If you’re buying to live in it: start with the neighborhood comparison below, then the tax section before you fall for a listing price. If you’re investing: skip to the investor section. If you’re selling in this range: the seller section covers pricing.

What “affordable” costs in Chicago right now

The $420,000 citywide median sits 10% above the U.S. median sale price, per Redfin’s own city-to-national comparison. That figure flattens a market where price per square foot ranges from $128 in Chatham to $303 citywide, and well beyond that on the North Side lakefront. The number that actually matters for a fixed budget is the per-square-foot figure in the specific area under consideration, covered next.

City neighborhoods compared: where the price gaps actually sit

Most Chicago buying guides compare suburbs to each other and never name a city-proper neighborhood at all. Here’s what the city side of that comparison looks like.

| Area | Median sale price | $/sq ft | Change YoY |

|---|---|---|---|

| Chicago (citywide) | $420,000 | $303 | +6.3% |

| Chatham | $256,000 | $128 | +46.9% |

| Austin | $345,000 | $160 | +21.1% |

| Belmont Cragin | $405,000 | $237 | +19.1% |

| Portage Park | $415,000 | not reported | −9.78% |

Source: Redfin Chicago; Redfin Chatham; Redfin Austin; Redfin Belmont Cragin; Redfin Portage Park.

Portage Park, the neighborhood most first-time-buyer guides point to as Chicago’s affordable pick, now sells within $5,000 of the citywide median. Chatham and Austin are the two submarkets that still sell meaningfully under it, though Chatham’s 46.9% year-over-year jump reflects a small, volatile sales volume rather than a stable trend line: worth confirming against a current listing sheet before anchoring a budget to it.

Is a condo a realistic affordable path in Chicago?Often, with a catch. Typical condo HOA assessments run $250 to $800 a month, and roughly 35% of Chicago condo buildings currently carry FHA approval, per a 2026 Chicago condo buying guide, so an FHA-financed condo purchase means checking a building’s approval status before falling for a unit, not after.

The tax variable most guides skip entirely

Chicago’s median effective property-tax rate is 1.66% of market value, lower than Cook County’s overall median of 2.14%, according to Ownwell’s Chicago property tax data. That citywide figure hides real variation: homeowners in ZIP 60624 on the West Side carry a median effective rate of 1.11%, while ZIP 60604 downtown carries 2.20%, a spread of roughly a full percentage point on properties in the same city.

Move outside city limits and the picture often flips. Chicago itself typically runs 1.8% to 2.0%, while Oak Park, Berwyn, and several south suburbs run 2.5% to 3.5% or higher, per JVM Lending’s Cook County tax breakdown. A $300,000 home at 1.1% costs about $3,300 a year in property tax; the same home at 2.5% costs about $7,500. That gap alone can equal or exceed the difference in mortgage payment between two homes priced $50,000 apart.

Does a lower list price always mean a lower monthly payment?No. A home priced $60,000 below another can still carry a higher monthly bill if it sits in a higher-tax pocket. Run the tax line before comparing two listings on price alone.

Down payment and closing-cost programs available now

This is where guides to this topic overlap most closely, and where that overlap is least reliable: program lists written as static miss that assistance runs on annual or bond-cycle funding that opens and closes.

| Program | Administrator | Max amount | Status | Stackable? |

|---|---|---|---|---|

| IHDAccess Forgivable | Illinois Housing Development Authority | $6,000 (4% of price), forgiven over 10 yrs | Open, statewide | Yes, with most local programs |

| IHDAccess Deferred | IHDA | $7,500 (5% of price), deferred until sale/refi | Open, statewide | Yes |

| BNAH | Chicago Dept. of Housing | $100,000, new construction only | Active, but eligible units are currently under construction and not yet listed for sale | Yes, per program terms |

| CHA Down Payment Assistance | Chicago Housing Authority | $20,000 (CHA residents) / $10,000 (others) | Closed: FY funds exhausted Oct. 2, 2025 | Yes; non-CHA combined grants/credits capped at 20% of price |

| HomeGrown Purchase Assistance | Chicago DOH, via NLS/TRP | Up to 25% of purchase price | Open, applications accepted | No: cannot combine with IHDA subsidy programs or TaxSmart MCC |

Sources: IHDA lending programs; City of Chicago BNAH program; CHA Down Payment Assistance; City of Chicago HomeGrown program.

Can BNAH, IHDAccess, and CHA assistance be combined on one purchase?Partially. CHA’s program page states DPA funds can be combined with other down payment help, and IHDA’s programs are generally stackable with local grants. HomeGrown is the exception: NHS Chicago’s published guidance states it cannot be layered with IHDA subsidy programs or the TaxSmart Mortgage Credit Certificate. Confirm the specific combination with a lender before writing an offer around it.

Who these programs work for, and who they rule out

IHDA programs require a minimum credit score and a $1,000 or 1% contribution from the buyer’s own funds. CHA’s non-CHA track caps household income at 80% of area median income and requires an eight-hour HUD-approved homebuyer education course for every person on the purchase agreement, per CHA’s eligibility page. Buying a 2-to-4-unit building under CHA- or NHS-administered programs adds a mandatory landlord training session covering the Cook County Landlords Ordinance, a requirement most first-time-buyer guides never mention because they assume a single-family purchase. USDA financing is unavailable inside Chicago entirely, restricted as it is to eligible rural and suburban tracts.

Do these grant caps and income limits change from year to year?Yes, on separate cycles. IHDA’s dollar caps have held steady across current sources, but CHA’s program runs on an annual funding cycle that can close mid-year, and BNAH’s inventory depends on which new-construction sites are actively under development. Re-verify status at the administering agency’s page before applying.

