What You’re Actually Buying: Mobile, Manufactured, and Modular

Three labels appear almost interchangeably in listings, and they carry different legal and financing consequences. A mobile home is a factory-built unit constructed before June 15, 1976, when the current federal construction and safety code took effect; almost none remain in active sale inventory. Manufactured homes are built after that date under HUD’s Manufactured Home Construction and Safety Standards, arrive on a permanent steel chassis, and carry a red HUD certification label on each section. Modular homes are also factory-built, but to state and local building codes rather than the federal HUD code, and they become real property automatically once installed on a foundation – they never pass through the personal-property stage the other two can.

| Type | Built | Governing code | Typical financing eligibility |

|---|---|---|---|

| Mobile home | Before June 15, 1976 | Pre-HUD, no federal standard | Rarely financeable; most lenders exclude pre-1976 units entirely |

| Manufactured home | After June 15, 1976 | HUD Manufactured Home Construction and Safety Standards | Chattel loan (personal property) or mortgage/FHA Title II (real property), depending on titling |

| Modular home | Any date | State and local building code | Financed like a site-built home once installed; always real property |

Manufactured homes are the only category where the same physical structure can be financed two structurally different ways: the deciding factor is what happens to the title, not what the home looks like.

What’s the difference between a mobile home and a trailer? In modern use, none in practice: pre-1976 factory-built homes are informally called both. A travel trailer is a distinct category built for temporary recreational towing, not year-round residence, and it isn’t covered by the HUD code at all.

What It Costs

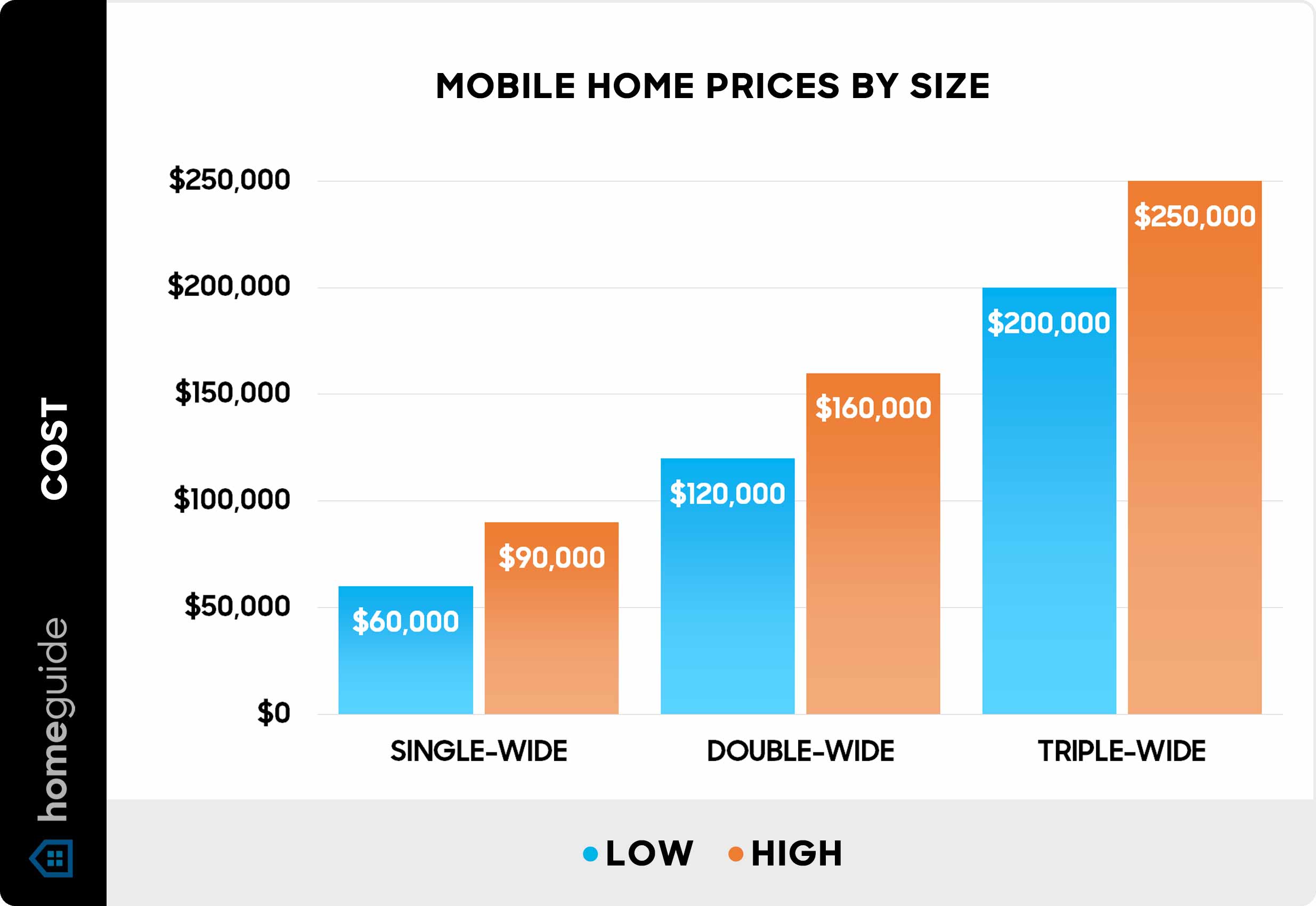

The Manufactured Housing Institute puts the 2025 national average for a new home at $115,557, with single-section homes averaging $95,074 and multi-section homes at $156,170; existing homes averaged $73,326, up 2.31% from the prior year. A separate federal series tells a related but not identical story: the Census Bureau’s Manufactured Housing Survey, via the Federal Reserve’s data system, put the average sales price of a new single-section home at $88,200 in December 2025 – lower than MHI’s annual single-section average because it measures one month’s shipments rather than a full-year blend across regions. Neither number is wrong; they measure slightly different things, and a page that quotes only one without saying so is quietly picking whichever figure flatters its narrative.

