Should you sell your land and house together or split them?

The right answer depends on which constraint binds first: the lender, the zoning code, or the market.

| Scenario | Recommended path | Why |

|---|---|---|

| Mortgage carries a due-on-sale clause and splitting would push the remaining home’s loan-to-value above 60% | Sell together | Fannie Mae’s servicing rules require a principal paydown above that threshold, or may deny the release outright |

| Zoning does not allow the smaller of the two resulting lots | Sell together, or apply for a variance first | An unbuildable parcel is hard to finance and hard to resell later |

| Land is unencumbered, meets minimum lot size, and local land demand is active | Sell separately | Two buyer pools, priced separately, often beats one combined listing price |

| The acreage is what justifies the house’s price (rural estate, hobby-farm buyers) | Sell together | Splitting removes the feature driving the price |

| Owner needs cash quickly and the land alone is easier to finance for a land-loan buyer | Sell the land first, the house within 2 years | Preserves eligibility for the combined IRS Section 121 exclusion |

The lender constraint usually decides the question before zoning or market timing get a vote.

Can I sell my land without selling my house? Yes, if the parcels are legally separate or can be subdivided, the mortgage allows the release (or the land is unencumbered), and zoning supports the resulting lot. Selling the land first also starts a 2-year clock for combining it with the home sale under IRS Section 121, covered below.

The legal mechanics of splitting land from a house

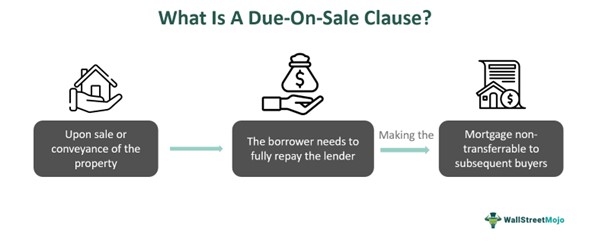

A due-on-sale clause is a standard mortgage provision that lets the lender demand full repayment if any part of the mortgaged property transfers without consent, as Cornell’s Legal Information Institute defines it. It is a contract right, not a criminal statute, and lenders exercise it at their discretion rather than automatically. For loans owned by Fannie Mae, a borrower requesting a partial release of the sold parcel submits Form 236; per Fannie Mae’s servicing guide updates, the servicer can approve the release without forcing extra principal payment as long as the loan-to-value ratio on the remaining property stays under 60% after the release. Above that threshold, the seller typically has to apply sale proceeds toward the loan balance before keeping any cash.

Zoning works independently of the mortgage. A county with a minimum lot size of, say, 2 acres per parcel will not approve a split that creates a sub-2-acre lot, regardless of what the lender allows.

Subdivision steps, survey to recording

- Survey and plat. Hire a licensed surveyor to prepare a boundary survey and proposed plat.

- Zoning submission. Submit the plat and a concurrency or zoning review application to the county planning department.

- Review comments. Address feedback from the county surveyor, utilities, or environmental health staff.

- Governing-body approval. Obtain sign-off from the commission or council, depending on jurisdiction.

- Recording. Record the approved plat and the new deeds at the county recorder or clerk of courts.

Seminole County, Florida illustrates the concrete shape of this: a minor plat there requires a $250 concurrency-review application fee, a boundary survey from a Florida-licensed surveyor at a specified plat scale, County Commission approval, and then recording with the Clerk of Courts. A simple lot split with no new infrastructure generally takes 30 to 90 days from application to recording in most counties; a full subdivision plat with new streets or utilities can take 6 to 18 months. Fees, required documents, and review steps vary by county, so treat any single county’s numbers as an example of the shape of the process, not a national figure.

What happens to septic, wells, and shared access when you split

Splitting a lot does not automatically split its infrastructure. If the house’s septic system, well, or driveway sits partly on the parcel being sold, the sale can leave one lot dependent on land it no longer owns.

Two real requirements show why this matters. Anne Arundel County, Maryland, requires a minimum of 10,000 square feet reserved exclusively for each building site’s initial septic system plus two future replacement systems, meaning a split that leaves too little dedicated area on either resulting lot can make that lot unbuildable. Hamilton County, Ohio, requires a permanent recorded easement whenever any part of a shared septic system sits on a separate parcel from the structure it serves. Skipping that easement is one of the more common reasons a split later stalls at closing.

Tax and financial consequences of splitting vs. selling together

Under IRS Publication 523 and the underlying regulation, vacant land adjacent to a principal residence can be included in the home’s capital gains exclusion if the land was used as part of the residence and the land sale and the home sale occur within 2 years of each other, in either order. The combined limit stays at $250,000 for a single filer or $500,000 for a married couple filing jointly; it does not double because the sales happen separately.