Reading cheap listings correctly

Chatham’s $128 per square foot against the citywide $303 isn’t purely a location discount. Chicago’s South Side submarkets carry a larger share of pre-1950 bungalow and two-flat stock than the North Side, and a per-square-foot gap this wide, more than half the citywide figure, typically means a meaningful share of that inventory needs roof, electrical, or mechanical work before it’s move-in ready. A $256,000 median doesn’t tell you which side of that line a specific listing sits on; an inspection contingency does. Treat any listing priced well under even Chatham’s own median as a signal to budget for repairs, not as a discovered bargain.

Why do some of the cheapest listed Chicago homes need full rehabs?Because the price-per-square-foot gap between a submarket like Chatham ($128) and the citywide figure ($303) reflects older, often unrenovated housing stock as much as it reflects location. A listing priced well under a neighborhood’s own median is frequently priced that way because of deferred maintenance, not because it’s an undiscovered bargain.

If you’re investing rather than occupying

Down payment assistance programs in the table above generally require owner occupancy for 5 to 10 years, ruling out CHA, HomeGrown, or IHDA assistance on a straight rental purchase. An investor buying in Chatham or Austin at $128 to $160 per square foot is instead weighing acquisition cost against Cook County’s property-tax spread directly: a 1-percentage-point difference in effective rate changes net rental yield more than most renovation-budget line items do. Belmont Cragin’s 19.1% year-over-year appreciation and Austin’s 21.1% both outpaced the citywide 6.3%, worth weighing against each area’s higher starting tax exposure before assuming faster appreciation nets out ahead.

If you’re selling in this price band

Pricing a home in a submarket where per-square-foot values sit far below the citywide figure means comparable sales, not the citywide median, should anchor a listing price. A CMA pulled against citywide numbers will overprice a Chatham or Austin listing and slow the sale.

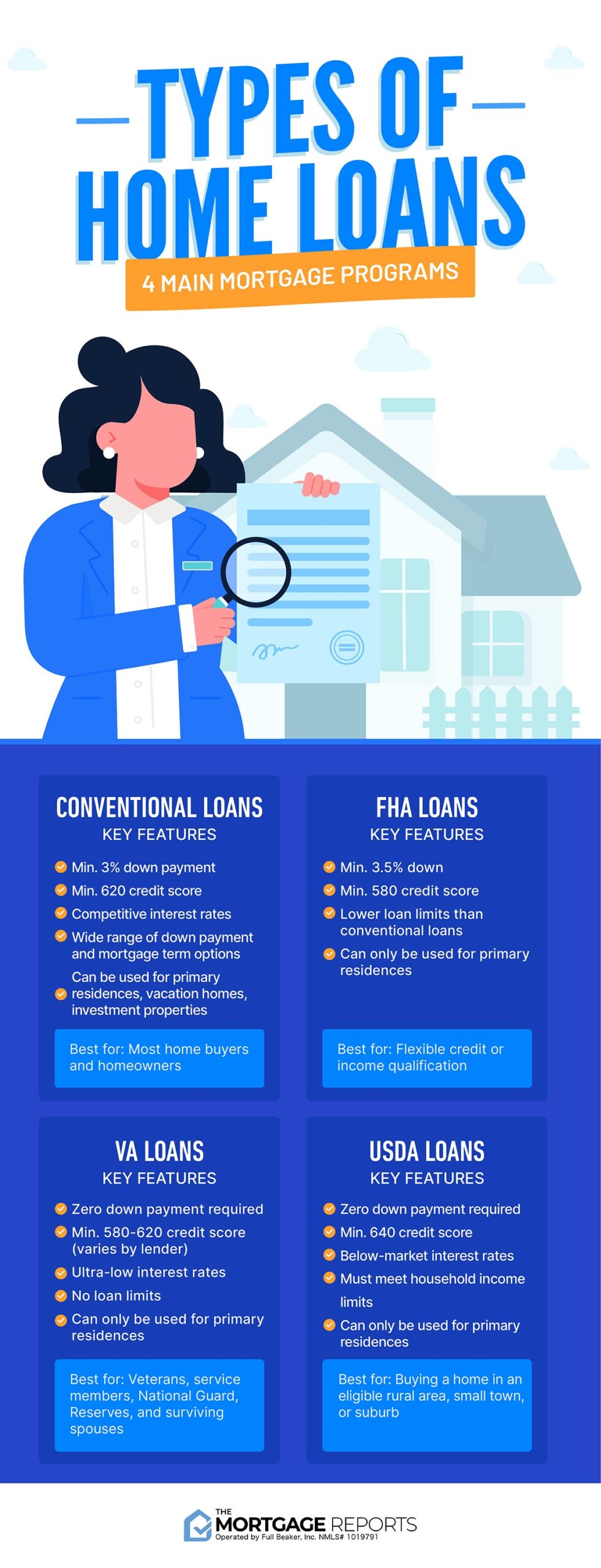

Financing quick reference

| Loan type | Min. down payment | Credit threshold | Geographic restriction |

|---|---|---|---|

| FHA | 3.5% (or 10% at 500–579 score) | 580+ for 3.5% down | None |

| VA | 0% | No fixed minimum; lender-set | None; service members, veterans, eligible spouses only |

| USDA | 0% | Lender-set, typically 640+ | Eligible rural/suburban tracts only; unavailable inside Chicago |

| Conventional | 3–5% | 620+ typical | None |

Source: HUD.gov loan programs. FHA and conventional financing both work anywhere inside city limits; USDA does not.

Leave a Reply