What It Actually Costs at the Median Price

Every LA guide gives ranges in isolation, a down payment percentage here, a closing-cost percentage there. Stacked against one property, the numbers look like this:

| Scenario | Down payment | Est. closing costs | Est. monthly P&I at 6.43% |

|---|---|---|---|

| FHA, 3.5% down | $32,800 | $18,700 to $37,500 | roughly $5,780 |

| Conventional, 10% down | $93,700 | $16,900 to $33,700 | roughly $5,310 |

| Conventional, 20% down | $187,400 | $15,000 to $30,000 | roughly $4,720 |

Down payment figures use the Redfin LA County median; loan limits come from the FHFA’s 2026 conforming and high-cost figures; monthly principal and interest is calculated at the Freddie Mac PMMS rate for July 2, 2026. Closing-cost figures are treated skeptically further down this page.

Financing: Down Payment and the 2026 Loan Limits

The 2026 baseline conforming loan limit is $832,750; in high-cost counties, including Los Angeles, it rises to cover the vast majority of single-family purchases at the county median. That’s why most LA buyers are shopping in conforming or FHA territory, not jumbo. FHA down payments start at 3.5% with a minimum 580 credit score; conventional loans start around 3% for well-qualified buyers, but competitive offers in a multiple-offer situation typically carry 10% or more, since a thin down payment can read as a shakier bid next to a seller’s other offers.

Who Pays Your Agent Now

Since August 17, 2024, MLS listings can no longer carry a pre-set buyer-agent commission field, and any agent working with a buyer must have a signed representation agreement in place before that buyer tours a home, per the National Association of Realtors’ settlement FAQ. Sellers can still offer to pay the buyer’s agent; they just do it outside the MLS, in a private conversation between agents or in the offer itself. Nothing in the rule stops you from asking the seller, in your offer, to cover some or all of your agent’s negotiated fee. It simply has to be an explicit ask now instead of an assumed default.

There’s a newer wrinkle competitors haven’t caught. A second, separate settlement, Tuccori v. At World Properties, adds a $52.25 million buyer-side payout on top of the original case, with a final court hearing scheduled for July 28, 2026, according to Inman’s coverage of the settlement. It doesn’t change how you negotiate today, but the commission-rule landscape is still moving, not settled the way most 2025-vintage guides assume.

Do I have to pay my buyer’s agent out of pocket now?Not automatically. Sellers can still offer to cover buyer-agent compensation; you just have to negotiate it explicitly, in writing, rather than assume it’s baked into every listing the way it used to be advertised on the MLS.

Inspections: What to Get, What You Can Skip

| Inspection | Typical cost | Consequence of skipping | Skip if budget is tight? |

|---|---|---|---|

| General home inspection | $300 to $600 | Misses structural, electrical, roof, and HVAC defects that can run into the tens of thousands to fix | No |

| Termite / wood-destroying-organism (WDO) | $75 to $325 | Undetected infestation can compromise framing; many lenders require a clearance letter anyway | No |

| Sewer lateral scope | roughly $200 to $250 add-on | A cracked or root-invaded line under an older LA lot can cost $10,000 or more to replace | Situational, prioritize on homes built before 1980 with the original line |

General inspection and termite cost data from CalcBee’s home inspection cost estimator and Angi’s termite inspection cost guide. This table is the closest thing to a decision rule a first-timer gets on inspections: skip nothing structural, and reserve judgment only on the add-on that depends on the property’s age.

Which inspection should I never skip?The general home inspection. It catches the defects most likely to cost five figures to fix, and it’s the cheapest of the three relative to what it can prevent.

