Can foreigners legally buy a house in Mexico

Article 27 of the Mexican Constitution restricts direct foreign ownership within 100 km of a land border or 50 km of a coastline. Outside that band, a foreign buyer signs a waiver, commonly called the Calvo Clause, agreeing to be treated as a Mexican national with respect to that property and to forgo appeal to their home government, filed through SRE under the Ley de Inversión Extranjera. Inside the band, direct ownership isn’t available to individuals; a Mexican bank instead holds title in trust for the buyer, who keeps full use, rental, sale, and inheritance rights over the property.

Do I need Mexican residency to buy a house?No. Eligibility runs on the restricted-zone rule and the SRE filing, not on visa or residency status.

Restricted-zone status of popular target markets

| City / area | Zone status | Structure required | Source |

|---|---|---|---|

| Cancún, Playa del Carmen, Tulum | Restricted (coastal) | Fideicomiso | SRE, Art. 27 rule |

| Puerto Vallarta, Los Cabos, Mazatlán | Restricted (coastal) | Fideicomiso | SRE, Art. 27 rule |

| Tijuana, Ciudad Juárez | Restricted (border) | Fideicomiso | SRE, Art. 27 rule |

| Mexico City, Guadalajara, San Miguel de Allende, Querétaro | Outside restricted zone | Direct title with SRE waiver filing | SRE, Art. 27 rule |

The zone rule, not the city’s reputation or price point, is what decides which paperwork applies; several inland colonial-era cities that read as “off the beaten path” sit outside the zone entirely, while some inland border cities fall inside it.

Which ownership structure fits your situation

The fideicomiso, a corporation, and direct title solve different problems, and the right one depends on what the property is for.

| Buyer intent | Recommended structure | Why |

|---|---|---|

| Vacation home, restricted zone | Fideicomiso | Full personal-use and inheritance rights; renewable past 50 years |

| Vacation home, outside restricted zone | Direct title with SRE waiver | No trust bank, no annual trustee fee |

| Single rental property, restricted zone | Fideicomiso | Rental income and eventual resale both flow through the same trust |

| Multiple rental units or commercial-scale operation | Mexican corporation with foreign-admission clause | Regulatory carve-outs exist for non-residential use inside the restricted zone |

Is buying safer than renting first?Renting through one full seasonal cycle before committing surfaces issues, flooding, road access, HOA quality, that a single viewing trip won’t. Nothing in Mexican law penalizes waiting.

