What You’re Actually Deciding

A Florida condo purchase is really two purchases layered together: the unit, and a fractional stake in a corporation that may owe money it hasn’t told you about yet. The price on the listing describes the first. Almost every serious risk in this guide comes from the second.

The Document Timeline: What You Get, When, and How Long You Have to Cancel

Florida resale contracts run on two separate clocks, and confusing them is the single most common way buyers lose cancellation rights they thought they still had. The general document-review window is now seven business days, not three, for contracts dated July 1, 2025 or later (Carlos M. Amor). A second, separate three-business-day window applies specifically to milestone inspection, SIRS, and turnover reports if those are requested and not already delivered (Barnes Walker). New-construction purchases run on a different statutory track entirely, with a longer developer-disclosure period (Million Luxury).

| Document | Who provides it | Window | What it protects |

|---|---|---|---|

| Resale disclosure package (declaration, bylaws, budget, minutes) | Seller, at seller’s expense if requested | 7 business days to cancel after signing and receipt | Financial and governance review |

| Milestone Inspection / SIRS / Turnover reports, if requested | Seller/association | 3 business days to cancel after receipt | Structural-risk review |

| New-construction developer disclosure | Developer | Longer statutory period under §718.503, separate from resale rules | Pre-construction contract protections |

| Association approval or right-of-first-refusal decision, if applicable | Association | Set in the contract rider; contract terminates and deposit returns if unmet | Buyer-approval risk |

The two resale windows do not run together automatically: a buyer who receives the general disclosure package on day one and the milestone report on day five still has three fresh business days from day five to review that specific report.

Can I back out after reviewing the condo documents? Yes, within the applicable window: seven business days for the general resale package, three for milestone, SIRS, or turnover reports specifically, each counted in business days from receipt, not from signing.

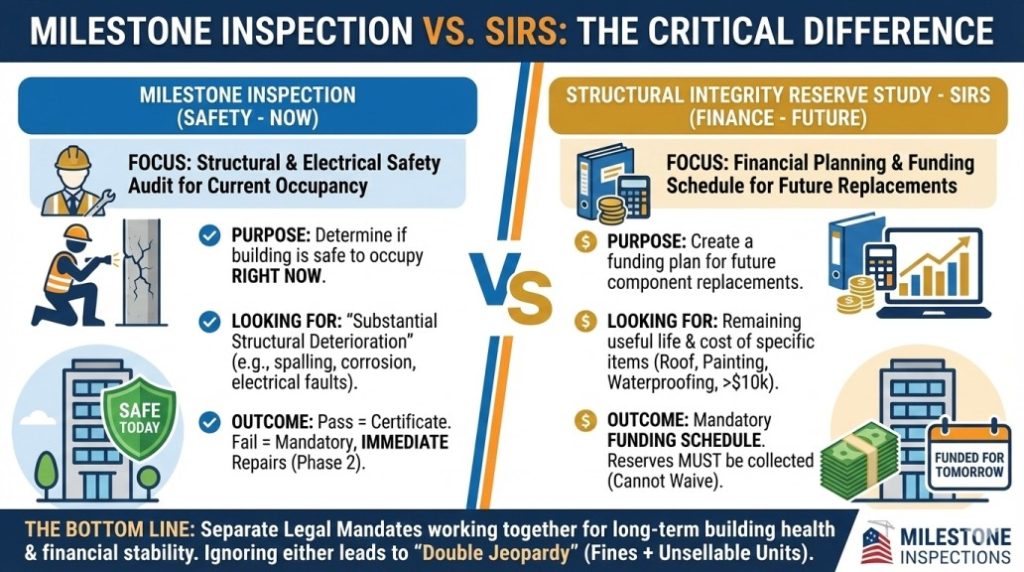

Milestone Inspections and SIRS: What They Cost If the Building Is Behind

Every condominium or cooperative building three or more habitable stories must complete a Milestone Inspection by December 31 of the year it turns 30 (or 25 if it sits within three miles of the coast, at local discretion), and again every ten years after that (Fla. Stat. §553.899). A related but separate requirement, the Structural Integrity Reserve Study, applies to the same buildings and must be completed at least every ten years, funding the reserves for eight specific structural components (Fla. Stat. §718.112(2)(g)). Associations that existed before July 1, 2022, and are unit-owner controlled had their initial SIRS deadline extended to December 31, 2025, under HB 913.