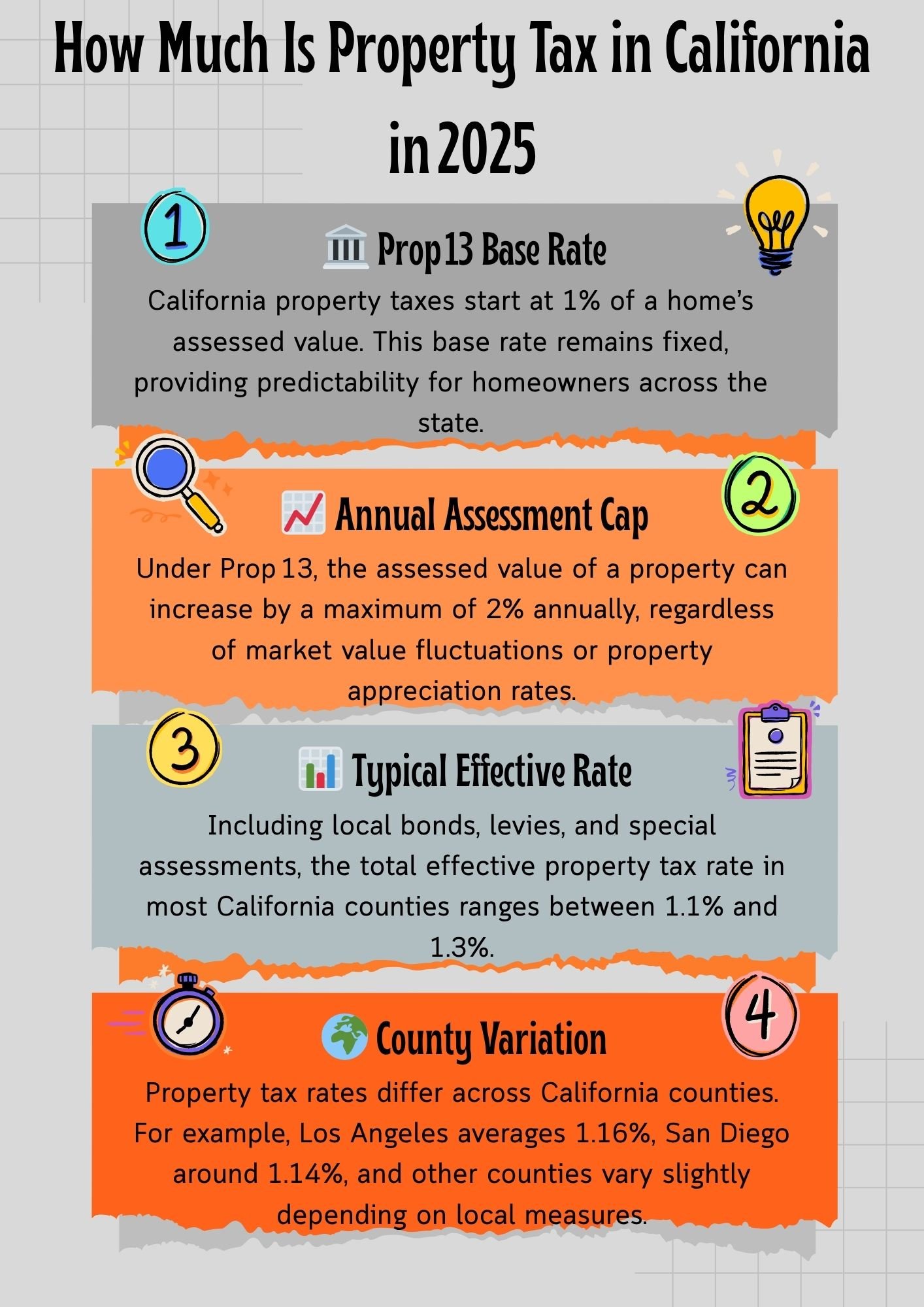

Property Tax and the Mello-Roos Line Item

Three widely-repeated numbers float around LA homebuying content: property tax “around 1.2%,” closing costs “2 to 5%,” and neither is attached to a named source anywhere in the competitor set this page was benchmarked against. Here’s what’s verifiable: Proposition 13 caps the base rate at 1% of assessed value, and local voter-approved bonds typically add another 0.1% to 0.55%, landing most LA County owners at an effective rate of roughly 1.1% to 1.4%, according to a constitutional and Board of Equalization-sourced breakdown at LegalClarity.

Mello-Roos is a separate animal. It’s a flat annual dollar charge tied to a Community Facilities District, not a percentage of value, and it can add roughly $1,500 to $7,000 or more per year in newer subdivisions. It shows up as its own line item on the tax bill and won’t appear in a generic “1.2%” estimate at all.

Why do different sites quote different property tax rates for the same neighborhood?Because the base 1% rate is identical everywhere, but the bonds stacked on top of it vary by school district and city, and Mello-Roos, where it applies, is a flat fee unrelated to the percentage-based rate.

