What Homes Cost, Region by Region

| Region | Typical price per m² | Nearest airport | Note |

|---|---|---|---|

| Santo Domingo (Piantini, Naco, La Esperilla) | DOP 140,000 to 190,000 (~$2,400 to $3,200) | SDQ, in-city | Urban demand, no coastal-setback exposure |

| Punta Cana / Bávaro / Cap Cana | $1,980 to $3,500 (apartments); villas from $450,000 | PUJ, 15 to 45 min | Coastal construction falls under maritime public-domain setback rules |

| Las Terrenas / Samaná | $725 to $1,125 (custom-build cost per m²) | AZS (El Catey), ~20 min | Hillside lots (Cosón) versus beachfront (Playa Bonita) carry different flood exposure |

| Cabarete / Sosúa / Puerto Plata | $1,200 to $2,400 | POP, 15 to 30 min | Older gated communities show wide HOA-quality variance |

These figures come from cross-referenced real-estate market analysis, not a government price index. No verifiable national statistics-office series could be confirmed for this page, so treat the ranges as directional rather than exact, and confirm current asking prices with at least two independent local agencies before budgeting.

Título de Registro vs. Constancia Anotada

The Dominican Republic’s own land registry, the Registro Inmobiliario, draws a hard line between two documents. A Certificado de Título, printed on blue paper, certifies full ownership of a specific, individually surveyed parcel. A Constancia Anotada, printed on pink paper, certifies a right to a certain number of square meters within a larger, undivided parcel that has not yet been through deslinde, the formal surveying process that separates it into its own registered lot. You can own meters. You do not yet own a bounded piece of land.

This is not a technicality. A Constancia cannot be legally sold or subdivided until the deslinde is completed, and disputes over undivided parcels are a recurring source of Dominican property litigation. Before signing anything, request a current Certificación de Estado Jurídico directly from the Registro Inmobiliario: a copy the seller hands you proves nothing about liens or encumbrances recorded since it was issued.

What’s the real difference between a Título and a Constancia?A Título de Registro is full ownership of a surveyed, individually registered parcel. A Constancia Anotada is a share of an undivided parcel, not yet separated by deslinde; it cannot be transferred or split further until that survey is completed and registered.

The Legal and Tax Mechanics of a Purchase

Deslinde and the Promise-of-Sale Contract

Deslinde is the licensed survey that converts a Constancia into a proper Título; without it, ownership stays provisional. Most deals begin with a notarized Contrato de Promesa de Venta, which fixes price and terms before the final deed transfer.

Transfer Tax, IPI, and CONFOTUR

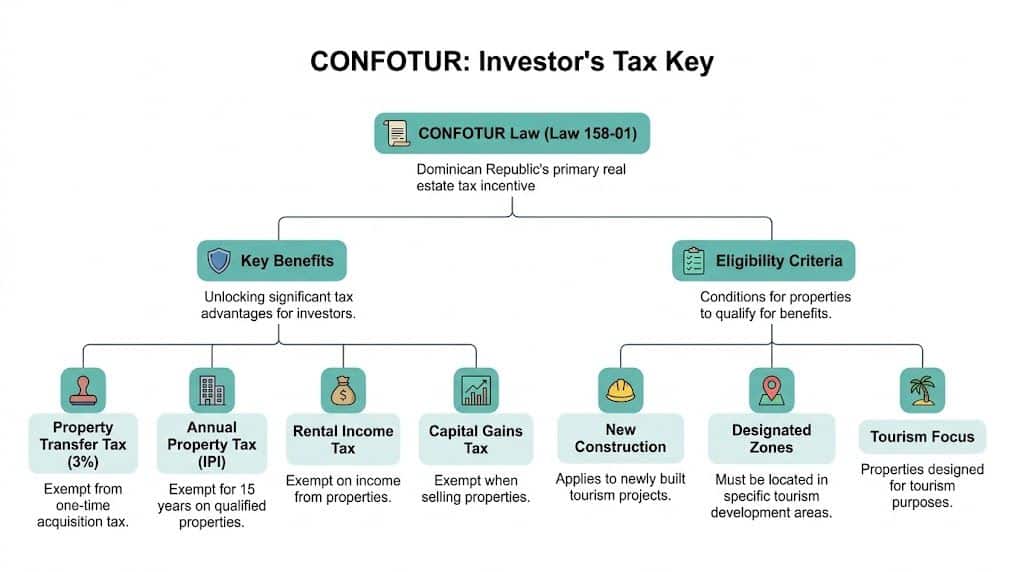

The one-time transfer tax is 3% of whichever is higher, the DGII-appraised value or the purchase price, under Law 288-04. On a $300,000 property that is $9,000. The annual IPI is 1%, but only on the portion of a property’s assessed value above the 2026 threshold of RD$10,695,494, about $182,200, set under Law 18-88 as amended by Law 253-12, and confirmed on the DGII help portal. It is paid in two installments, due March 11 and September 11. A property under that threshold owes no annual tax at all. CONFOTUR, the tourism-incentive law (Law 158-01), waives both the transfer tax and the IPI for qualifying certified projects for a fixed exemption period; the resale of a CONFOTUR-certified unit can carry its remaining exemption years to the new buyer, a real liquidity edge over a non-certified equivalent.

| Tax | Rate | Applies to | Authority |

|---|---|---|---|

| Transfer tax | 3%, one-time | Higher of DGII value or price | DGII, Law 288-04 |

| IPI (annual) | 1% on excess above threshold | Value above ~$182,200 (2026) | DGII, Law 18-88/253-12 |

| CONFOTUR exemption | 0% on both above | Certified tourism projects | MITUR/CONFOTUR, Law 158-01 |

| Inheritance tax | 3% residents / 4.5% non-residents | Net inherited value | Dominican Civil Code, DGII |

The tax bill on a mid-size purchase is predictable and modest by North American standards; the harder cost to plan around is the title-type risk described above, which no tax rate captures.