A worked example in the underlying Treasury regulation shows the mechanics: a taxpayer sold 8 acres for a $110,000 gain in one year, could not exclude it because the home had not yet sold, then sold the home and remaining 2 acres 2 years later for a $180,000 gain, excluded that gain, and filed an amended return to retroactively claim the remaining exclusion on the earlier land sale. Selling the land more than 2 years before or after the home sale forfeits that combined treatment entirely; the land sale is simply taxed as its own transaction.

Will splitting my land trigger a tax bill? Not necessarily. If the land sale and the home sale both close within 2 years of each other and the land was used as part of the residence, the IRS treats them as one sale for exclusion purposes. Outside that 2-year window, the land sale is taxed on its own.

How land buyers differ from home buyers

Land buyers are usually planning a future use, building, farming, recreation, or resale, rather than reacting to move-in condition, so curb appeal and staging carry little weight. Financing timelines and lender scrutiny run longer than a typical home purchase. That is the extent of the difference that actually changes what a seller should do.

Pricing: land vs. house vs. combined listings

| Financing type | Typical down payment | Source |

|---|---|---|

| Homesite land, under 5 acres | 15% to 20% | GreenStone Farm Credit Services |

| Recreational or larger land, 5+ acres | 20% to 35% | GreenStone Farm Credit Services |

| FHA land-to-build construction loan | 10%, credit score as low as 500 | LendingTree, citing FHA program terms |

| Combined house-and-acreage listing | Follows standard conventional, FHA, or VA home-loan terms | LendingTree |

A buyer financing raw land alone faces a materially larger cash requirement than a buyer financing the same acreage attached to a house, which shrinks the pool of qualified land-only buyers relative to a combined listing.

| Listing type | Typical time on market | Source |

|---|---|---|

| Existing single-family home, national median (Nov. 2025) | 36 days | NAR Existing-Home Sales Report |

| Land only, national (2025 closings) | About 125 days | National Land Realty 2025 Industry Report |

| Land in the fastest counties | 2 to 3 months | National Land Realty 2025 Industry Report |

| Land in the slowest counties | A year or more | National Land Realty 2025 Industry Report |

How long does a combined land-and-house listing take to sell compared to land alone? No national figure separates that listing type specifically, but because buyers finance it like a house rather than like raw land, it should track closer to the 36-day home median than the roughly 125-day land median.

Preparing and marketing each scenario

- Combined listing. One agent, typically the residential agent, markets the whole property; acreage becomes a selling feature rather than a separate product.

- Split sale. Land-specific marketing (platforms, buyer lists, zoning detail) differs enough from residential marketing that commission arrangements should specify which agent handles which parcel before either one is listed.

- Either scenario. A current survey, clear boundary markers, and utility documentation matter more to land buyers than paint and landscaping do.

Do I need two agents to sell a house-and-land package? Not necessarily for a combined listing, where one agent can represent the whole property. For a split sale, pairing a residential agent with a land specialist is common, since the marketing and buyer pool differ enough that few agents cover both well.

Common mistakes when selling land with a house

| Document | Needed to sell together | Needed to sell split | Why it matters |

|---|---|---|---|

| Deed and legal description | Yes | Yes, two new descriptions | A split needs the plat’s new legal descriptions recorded before either lot can close |

| Survey or plat | Helpful | Required | Establishes the boundary the county will approve |

| Partial release of mortgage (Form 236, if mortgaged) | No | Required | Without it, the sale can trigger the due-on-sale clause |

| State vacant-land disclosure form (where one exists) | Not applicable, house disclosure rules apply | Required in states with a separate land form | Wisconsin, for example, requires a distinct Vacant Land Disclosure Report under Wis. Stat. §709.033, separate from its residential condition report |

| Septic or well easement | Not applicable if the system stays on one lot | Required if the system serves both resulting lots | County health departments generally require a recorded easement before approving a split that separates a system from its lot |

- Splitting before securing lender consent. The seller lists the land, finds a buyer, and only then discovers the due-on-sale clause applies.

- Pricing land using house-sale comps. Land pricing has no clean comparable set the way a house does; using nearby home sales as a proxy overprices or underprices the parcel.

- Ignoring septic or well continuity. A split that strands a shared system on the wrong parcel can stall closing for months while an easement gets negotiated and recorded.

- Missing the 2-year window for the tax exclusion. Selling the land and the house more than 2 years apart forfeits the combined exclusion treatment entirely.

Most of these mistakes surface at closing, not at listing.

Leave a Reply