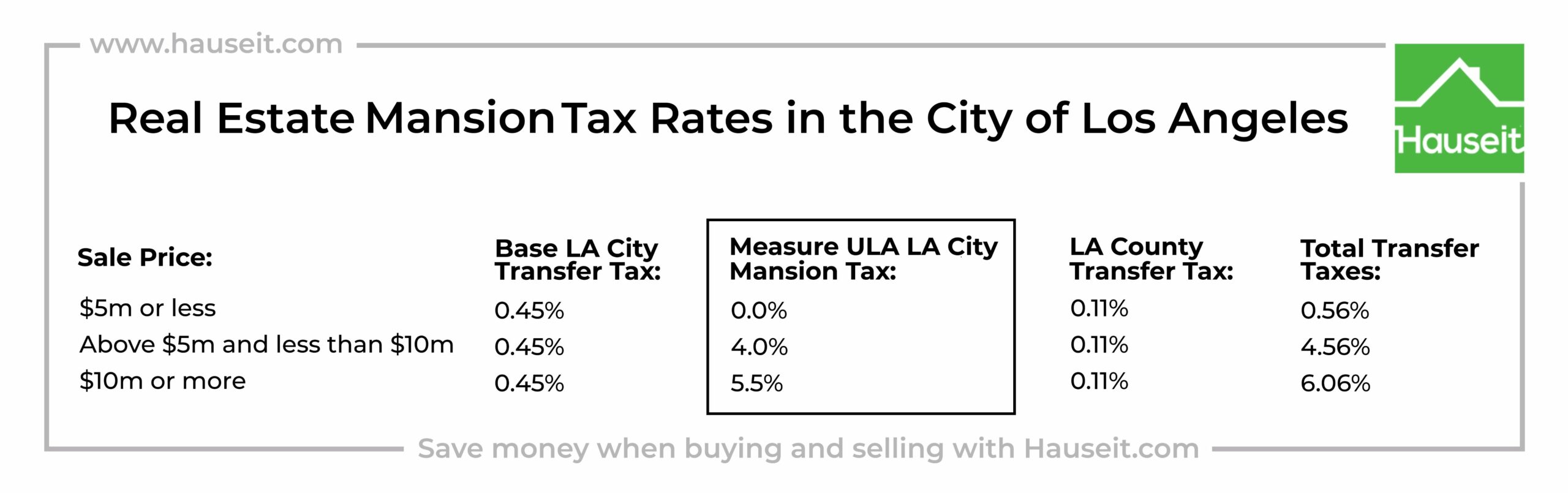

Measure ULA and Where It Stops Applying

For sales closing after June 30, 2026, the City of Los Angeles taxes transfers between $5.4 million and $10.9 million at 4%, and anything above $10.9 million at 5.5%, per the LA Office of Finance’s ULA FAQ. A median-priced LA purchase sits roughly $4.4 million below the lower threshold. The tax applies to the full sale price, not the gain: Dodgers first baseman Freddie Freeman reportedly owed roughly $2 million in ULA tax on a Los Angeles home sale that closed below what he originally paid for it, because the tax doesn’t care about profit or loss.

Does the Mansion Tax apply if I’m buying a typical home in LA?No. It only applies to sales above $5.4 million within city limits. A $937,000 median purchase is nowhere near the threshold.

Why Nothing Under $700,000 Stays on the Market Long

The median LA homeowner has now held their property for 20 years, the longest tenure of any major U.S. metro and up from 19.4 years just a year earlier, according to Redfin’s 2025 tenure analysis. Much of that is Proposition 13, which keeps long-tenured owners’ tax bills far below what a new buyer would pay for the same house, combined with mortgage rates that fell as low as 3% during 2020 to 2022 and haven’t returned there since. The practical effect: the entry-level inventory that used to turn over every five to seven years mostly isn’t turning over at all, so budget for a light renovation on an older, smaller property.

Is Dream For All coming back?Not on any announced timeline. Its 2026 registration window closed March 16 with no new applications accepted, per CalHFA’s own program page. Don’t structure a purchase timeline around waiting for it.

Down Payment Assistance That’s Actually Funded Right Now

| Program | Assistance | Purchase price cap | Status, mid-2026 |

|---|---|---|---|

| LACDA HOP80 | Up to $100,000 or 20% of price, whichever is less | $700,000 | Open, income-limited to 80% AMI tier |

| LACDA HOP120 | Up to $85,000 or 20% of price, whichever is less | $850,000 | Open, income-limited to 120% AMI tier |

| CalHFA Dream For All | Up to 20% of price, capped at $150,000 | None published | Closed since March 16, 2026, no reopening date |

Program terms per the Los Angeles County Development Authority’s Home Ownership Program page, AMI guidelines effective June 1, 2026.

Mistakes That Cost Buyers Money

- Assuming 20% down is required. Conventional loans start around 3%, and FHA starts at 3.5%; the real tradeoff is mortgage insurance cost against how competitive a thin down payment looks in a multiple-offer situation.

- Missing a Mello-Roos flat fee. See the property tax section above; ask directly whether a property sits in a Community Facilities District before writing an offer.

- Skipping the sewer scope on a pre-1980 property to save $250. A collapsed lateral under an older LA lot is a five-figure repair.

- Waiting for Dream For All. It’s closed with no announced reopening; a purchase timeline built around it is a timeline built around nothing.

What the Disclosures Actually Cover

Any LA property in a designated wildfire zone requires a point-of-sale disclosure under AB38, effective since January 1, 2021, per the LA Fire Department’s fire-zone page. Separately, the city’s mandatory seismic retrofit ordinance targets roughly 13,500 identified wood-frame buildings with soft or open ground floors, mostly older multi-unit apartment buildings, not detached single-family homes, according to tracking of LA’s retrofit program. If you’re buying a small multi-unit property, check the city’s soft-story inventory before assuming a seller’s standard disclosures cover it.

Leave a Reply