out-of-state buyers

The recurring mistake in this market is comparing a bare listing price across sources without checking whether the number includes a CDD assessment, a defined flood zone premium, or the incentive that made the headline price possible. A second, related mistake is assuming the builder’s on-site representative is working for you.

Leave a Reply