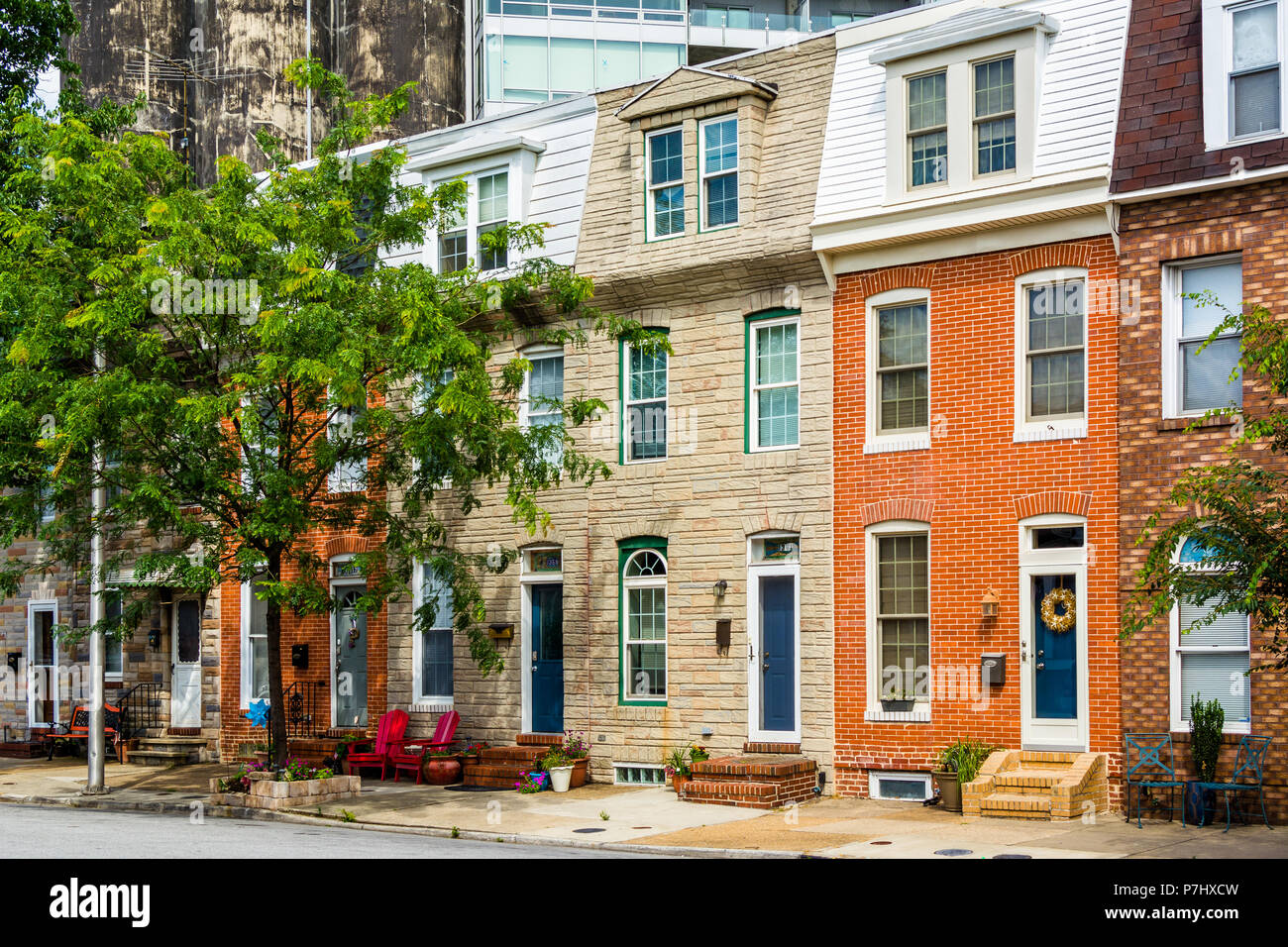

Housing Stock: Rowhomes, Silo Point, and New Construction

Rowhomes

Most of the housing stock is two- and three-story brick rowhomes built in the late 1800s and early 1900s, many eligible for the CHAP historic tax credit covered below. Renovated units typically run $350,000 to $600,000 depending on size, finish level, and parking.