| Requirement | Trigger | Not required if | Statute |

|---|---|---|---|

| Milestone Inspection | Building 3+ habitable stories, age 30 (25 if coastal) | Building under 3 habitable stories | §553.899 |

| SIRS | Same height threshold, every 10 years | HOA-governed (Ch. 720) properties; buildings under 3 stories | §718.112(2)(g) |

| Combined SIRS/Milestone timing | Milestone due by Dec 31, 2026 | May be done together; SIRS can’t be completed after Dec 31, 2026 either way | §718.112(2)(g)(7) |

What this actually costs when a building is behind is not abstract. At the Cricket Club in North Miami, deferred maintenance led to special assessments as high as $134,000 per unit in 2024; at Mediterranean Village in Aventura, some owners were assessed up to $400,000 (Building Mavens). Those are outliers, not a forecast for every older building, but they show the actual range a buyer is underwriting when a reserve study is thin or absent.

Who Pays for a Special Assessment Already on the Books

The current condominium rider (CR-7 Rev.) requires the seller to represent whether they’re aware of any special assessment levied, reported in board minutes within the twelve months before the contract, or already in progress, and the rider now carries three separate checkboxes addressing different assessment scenarios, up from one in earlier versions (Berlin Patten Ebling). The mistake buyers make most often is assuming a seller’s clean disclosure means no exposure. It doesn’t. The seller’s representation only covers what was reported in minutes within that twelve-month window: an assessment discussed informally, or one the seller simply didn’t attend a meeting to hear about, isn’t covered by the representation and isn’t the seller’s liability to disclose.

| Assessment status at contract | What the seller must disclose | Who typically bears it |

|---|---|---|

| Already levied and fully paid by seller | Confirmed at closing via association estoppel | No buyer liability |

| Levied, with installments remaining | Per the rider’s checkbox election for that transaction | Depends on the specific box checked; verify with the estoppel certificate, not the rider alone |

| Discussed in minutes within 12 months, not yet levied | Seller must disclose if aware | Whoever owns the unit when the board actually levies it, buyer included if that happens post-closing |

| Discussed outside the 12-month window or not in minutes at all | Not covered by the seller’s representation | Buyer, with no recourse against the seller |

The recurring error is treating the estoppel certificate as optional. It’s the one document that states, as of a specific date, exactly what’s owed and what’s pending, and it supersedes the rider’s representations for anything that’s happened since the contract was signed.

Who pays if a special assessment is levied right before closing? It depends on the timing rule the rider selects for that transaction and on when the assessment was formally approved under the association’s governing documents, not on when the buyer or seller first heard about it. Request a current estoppel certificate close to closing rather than relying on the contract-stage disclosure alone.

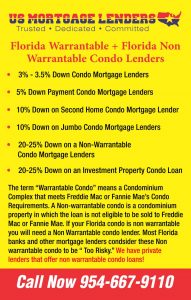

Financing: Warrantable vs. Non-Warrantable Under the 2026 Rules

A condo unit can be fairly priced and still be difficult to finance if the building itself fails project review. Fannie Mae’s Lender Letter LL-2026-03, issued March 18, 2026, rewrote several of the rules that determine this (Fannie Mae).

What “Non-Warrantable” Means

A warrantable building meets Fannie Mae and Freddie Mac project standards: roughly 50% owner-occupancy, no single entity owning more than 10% of units, adequate reserves, and master insurance that covers the required perils (Reach Home Loans). A non-warrantable building isn’t unfinanceable, but it moves buyers into portfolio or non-QM loans with larger down payments and higher rates.

Rules That Changed in 2026

Effective July 1, 2026, Fannie Mae caps the per-unit deductible on a Florida condo’s master property insurance policy at $50,000 for all required perils; a building whose master policy exceeds that on wind or water coverage loses conventional eligibility until the policy is restructured. A 15% minimum reserve-funding requirement takes effect for loan applications dated January 4, 2027 or later. Limited Review, the faster approval path many smaller Florida buildings relied on, is retired for all applications dated August 3, 2026 or later, pushing more buildings into full documentation review. Working in buyers’ favor, the 50% investor-concentration cap for established projects under Full Review was dropped immediately upon the letter’s release, and Florida’s separate PERS review requirement for new and converted attached condo projects was retired the same day.

Why would a lender reject a condo I can otherwise afford? Because project review evaluates the building, not just the borrower: owner-occupancy ratio, reserve funding, insurance deductibles, and pending litigation can all sink a loan file even when your income, credit, and down payment are fine.