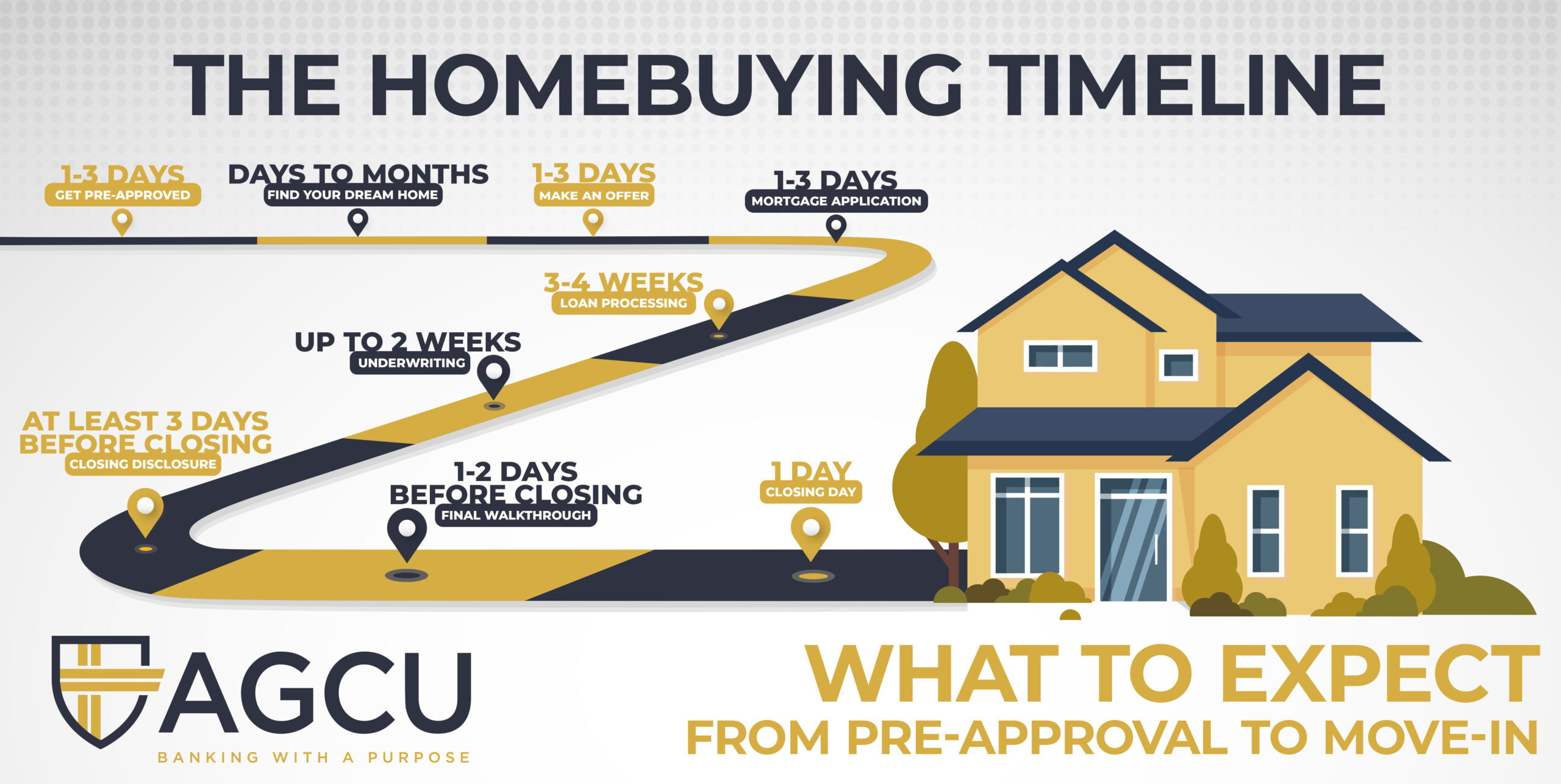

Step-by-step: how the purchase works

| Step | Responsible party | Typical timeframe | Documents | Common mistake |

|---|---|---|---|---|

| Signed offer / promise-to-purchase | Buyer, seller | 1 to 2 weeks | Contrato de promesa, earnest deposit | Skipping a written contract in favor of a verbal deal |

| Title and lien search | Notario público | 1 to 3 weeks | Certificado de libertad de gravamen, escritura history | Trusting the seller’s word instead of an independent search |

| Fideicomiso permit filing (restricted zone only) | Bank fiduciary, via SRE | About 5 business days once filed | Fideicomiso application data | Confirming zone status only after making an offer |

| Deed signing before a notary | Notario público | Varies by state and notary backlog | Escritura pública | Not separating notary fees from the acquisition tax in the budget |

| Public registry recording | Registro Público de la Propiedad | Weeks to months, state-dependent | Escritura, payment receipts | Assuming the deal is finished at signing rather than at registration |

The only step with a government-stated turnaround is the SRE filing itself; every other timeframe depends on the notary and the state registry involved, which is why a written, notary-specific schedule matters more than any national average.

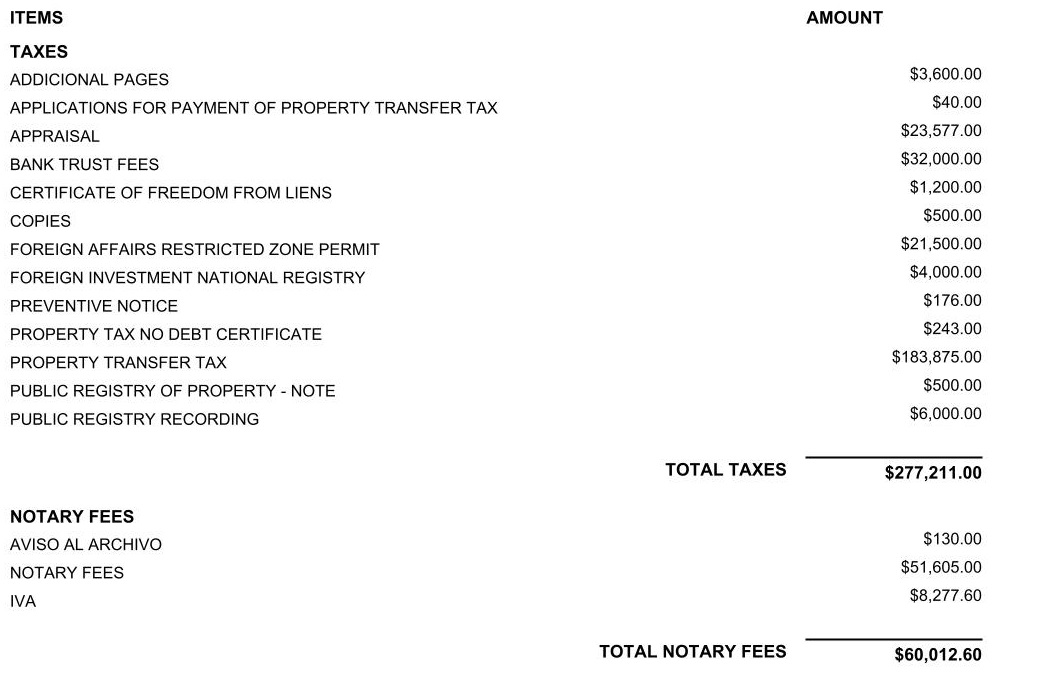

What it costs to buy and hold

| Item | Who pays | When due | What’s known |

|---|---|---|---|

| SRE permit / fideicomiso setup | Buyer | At trust formation | Fee set annually in the SAT’s Resolución Miscelánea Fiscal, Anexo 19; ask your notary for the current published amount |

