What Landlords Actually Require to Qualify You

Most NYC landlords set the same income bar: gross annual income of roughly 40 times the monthly rent, verified through pay stubs, an offer letter, or tax returns.

The 40x Rule Is a Custom, Not a Law

No New York statute sets an income multiple for lease approval. The 40x figure spread through the brokerage industry until it became the default underwriting shortcut, and it varies by building: smaller, owner-managed buildings sometimes accept 30x to 35x, especially with strong savings on file, while large luxury towers can ask for 50x. Landlords also pull a credit report, weighing payment history and existing debt more than any single cutoff.

Is the 40x rule a law? No. New York caps application fees and security deposits by statute, but no law sets an income multiple for approval. Each landlord sets its own threshold, and buildings vary from roughly 30x to 50x.

Broker Fees Since the FARE Act: Who Pays, and When

As of June 11, 2025, a broker who lists an apartment on a landlord’s behalf can’t collect a fee from the tenant renting it, even if the tenant found the listing on a major site like StreetEasy or Zillow.

| Who hired the broker | Who pays the fee | Typical amount |

|---|---|---|

| Landlord hired the broker (most listings) | Landlord | Negotiated between landlord and broker; no cost to tenant |

| Tenant hired their own broker to search | Tenant | A widely cited pre-FARE Act figure put this at 12% to 15% of annual rent; now a negotiable, tenant-initiated arrangement |

| Fee already paid or contractually owed before June 11, 2025 | Case-by-case | DCWP treats pre-effective-date obligations individually; no new fee is owed after the date regardless of lease date |

The core rule is that whoever hires the broker pays the broker. Violations are reportable to DCWP and, per legal analysis of the law, carry fines up to $2,000 plus a private right to sue for restitution.

Do I still have to pay a broker fee in 2026? Only if you hired the broker yourself. If a broker listed the apartment for the landlord, the FARE Act prohibits charging you for it, and you can report a violation to DCWP.

Documents to Bring, and What to Substitute If One Is Missing

| Document | Why it’s asked for | If you don’t have it |

|---|---|---|

| Photo ID | Confirms identity for lease and credit pull | A passport works if you lack a U.S. driver’s license |

| Pay stubs (last 2 to 3) or offer letter | Verifies income against the 40x threshold | A signed offer letter or employer letter is commonly accepted instead |

| Bank statements (2 to 3 months) | Shows reserves beyond salary | Asset statements can offset a marginal income multiple at some buildings |

| Tax returns (1 to 2 years) | Confirms income for freelance or self-employed applicants | 1099s plus a CPA letter often substitute |

| Credit/background check authorization | Required for the $20-capped check | Your own report from the past 30 days waives the fee |

A slow or incomplete application has a real cost in this market: 16.4% of Manhattan new leases in January 2026 closed as bidding wars, with the winning offer averaging 9.9% above the asking price.

Can I negotiate the broker fee or income requirement? Sometimes. Landlords who hired their own broker have no fee to negotiate with you, since they’re barred from charging you one; income shortfalls are more negotiable, especially with strong bank statements, a co-applicant, or a guarantor service.

Why Timing Changes Your Odds

Demand peaks between May and September, when most leases, including academic-year subleases near NYU and Columbia, turn over on the same 30 to 45 day cycle. Manhattan listing inventory fell 9.3% year over year in January 2026 even as new leases rose, which is part of why the December-through-February window typically brings faster approvals and smaller bidding-war premiums.

Market-Rate, Rent-Stabilized, or Co-op Sublease: Why the Lease Type Matters

Whether an apartment is market-rate, rent-stabilized, or a co-op sublease determines how much your rent can legally rise at renewal, and in 2026 that difference is worth more than usual.

Rent-Stabilized vs. Market-Rate vs. Co-op Sublease vs. Condo Lease

| Lease type | Renewal rights | Rent increase limit (current cycle) | Typical building |

|---|---|---|---|

| Rent-stabilized | Tenant has a right to renew | 0% for one- and two-year renewals commencing Oct 1, 2026 through Sept 30, 2027 | Pre-1974 buildings, generally 6+ units |

| Market-rate (unregulated) | No statutory renewal right | No cap; negotiated at each term end | Post-1974 construction, most new development |

| Co-op sublease (renting from a shareholder) | Set by the proprietary lease and board rules | Whatever the shareholder sets, subject to board sublet limits | Prewar and postwar co-op buildings |

| Condo lease | No renewal right beyond the lease term | No cap | Newer condo developments |

On June 25, 2026, the Rent Guidelines Board voted 7 to 1 to freeze rent-stabilized renewals at 0% for both one- and two-year leases, the first outright freeze in years, covering roughly one million apartments citywide. If your lease is stabilized and starts in that window, you owe nothing over last year’s legal rent. You can check a specific address’s stabilization status through the state’s DHCR rent registration records before you sign.

Applying: Approval Odds and What Happens If You’re Rejected

New York law caps the application fee at $20, and that fee must be waived entirely if you supply your own credit or background report from the past 30 days. Co-op and condo purchase applications are exempt from the cap, but renting or subletting a co-op unit from a shareholder is not; the $20 limit still applies there.

If another applicant is approved first, you generally don’t get the $20 fee back, and a guarantor-service premium is typically non-refundable once the provider has started underwriting.

