Search current NYC condo listings

Live inventory changes hourly, so this page points you to filterable search rather than trying to replicate it. Use the search tool above to set price, neighborhood, and bedroom filters, then come back to the sections below before you write an offer.

Condo or co-op? What changes before you search

New York is unusual: a large share of “apartments for sale” listings are co-ops, not condos, and the two are different transactions with different rules on financing, approval, and resale flexibility.

| Factor | Condo | Co-op |

|---|---|---|

| Financing | Standard mortgage secured by a deed to real property | Board-set debt-to-income and post-closing liquidity rules; loan secured by shares, not real property |

| Board approval | Usually none; buildings often hold only a right of first refusal | Full board interview and approval, which can be denied without a stated reason |

| Subletting | Generally unrestricted, sometimes with a registration fee | Often capped at one to two years within every five, or banned outright (Manhattan Real Estate Market 2026 analysis) |

| Foreign or LLC ownership | Permitted; LLC and trust purchases are common | Frequently restricted or barred by the proprietary lease |

| Typical closing speed | Faster, often 30 to 60 days | Slower, often 60 to 90+ days once board review is added |

A buyer searching specifically for a condominium, rather than any apartment, is very often trying to avoid exactly what sits in the co-op column: board discretion, subletting limits, and LLC restrictions. That distinction is worth resolving before you filter by price.

Is a condo or co-op better for a foreign buyer or an LLC purchase?Condos are almost always the workable path. Co-op boards can and do reject buyers who purchase through an entity or who won’t disclose beneficial ownership, and many proprietary leases prohibit it outright. Condos carry no such board discretion.

What a condo costs beyond the listing price

| Cost | Typical range | Who pays | When it applies |

|---|---|---|---|

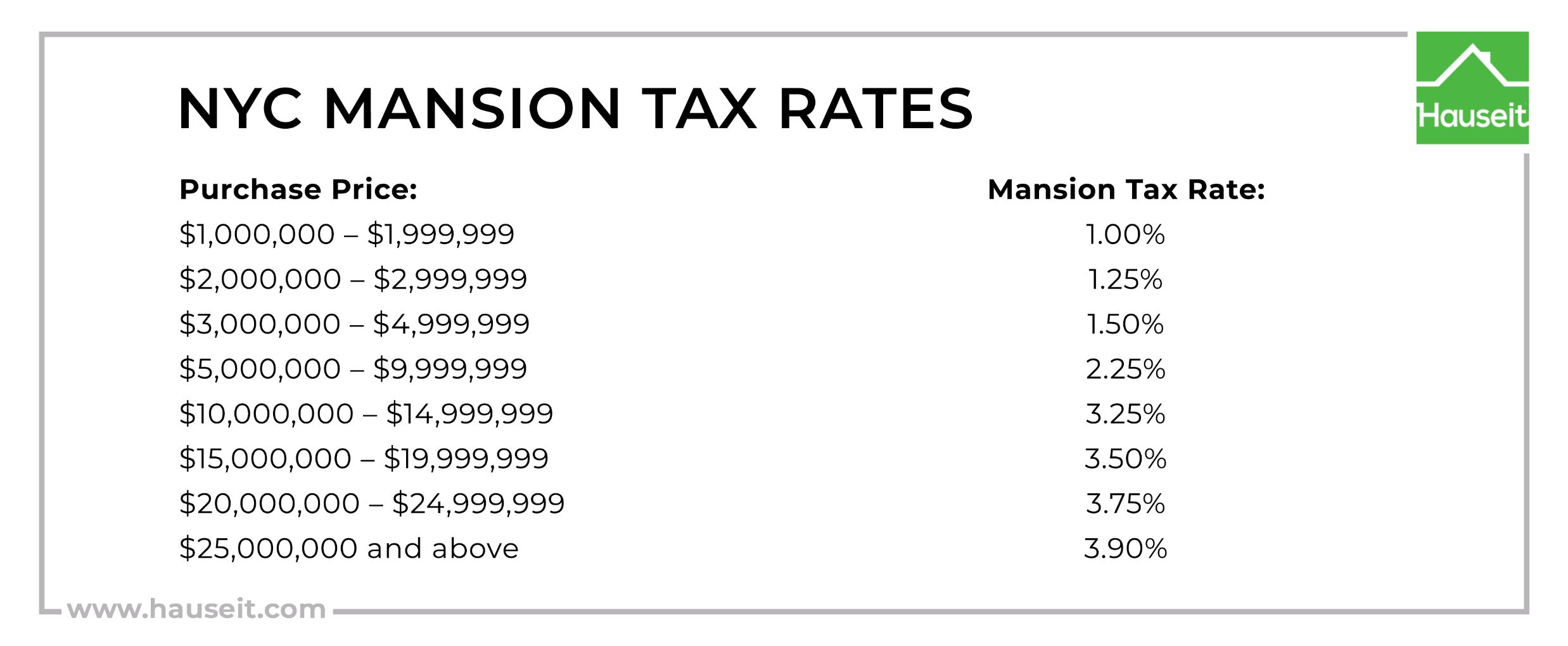

| NYS mansion tax | 1% at $1M, rising in tiers to 3.9% at $25M+, applied to the whole price at each tier | Buyer | Any residential purchase of $1M or more (NYS Department of Taxation and Finance) |