| Notary fees | Buyer, customary | At signing | Set by each state’s notary tariff; get it itemized in writing before signing |

| Acquisition tax (ISAI) | Buyer | At signing | A state-level percentage of the appraised or transaction value; varies by state legislation |

| Annual fideicomiso trustee fee | Buyer | Yearly | Charged by the trustee bank; compare fee schedules before choosing a trustee |

| Rental income tax | Owner | Filed with rental income | 25% ISR withholding on gross rents for nonresidents, per current guidance; a net-basis election is available with a valid RFC |

Financing a Mexican property as a foreigner

Foreign buyers can borrow from Mexican banks, though qualifying documentation and down payments are more demanding than for Mexican residents. As one dated reference point, BBVA’s Hipoteca Fija product carried a calculated annual cost of 13.2 percent against a nominal rate of 11.20 percent, calculated Feb. 27, 2026 and valid through Aug. 26, 2026. The two-point gap between the advertised rate and the real cost shows up in nearly every Mexican mortgage quote, not only this one.

Can I get a mortgage in Mexico, or should I finance from home?Both exist. A home-country cash-out refinance or HELOC is often cheaper than a Mexican peso mortgage once the rate gap above is priced in, but it exposes the loan to currency risk if your income is in a different currency than the loan.

Wiring funds across the border adds a cost most buyers never separately account for: bank wire fees plus the spread between the mid-market exchange rate and the rate the sending or receiving bank actually applies. On a six-figure transaction, that spread alone commonly outweighs the wire fee itself.

Red flags and disqualifiers

Ejido land is communal agrarian land, and it cannot be individually deeded and sold until it has gone through a formal desincorporación process administered by Mexico’s Registro Agrario Nacional. A parcel that hasn’t completed that process cannot legally pass to an individual buyer, foreign or Mexican.

| Warning sign | What it usually means | What to do instead |

|---|---|---|

| Seller offers a private contract with no notario involved | The transfer may not be registrable; ejido status is a common reason | Insist on a notario-verified title search before any deposit |

| Price is markedly below comparable listings, no stated reason | Possible ejido status, unresolved inheritance dispute, or lien | Request the certificado de libertad de gravamen directly, not through the seller |

| No RFC or Mexican tax paperwork trail from the seller | Complicates your own future capital-gains basis at resale | Get the seller’s documentation before, not after, signing |

| Property sits within a coastal federal maritime-terrestrial zone (zofemat) | A portion of the lot may not be privately titleable at all | Verify the exact boundary with a licensed surveyor before making an offer |

What is ejido land and how do I spot it before I make an offer?Ask for the escritura pública and the certificado de libertad de gravamen up front. Land still under ejido or communal status will not have either.

Taxes: buying, owning, and renting

Predial, the annual property tax, applies regardless of nationality and is set by each municipality’s cadastral value. This is genuinely a municipal figure, not a national one, so the honest answer for any specific property is: ask the municipal treasury office for the current predial notice on that parcel, and treat any nationwide percentage you’re quoted as a rough starting point.

Selling as a foreign owner

At sale, a nonresident chooses between two ISR calculations, and the notary calculates both before withholding: 25 percent of the gross sale price with no deductions, or an elective 35 percent of the net gain, where the original acquisition cost is adjusted upward using Mexico’s INPC inflation index before the gain is computed, per International Tax Review’s analysis of the Mexican Income Tax Law. The second method commonly produces a lower tax bill when the owner has documented the original purchase price and any improvements with valid CFDI invoices; without that documentation, the notary defaults to the 25 percent gross method.

What happens to my fideicomiso if I never become a resident?Nothing changes. The trust is a property-holding vehicle tied to the real estate, not to the beneficiary’s immigration status, and it continues, and can be renewed past 50 years, regardless of residency.

This is also where Canadian buyers diverge from the US-centric framing most guides default to: Canada does not carry the same foreign tax credit mechanics as the US on a foreign real estate gain.

Working with an agent

AMPI, Mexico’s national real estate association, founded in 1956, offers CONOCER/SEP-accredited competency certifications, including one specific to real estate advisory in tourist zones (EC0277). An AMPI-affiliated agent operates under a written code of ethics and is affiliated internationally with the US National Association of Realtors and FIABCI. Ask any agent representing you on a cross-border deal for their AMPI membership status directly.

Insurance and ongoing costs

Property insurance is available from both Mexican insurers and cross-border providers serving foreign owners, and coastal properties carry a different risk profile than inland ones. Reliable, current premium figures broken out by coastal versus inland zone weren’t something this research turned up from a primary, citable source, so rather than repeat an unverified number: request quotes from at least two insurers once you have a specific address, since the swings by zone are large enough that a single national figure isn’t something a guide can responsibly state.

Leave a Reply