Silo Point and Condo Towers

Silo Point is a 24-story, 228-unit condo tower converted from a Baltimore & Ohio Railroad grain elevator built in 1923–24. Developer Turner Development Group bought the 308-foot structure for $6.5 million in 2003 and opened residences in 2009, according to Baltimore Sun reporting and the Explore Baltimore Heritage archive. Units there currently list from the low $300,000s to over $1 million, and building-specific condo fees run well above a typical rowhome co-op’s fee – a gap the risk table below quantifies by factor, not by dollar figure.

New Construction

Townhome product such as ALTA47 sits at the upper end of the price range, generally $500,000 to $700,000 or more, and typically carries no CHAP eligibility, since the credit applies only to designated historic structures.

Does the historic designation limit what I can renovate? Yes: CHAP requires pre-approval of the renovation plan before work begins, and projects that start without it lose eligibility for the tax credit regardless of quality.

What Homes Cost Right Now

The price dispute above is not cosmetic. Redfin’s May 2026 figure reflects a thin, single-month sales pool – Redfin’s own recently-sold data counted 10 closings in a comparable recent month. Homes.com’s rolling 12-month median smooths that volatility but lags current conditions by design. A buyer comparing an active listing to either figure should ask the listing agent for the specific comparable sales used, not accept either number as settled.

Price per square foot: Redfin’s $243 (down 13.2% year over year) and Movoto’s $289 (June 2026 asking prices) bracket the likely range for a comparable sale. Days on market run from 19 (Movoto, asking data) to 44 (Homes.com, closed sales), both faster than Baltimore City’s overall 49-day average.

Who Locust Point Suits – and Who It Doesn’t

Locust Point suits buyers who want water-adjacent living within I-95 reach of downtown and can accept elementary-only school zoning, a working industrial edge, and a housing stock split between century-old rowhomes and a single dominant high-rise. It doesn’t suit anyone who needs guaranteed car-free walkability, or who won’t research flood exposure before making an offer on a three-sided peninsula.

Getting Around

| Destination | Distance | Notes |

|---|---|---|

| Johns Hopkins Hospital | 3 miles | Per Homes.com’s neighborhood data |

| Sinai Hospital | 5 miles | Per the same source |

| Inner Harbor / downtown | Under 2 miles | Via I-95 or the waterfront promenade |

| M&T Bank Stadium | Under 2 miles | Adjacent to the Hamburg Street light rail stop |

The neighborhood carries a Walk Score of 67, rated “moderately walkable,” with roughly 2,836 residents and 3,255 jobs counted in the same dataset.

Is Locust Point walkable without a car? A Walk Score of 67 means most errands require some walking, but a car materially expands options – a full 29 points below Fells Point’s 96, so the two neighborhoods aren’t comparable on walkability alone.

Schools: Zoned, Choice, and the Tension Nobody Mentions

Baltimore City elementary schools are assigned by home address; middle and high schools carry no zoning at all and instead run on a citywide choice lottery, with some programs requiring a minimum composite score for admission, per Live Baltimore’s guidance and Baltimore City Public Schools. A strong zoned elementary school guarantees nothing about middle or high school placement – a family moving to Locust Point purely for elementary zoning will still face the citywide choice process within a few years.

Are Locust Point schools zoned or open enrollment? Elementary is zoned by address; middle and high school placement runs through the citywide choice process.