| NYC Real Property Transfer Tax | 1.00% up to $500,000; 1.425% above $500,000 | Seller by default, occasionally shifted by contract | Every sale, regardless of price (HelpNewYork RPTT guide) |

| Mortgage recording tax | 1.8% of the loan under $500,000; 1.925% at $500,000 or more | Buyer, only if financing | Condos and houses; co-ops are exempt because a co-op loan is secured by shares, not a recorded mortgage (PropertyClub) |

| Condo-vs-co-op financing gap | Roughly 2% of the loan amount saved by buying a co-op instead of a condo | N/A | Whenever the two property types are being compared side by side |

The mansion tax is not marginal: a purchase at $2,999,999 owes 1.25% of the entire price, and two dollars more crosses into the 1.5% tier (Reed Corp CPA). Buyers negotiating near a threshold routinely structure the price just under the line rather than absorb the jump.

The number sponsor listings don’t show you

New-development condos frequently carry a 421-a or 485-x property tax exemption that phases out over the building’s remaining term, often stepping the tax bill up by around 20% every two years in the back half of the schedule (Miltoncoste.com). The 421-a program stopped accepting new applications in June 2022, so this affects resale and near-complete new-construction listings, not future ground-up projects. One brokerage analysis, citing the city’s Independent Budget Office, estimates that Manhattan condo buyers pay roughly 0.43% of the sale price for each remaining year of 421-a benefit still attached to the unit (Manhattan Miami). The listing’s advertised monthly tax figure reflects this year’s abated number, not what the unit will carry once the phase-out completes; ask for the building’s actual abatement certificate and remaining schedule ahead of an offer.

Why do new-development listings sometimes show unrealistically low property taxes?Because the abatement hasn’t finished phasing out yet, and because sponsor units in newly filed offering plans can also qualify for a streamlined FHA Single Unit Approval before the building itself is separately certified, a detail that changes the financing math independently of the tax question. Request the phase-out schedule and the offering plan’s financing terms before you calculate long-term carrying cost.

Before you make an offer: what the listing won’t tell you

No amount of filtering on price or square footage surfaces a building’s financial health. Four checks matter more than most buyers realize:

- Reserve fund balance. New York has no statewide legal minimum reserve requirement for condo or co-op associations; the only mandatory reserve rule applies at the moment a building is first converted from rental to condo (NYC Admin Code §26-703). Ask the board for the current reserve balance and the most recent reserve study, if one exists.

- HPD and DOB violation history. Search the building’s address on NYC HPD’s Online Registration and Complaint System and the DOB Building Information Search for open violations and inspection history ahead of an offer.

- Pending litigation. Ongoing lawsuits involving the HOA, especially anything touching safety or structural conditions, can make a building non-warrantable outright (Newrez).

- Managing agent licensing. A managing agent with a clean, current license is a small but checkable signal of building administration quality.

A 66-unit West Village co-op offers a real-world sense of scale: in February 2025 its board launched a 12-month, $8 million special assessment, averaging roughly $100,000 per apartment, to cover facade repairs after depleting its reserves (Habitat Magazine). There is no legal cap on how large a special assessment can be.

What is a special assessment, and can I find out about one before I buy?It’s a one-time bill the board issues when reserves and monthly charges don’t cover a major cost, with no dollar cap in New York. Ask directly for the last five years of assessment history, not just the current reserve balance; boards are not obligated to volunteer either one.

Financing eligibility narrows what you can actually buy

Not every condo qualifies for FHA, VA, or standard conventional financing. Lenders and the government-sponsored entities require roughly 10% of the building’s annual budget held in reserves, cap how many units a single entity can own, limit the share of units 60 or more days delinquent on common charges to about 15%, and generally disqualify buildings involved in active non-routine litigation (Homebuyer.com). A building failing any of these tests is “non-warrantable,” meaning low-down-payment financing disappears and buyers are pushed toward larger down payments or specialty lenders. HUD maintains a searchable FHA-approved condo list that’s worth checking on the way into a building tour, not on the way out.

Does every NYC condo qualify for an FHA loan?No. A building must appear on HUD’s approved list or pass a Single Unit Approval review, and it must meet reserve, delinquency, and litigation thresholds. Confirm status before assuming FHA financing is available for a specific building.

Browse by borough and neighborhood

- Manhattan – the highest median prices and the deepest concentration of legacy 421-a buildings still working through their phase-out schedules.

- Brooklyn – a wider mix of pre-war conversions alongside new construction, with more active co-op board approval processes than Manhattan’s condo-heavy new-development corridors.

- Queens – Long Island City carries the city’s largest concentration of 421-a-benefited condos, per closing-cost specialists who track the program (Gadura Real Estate).

- The Bronx and Staten Island – the smallest condo inventories of the five boroughs, with correspondingly less exposure to sponsor-unit financing quirks and tax-abatement phase-outs.

Leave a Reply