Inheritance and Forced Heirship

Dominican succession law follows forced heirship (reserva hereditaria): children hold a protected share of an estate regardless of what a will says, and a surviving spouse typically receives only a usufruct, the right to use the property, rather than an ownership share. A foreign owner’s home-country will is not automatically enforceable; without a Dominican-compliant will naming the applicable law, local succession rules can override stated wishes. Inheritance tax runs 3% for residents and 4.5% for non-residents on the net estate value.

How much of the purchase price goes to taxes and fees at closing?Budget roughly 4% to 9% of the purchase price beyond the sticker figure: the mandatory 3% transfer tax, plus legal, notary, and registry fees that widen with title complexity and translation needs. CONFOTUR-certified purchases skip the transfer tax entirely.

Financing a Purchase From Abroad

Most Dominican property sales close in cash; local financing exists but on notably different terms than a US or Canadian mortgage. Banks including Banreservas, Banco Popular, Scotiabank, BHD León, and APAP lend to non-residents, but expect a larger down payment and a shorter, pricier loan.

| Lender type | Typical down payment | Rate range | Loan currency | Term |

|---|---|---|---|---|

| Dominican bank, USD loan | 30% to 50% | 8% to 10% | USD | 15 to 20 years |

| Dominican bank, DOP loan | 30% to 50% | 11% to 14% | DOP | 15 to 20 years |

| Developer financing (pre-construction) | 10% to 30% | Often above bank rates | Usually USD | Short, to completion |

| Home-country HELOC / refinance | Varies by home equity | Roughly 7% to 9% (US rates) | Home currency | Varies |

A DOP-denominated loan means your payment moves with the peso. As of July 10, 2026, the Banco Central’s official reference rate stood at RD$58.4754 per dollar to buy and RD$58.8724 to sell; that rate drifts with tourism receipts, remittances, and US monetary policy, so a mortgage priced in pesos carries real currency exposure over a 15-year term that a USD-denominated loan avoids.

Can I finance this from outside the country?Yes, through a Dominican bank (30% to 50% down, 8% to 14% depending on currency), developer financing on pre-construction units, or by borrowing against home-country equity and buying in the DR as a cash buyer, often the cheapest of the three.

Common Mistakes and How Buyers Lose Money

- Paying a deposit before verifying title. Legitimate sellers have nothing to hide; a request for money before you can independently pull a Certificación de Estado Jurídico from the Registro Inmobiliario is the clearest warning sign available.

- Accepting a Constancia Anotada without understanding it. It is not full title until deslinde is complete and registered.

- Assuming a signed contract equals ownership. Rights become enforceable against third parties only once the transfer is registered at the Registro Inmobiliario, not at signing.

- Skipping an independent survey on land purchases. Boundary overlaps between registered parcels are a known and recurring dispute source.

- Underestimating pre-construction default risk. If a project stalls, financing collapses, or the underlying land is held by an unrelated title-holder through a lease or option, an investor’s claim may run against a developer with no assets to satisfy it.

An industry-tracking estimate, referencing a documented Pro Consumidor fraud case, puts fraud exposure at roughly 5% to 8% of foreign-buyer transactions. Treat that as a directional industry estimate, not a government statistic, since no primary regulator figure could be confirmed.

What’s the most common way buyers lose money here?Paying toward a property before an independent title search, most often on a Constancia Anotada or a pre-construction unit tied to an undeveloped Promise-of-Sale, without confirming who actually holds the registered land.

Choosing a Region by Buyer Type

| Buyer profile | Fitting property type | Fitting region | Main risk |

|---|---|---|---|

| First-time / rental income seeker | Entry-level apartment, 90 to 130 m² | Punta Cana, Bávaro | Oversupply in some new towers |

| Family relocating full-time | 3+ bedroom villa or townhouse | Santiago, Las Terrenas, Santo Domingo suburbs | HOA and school-access variance |

| Income-producing small asset | Small boutique rental or multi-unit | Cabarete, Sosúa, Las Terrenas | Management-quality dependency |

| Custom-build / long-horizon investor | Raw land, deslinde-completed | Samaná hillsides, Puerto Plata interior | Construction-cost inflation, permitting timelines |

The nearer to a beach, the higher the entry price, and the more the property depends on tourism cycles for its rental case; the persona-to-region fit matters more than any single town’s reputation.

Which region fits a first-time buyer versus an investor?A first-time or rental-income buyer is usually best served by an established Punta Cana or Bávaro apartment with existing rental-management infrastructure. An investor comfortable with more operational involvement gets more yield potential from a smaller boutique asset in Cabarete or Las Terrenas.

Is the Investment Case as Strong as the Numbers Suggest

The Dominican Republic’s Ministry of Tourism reported a provisional record of roughly 11.6 to 11.7 million total visitor arrivals, air and cruise combined, for 2025, above 2024’s confirmed 11.19 million, itself a record at the time. That growth is real and dated to an official source.

Tourism volume supports the rental case in broad terms. It does not tell you what a specific unit will earn.

Leave a Reply