What Nearby Neighborhoods Offer Instead

| Neighborhood | Median sale price (May 2026) | YoY change | Walk Score |

|---|---|---|---|

| Locust Point | $499,832 | −8.8% | 67 |

| Fells Point | $384,871 | +28.3% | 96 |

| Federal Hill-Montgomery | $269,809 | −27.6% | Not independently verified this pass |

| Canton | $449,900 (current asking, not median sold) | n/a | Not independently verified this pass |

Fells Point’s walkability lead is large enough that it, rather than price, likely decides the choice for a buyer weighing the two; Federal Hill-Montgomery’s much lower reported median may reflect a smaller, more volatile sales sample rather than a genuinely cheaper market.

Buying Here: CHAP Credits, Flood Exposure, and Industrial-Adjacency Costs

The CHAP Tax Credit

Baltimore’s CHAP program grants a 10-year property tax credit on the increase in assessed value that follows a qualifying rehabilitation, provided the owner reinvests at least 25% of the property’s pre-rehab full cash value and receives pre-approval before work begins. The credit is computed once, fixed for the decade, and transfers to the next owner. Citywide, more than 3,500 properties have used it since 1997, at a cost to the city of roughly $10 million a year in foregone revenue, according to a PlaceEconomics analysis commissioned by the city. A recently listed Locust Point rowhome carried an active credit with about eight years remaining and roughly $68,000 in projected remaining savings – real money a buyer should confirm transfers with the sale.

Flood Zone and Insurance

Locust Point sits on a peninsula bordered by water on three sides. Redfin’s First Street-sourced data rates the neighborhood’s flood risk as moderate, with about 1% of properties (14 homes in the dataset) projected to face severe flooding risk over the next 30 years, and notes that risk is rising faster than the national average. That figure is a portfolio-level estimate, not a parcel-specific flood-zone letter; buyers should pull the FEMA designation for the exact address before waiving a flood-insurance contingency, since elevation varies block by block on a peninsula this size.

Noise, Smell, and Cruise-Day Traffic

The Domino Sugar refinery, a 30-acre working plant at 1100 Key Highway that processes about 98 million pounds of sugar a year according to Baltimore Magazine, sits at the neighborhood’s edge. Its landmark sign switched from neon to LED lighting in a roughly $2 million project completed in July 2021, according to SouthBMore.com – a small, checkable sign the plant is an active, maintained operation. Buyers on blocks closest to the working waterfront should expect occasional plant noise and, on cruise-terminal sailing days, added congestion on Fort Avenue.

| Factor | Why it matters | Who’s most affected |

|---|---|---|

| CHAP eligibility | Can be worth tens of thousands over 10 years | Buyers of pre-1900s rowhomes in designated districts |

| Flood risk | Affects insurance cost and resale liquidity | Owners on low-lying, water-facing blocks |

| HOA/condo fee spread | Rowhome co-op fees differ sharply from Silo Point’s full-service fee | Condo buyers comparing product types |

| Industrial adjacency | Noise, odor, and cruise-day congestion | Blocks nearest Fort Avenue and the working waterfront |

Is flood insurance required for homes here? It depends on the specific parcel’s FEMA flood-zone designation, not the neighborhood as a whole; a lender will require insurance only if the individual address falls within a mapped high-risk zone.

For Investors: Rental Demand and Yield Context

Reported one-bedroom rents range roughly $1,625 to $2,700 across trackers, with averages clustering between $1,908 and $2,214, per Apartments.com and Apartment List. Two-bedroom rents range roughly $2,385 to $2,957 on average, with a wider top end near $6,900 for high-end waterfront units. Against a $350,000 to $475,000 typical rowhome purchase price, that implies a gross rent-to-price ratio of roughly 0.4% to 0.6% monthly – worth checking against a specific property’s actual carrying costs, including the city’s $2.248-per-$100 property tax rate (about $2.04 for owner-occupied homes with the homestead credit, per Baltimore City Finance), any CHAP credit, and condo or HOA fees, rather than treated as a blanket yield figure.

Is Locust Point a good rental investment right now? The math depends heavily on whether the specific unit carries a CHAP credit and what its actual HOA or condo fee is; a rowhome without those carrying costs pencils out very differently from a Silo Point unit with a premium condo fee, even at a similar purchase price.

Leave a Reply