How renting directly from an owner works here

FRBO means the owner handles what a property-management company normally would: maintenance requests, showings, lease terms, deposit handling. In New Orleans that has two practical consequences a managed rental doesn’t. Louisiana law does not require the deposit to sit in an escrow or interest-bearing account, so there’s no third-party record of where your money went. And the lease is often not a standardized management-company form, so clauses vary house to house, which is exactly why the checklist further down matters more here than it would with a large landlord.

Verifying a listing and the owner are real

Renters filed nearly 65,000 rental-scam reports with the FTC between January 2020 and June 2025, totaling $65 million in losses, with a median reported loss of $1,000, according to the FTC’s December 2025 data spotlight. FRBO listings are a natural target: there’s no company reputation on the line, and a private “owner” is easy to fabricate.

Cross-check ownership directly: type the address into the Orleans Parish Assessor’s property search or the City’s Property Viewer and compare the name on record to the name you’re corresponding with. A mismatch isn’t automatically a scam; the owner could be an LLC or a family trust. It’s a reason to ask direct questions before you commit money.

Licensed rental, or unlicensed short-term rental wearing a FRBO listing?

New Orleans defines a short-term rental as any dwelling rented for fewer than 30 consecutive days (60 in the Vieux Carré), and operating one without a permit is illegal under both the Municipal Code and the Comprehensive Zoning Ordinance, per the City’s Short Term Rental Administration. A Non-Commercial Short Term Rental permit requires the owner to actually live in the home full-time and reserve one bedroom for their own occupancy, a different arrangement than a straightforward month-long-plus FRBO lease. If a listing’s terms feel closer to a nightly or weekly booking than a lease, ask directly whether it operates under an STR permit and whether the term you’re being offered is 30 days or longer. Unpermitted STR activity can be referred to an administrative adjudication hearing, and the City can revoke the owner’s permit or impose fines, none of which protects you if you’ve already moved in expecting a standard tenancy.

What happens if the “FRBO” listing turns out to be an unlicensed short-term rental?You have no standing as a long-term tenant if the unit was never legally a long-term rental to begin with, and the City’s enforcement action targets the owner’s permit, not your lease. Ask for the STR permit number or proof the listing is for a 30-day-plus term before you pay anything.

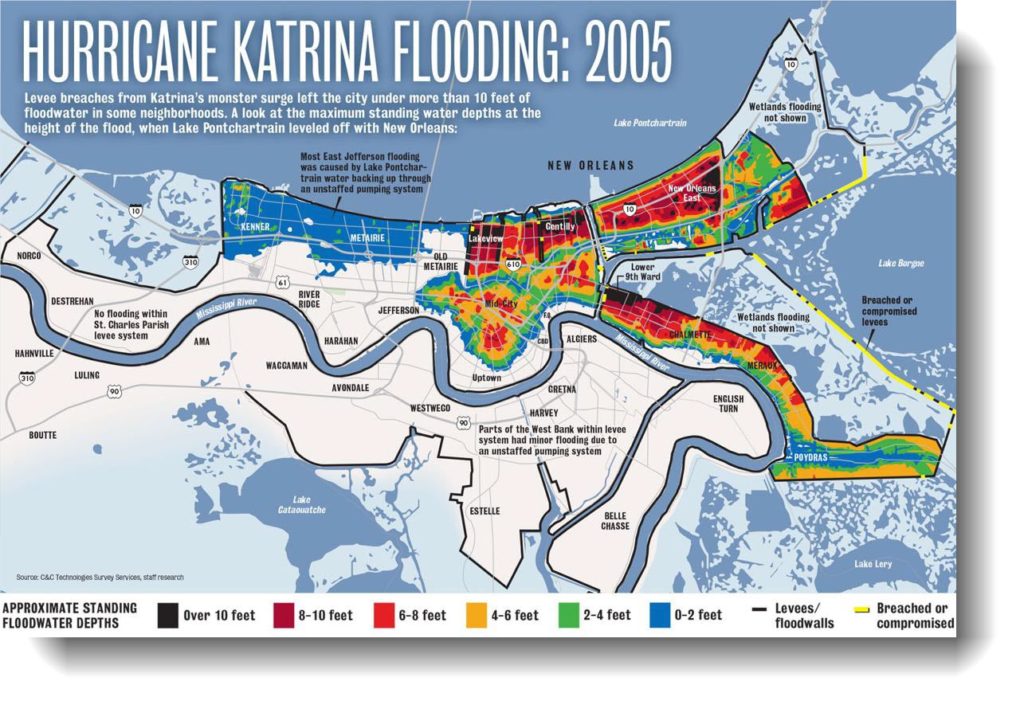

Flood zone, elevation, and insurance by neighborhood

This is the single biggest driver of what a house actually costs to live in, and it’s the one factor no marketplace listing surfaces next to the price. New Orleans’ historic ridge neighborhoods sit on naturally higher ground; the low-lying “bowl” neighborhoods, drained and developed toward the lake, carry materially higher flood-zone designations and insurance costs, per The W Group Real Estate’s 2026 buyer breakdown and the city’s own hazard-mitigation planning, cited by Ashley Nesser.