New Construction vs. Resale: Different Rules, Different Risks

Developer sales and resale purchases run on separate statutory tracks. New-construction buyers get a longer, developer-specific disclosure and rescission period under §718.503, distinct from the seven-day resale window above, and the developer carries different disclosure obligations than a private seller does (Million Luxury). The turnover inspection report, the developer’s structural handoff document required once the association transitions to unit-owner control, establishes the baseline condition a new board inherits, and functions as the closest thing a new-construction buyer has to a Milestone Inspection before one is legally required. Resale buyers, by contrast, inherit whatever the association’s financial and structural history actually is, which is exactly why the document timeline and special-assessment sections above carry more weight on a resale purchase than on a new-construction one.

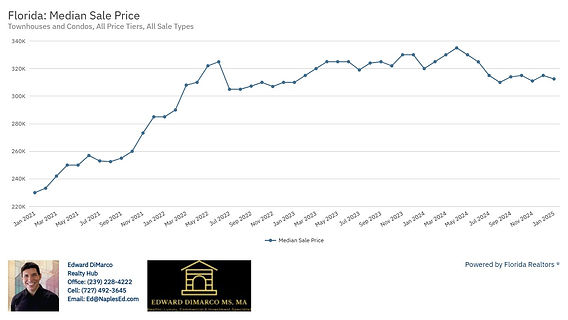

Real Costs by Region

Statewide, the condo and townhouse median sale price was $315,000 in April 2026, flat year over year, with 8.9 months of supply, down from 10.3 months a year earlier, still a buyer-favorable market despite tightening from 2025 (Florida Realtors). HOA dues vary sharply by metro and building type:

| Metro | Typical condo HOA fee (monthly) | Note |

|---|---|---|

| Miami-Dade | $835 to $965 | Coastal insurance and mandatory reserves drive the range up |

| Fort Lauderdale | ~$646 | Luxury waterfront towers run well above this figure |

| West Palm Beach | ~$719 | Mix of older and newer coastal buildings |

| Naples | ~$1,000 | Among the state’s highest, tied to luxury amenity load |

| Tampa | ~$655 | Blends downtown coastal condos with inland suburban stock |

| Orlando | ~$490 | Lowest of the six; fewer coastal-insurance pressures |

Regional HOA-fee data: Florida Realty Marketplace, a secondary aggregator without a named primary methodology; treat as directional, not exact, and confirm against the specific building’s current budget.

Insurance is the piece these fee ranges only partly capture, because it’s billed to the association, not the unit owner, and shows up inside the HOA fee rather than beside it. Whole-building master-policy premiums run roughly $15,000 to $50,000 a year for a small inland property, $75,000 to $250,000 for a mid-sized coastal building, and $300,000 to $2 million or more for a large coastal high-rise (FirstService Residential), figures that flow straight into the reserve and dues calculations above.

Rental Restrictions and Investor Considerations

An HOA allowing short-term rentals in its governing documents doesn’t mean the municipality does. City and county short-term-rental ordinances operate independently of condominium association rules, and a unit that’s technically Airbnb-eligible under the declaration can still be non-compliant under local law. This guide can’t currently point to a single, current, statewide-sourced summary of Florida’s short-term-rental preemption status strong enough to cite here; that gap is listed as an open research item rather than answered with a guess. What is verifiable: rental restrictions live in the declaration and bylaws, not in the HOA-fee listing, and lenders reviewing owner-occupancy ratios for warrantability treat heavy short-term-rental activity as an investor-concentration signal, which ties directly back into the financing section above.

Does the HOA allowing Airbnb mean the city does too? No. HOA rules and municipal short-term-rental ordinances are separate legal layers, and a unit can satisfy one while violating the other; check both before assuming a rental strategy is viable.

Common Mistakes and the Limits of This Guide

The pattern across the sections above is timing: two different review windows, a seller representation that only covers a twelve-month slice of history, and a warrantability status that can shift between offer and closing as Limited Review retires in August 2026. Treating any single document as the whole picture is where most of the risk above actually lives.

This guide is not legal, financial, or insurance advice, and figures here reflect published data as of mid-2026. Verify current numbers, deadlines, and building-specific status with a Florida real estate attorney, your lender, and the association directly before relying on them for a purchase decision.

Leave a Reply