What happens if my application is rejected? You usually forfeit the $20 application fee and any guarantor-service premium already processed; ask a provider about its refund policy before you pay, since terms differ by company.

Guarantor Options Beyond a Personal Cosigner

When income falls short of 40x and no personal cosigner qualifies, a paid guarantor service is the most common substitute, and pricing varies more than most renters expect.

| Option | Cost / requirement | Best for |

|---|---|---|

| Personal cosigner | Must earn roughly 80x the monthly rent, live in the tri-state area; no service fee | Renters with a qualifying relative or friend nearby |

| Insurent Lease Guaranty | 70% to 90% of one month’s rent for U.S. applicants with credit; 98% to 110% for non-U.S. applicants; requires income of 27.5x monthly rent or liquid assets of 50x | Renters at one of Insurent’s roughly 8,000 partner buildings |

| TheGuarantors | Reported 40% to 130% of one month’s rent by risk tier; the company doesn’t publish a fee schedule | Buildings that don’t accept Insurent |

| Negotiated larger deposit or prepaid rent | No fixed formula; deposit still capped at one month’s rent by state law | Renters whose landlord will deal directly instead of requiring a guarantor |

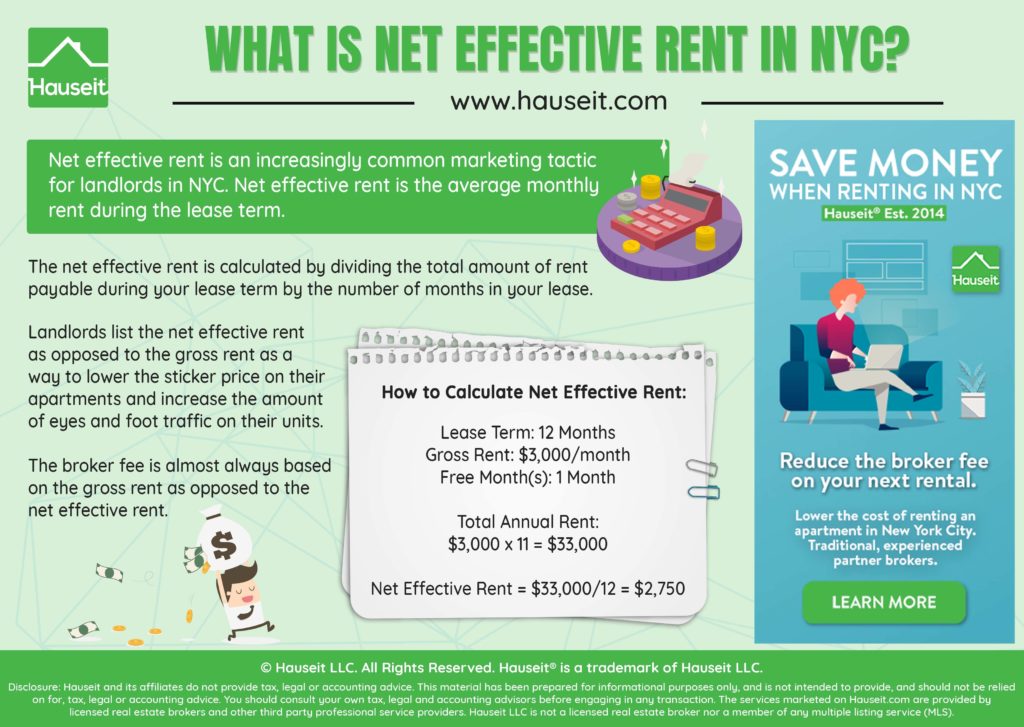

Signing Day: Net Effective Rent and the Real Move-In Cost

Net effective rent is what you pay per month once a landlord’s concession, usually a month of free rent, is averaged over the lease term, and it’s often meaningfully lower than the sticker price.

Net Effective Rent, With a Real Example

A $4,700 apartment offering one month free on a 12-month lease has a net effective rent of about $4,308: multiply the sticker rent by the 11 months you actually pay, then divide by all 12 months of occupancy. Comparing net effective rent, not the advertised number, is how you tell which of two similarly priced listings is cheaper.

Total cash at signing typically means first month’s rent, a security deposit capped at one month’s rent, and the $20 application fee, plus a broker fee only if you hired your own broker. A StreetEasy analysis published in September 2025 put average total move-in cash at $12,951 across NYC listings, a figure that blends fee and no-fee scenarios from the FARE Act’s early months.

Mistakes That Cost Renters the Apartment

- Submitting an incomplete document set. A missing pay stub or bank statement can put you behind a faster applicant in a bidding-war market.

- Underestimating total cash needed. Budgeting only for rent and deposit misses the $20 application fee and, for many renters, a guarantor premium running into four figures.

- Assuming “no-fee” still means the pre-2025 definition. Since the FARE Act, most listings default closer to no-fee-to-tenant unless you separately hire your own broker.

- Not confirming rent-stabilized status before signing. The 0% freeze applies only to stabilized units; a market-rate lease at the same address carries no such protection.

- Paying a guarantor premium before confirming the building accepts that provider. Insurent only works at its roughly 8,000 partner buildings, so a premium paid to the wrong provider is money spent with nothing to show for it.

Leave a Reply