| Neighborhood cluster | Typical FEMA zone | What it means for you |

|---|---|---|

| Uptown, Marigny, parts of Gentilly (ridge) | X, unshaded | Lower risk; a separate flood policy still costs roughly $500 to $800 a year even though it isn’t federally required |

| Lakeview, West End | AE, with V-zone pockets near the lake | Federally required flood insurance on financed properties; Lakeview is named among the city’s lowest-elevation areas in its own hazard planning |

| Gentilly, Mid-City | AE, built on former swampland | Heavy-rain and canal-overflow flooding on top of the standard flood-zone risk |

| Bywater, Marigny, Lower Ninth Ward | AE, levee-adjacent | Bordered by the Industrial Canal and the Mississippi River levee system; surge and drainage risk distinct from lake-side neighborhoods |

| New Orleans East | AE, low-lying | Large tracts remapped into AE zones; among the more exposed areas in the parish |

An address on the ridge and an address in the bowl can carry insurance costs $1,000 or more apart even at an identical rent. A house without an elevation certificate on file can cost $1,000 to $3,000 a year more to insure than a comparable house that has one, since the certificate documents how far the first floor sits above the flood-plain baseline. Look up any specific address on the FEMA Flood Map Service Center or the City’s Base Flood Elevation lookup tool before you sign, because a neighborhood-level generalization can be wrong for one particular block.

Do I still need renters insurance if the owner has homeowners insurance?Yes. A homeowner’s policy covers the structure, not your belongings or your liability inside it, and it doesn’t cover flood damage to your possessions at all: that requires a separate NFIP or private flood policy in your own name.

What a privately drafted Louisiana lease must cover

A private owner’s lease was probably not written by the same legal-review process a management company’s template goes through, so the following aren’t suggestions. They’re statutory minimums.

| Lease clause | What Louisiana law sets | What to verify yourself |

|---|---|---|

| Security deposit return | Returned within one month of lease termination, with an itemized statement if any amount is withheld (La. R.S. 9:3251) | The lease’s stated timeline matches or beats one month |

| Notice to end month-to-month | 10 calendar days before the end of the rental month, from either side (Civil Code art. 2728) | Whether the lease requires longer notice than the statutory minimum |

| Bad-faith withholding penalty | Greater of $300 or double the amount wrongfully withheld, plus possible attorney’s fees (La. R.S. 9:3252) | Keep a written, dated demand for your deposit; verbal requests weaken your claim |

| Habitability | Landlord has a Civil Code duty to deliver and maintain the property in a condition fit for its intended use | Get repair promises in writing, since a private owner has no maintenance-ticket paper trail |

| Lead-based paint | Federal disclosure required for any unit built before 1978 | Ask directly if the house predates 1978 and request the disclosure form if so |

Security deposit timing is about to change

Louisiana’s Lessee’s Deposit Act, R.S. 9:3251, currently sets a one-month return window. 2026 Act 63 (HB292) amends that statute, with an effective date of August 1, 2026. If you’re signing a lease that will still be active on that date, ask the owner directly whether their lease language has been updated to match the amended statute, since older lease templates may still reference the pre-amendment wording.

Notice periods run both directions

If your lease has no fixed term, a true month-to-month arrangement, either you or the owner can end it with 10 calendar days’ written notice before the end of the rental month, under Civil Code article 2728. Oral notice doesn’t count; keep a dated, written copy.

Habitability has no PM company to escalate to

In a managed rental, a maintenance ticket goes to a company with a process. Here, a habitability problem, no working plumbing, no functioning smoke detectors, structural water intrusion, is a direct conversation with the person who also holds your deposit. Document every repair request in writing from day one.

How long does a private landlord in Louisiana have to return my deposit?One month after the lease terminates, under current law. Verify whether your specific lease’s language has been updated for the amended timeline taking effect August 1, 2026, if your lease extends past that date.

Utility setup and historic-home logistics

There’s no property-management company to set up utilities for you: you’ll open your own Entergy New Orleans electricity account and your own Sewerage & Water Board account the same week you get keys, and both typically require a deposit if you have no prior account history in the city. Many New Orleans houses are 80 to 100+ years old, with raised foundations, older wiring, and window units rather than central air, none of which a private owner is obligated to disclose upfront the way a rental-listing photo makes a house look.

Negotiating directly with an owner

Pull three comparable listings in the same neighborhood and flood-zone tier, not just the same bedroom count, before you make an offer; that match matters because insurance and utility costs, not just rent, are what a private owner is actually weighing against another applicant. An owner who self-manages often values a longer lease term or a demonstrably reliable applicant (verifiable income, references from a prior landlord) more than a marginal discount, since re-listing costs them time they don’t have a leasing office to absorb.

Is there a discount for renting FRBO instead of through a management company?Not inherently. What changes is who you’re negotiating with: a private owner can say yes to a nonstandard request, a longer lease, a payment date shift, on the spot, where a management company needs a policy exception.

Leave a Reply