| Home type | New (avg.) | Existing/resale (avg.) | Source and date |

|---|---|---|---|

| Single-section | $95,074 | $73,326 (blended, all types) | MHI 2025 State of the Industry |

| Multi-section | $156,170 | ||

| All types, new | $115,557 | – | |

| All types, existing | – | $73,326 |

The sticker price is the smallest line item once land, delivery, and setup enter the budget. Foundation work alone spans roughly $1,000 for a basic pier-and-block system to $40,000 for a full poured basement, and insurance is a separate, ongoing cost that most buying guides under-specify. National averages run $700 to $1,500 a year, per Insure.com’s 2026 cost data, but the gap between a manufactured home and an otherwise comparable site-built house can be stark. Consumer Reports profiled a Spearfish, South Dakota family paying about $1,800 a year to insure a 2,400-square-foot 1913 farmhouse, while their daughter and son-in-law paid almost $4,000 for similar coverage on a 1,500-square-foot manufactured home a hundred feet away. Consumer advocates cited in that reporting attribute part of the gap to genuine wind-and-fire risk and part to underwriting bias against manufactured housing specifically.

Is home insurance required for a mobile home? Not by federal law. Lenders financing the home and most land-lease communities require it as a condition of the loan or the lease, so in practice it’s rarely optional. Expect $700 to $1,500 a year nationally, more in coastal or high-wind states.

Financing: Why It’s Different, and What’s Actually on Offer

Land ownership decides which of five paths is even available. A chattel loan finances the home as personal property and doesn’t require owning the land – government mortgage-disclosure data show it’s how 42% of all manufactured-home purchases are financed, per the CFPB’s 2021 HMDA analysis – but chattel loans have historically carried an annual percentage rate roughly 150 basis points above the average prime offer rate for comparable mortgages, according to the CFPB’s earlier 2014 report on the same market. Lender guides published in late 2025 put typical chattel rates in the 7% to 10% range against 6.5% to 7.5% for a conventional or FHA-backed manufactured-home mortgage.

| Loan type | Property classification required | Down payment / eligibility notes | Rate note | Source |

|---|---|---|---|---|

| Chattel loan | Personal property (home only) | Land ownership not required; 10%–20% down typical | ~150 bps above comparable mortgage APOR historically; lender estimates put current rates at 7%–10% | CFPB 2014 report; lender rate guides |

| FHA Title I | Personal or real property | No land ownership required; loan limits $105,532–$237,096 depending on section count and combo status | Government-insured, not government-issued; rate set by originating lender | HUD.gov 2024 Title I Letter |

| FHA Title II | Real property only | Requires owned land, permanent foundation | Loan ceiling $541,288–$1,249,125 for 2026, varies by county | FHFA 2026 conforming limit addendum |

| Conventional / VA | Real property only | Requires owned land, permanent foundation, title converted from personal to real property | Priced like a standard mortgage for the borrower’s credit profile | Freddie Mac CHOICEHome program |

The practical dividing line isn’t the loan’s name. It’s whether the home is still titled as personal property when the application goes in. Convert the title first, and three additional loan types open up; skip that step, and chattel is the only door available regardless of credit score.

Can I get a traditional mortgage for a mobile home? Only if it’s titled as real property: built after June 15, 1976, on a permanent foundation, on land you own, with the personal-property title surrendered. Otherwise the available options are a chattel loan or an FHA Title I loan, both of which finance the home without requiring land ownership.

Titling and Property Tax

Manufactured homes start out titled like a vehicle, through a state DMV or equivalent agency, and stay that way, taxed as personal property rather than real estate, until the owner files to convert them. Conversion generally requires owning the land, a permanent foundation, and surrendering the vehicle title; Mississippi’s Department of Revenue, for instance, requires wheels and axles removed and the unit anchored under state insurance-department rules before a county tax assessor will record the change to real-property status.

Buying New vs. Used: What to Verify

A used manufactured home carries paperwork risks a new one doesn’t. If the HUD certification tag or data plate is missing or damaged, a lender’s appraiser will typically require a verification letter from the Institute for Building Technology Safety confirming the home passed its original HUD inspection – ordering that letter costs money and can take up to two weeks, a delay worth planning around before signing a contract. Some states also require a separate vehicle title tied to the home; if it’s still in the seller’s name at closing, that has to be resolved before the deal can move to a real-property conversion.

| What to check | How | Why it matters |

|---|---|---|

| HUD certification tag / data plate | Confirm the red metal tag on each section and the data plate inside a cabinet or utility closet | Missing tags trigger a costly, multi-week IBTS verification before most lenders will approve financing |

| Vehicle title status | Ask for the current title and confirm the seller’s name matches | An unresolved vehicle title blocks the real-property conversion needed for mortgage financing |

| Foundation type | Ask whether it’s pier-and-block (temporary) or a permanent foundation meeting the lender’s standard | Only a permanent foundation supports real-property titling and conventional financing |

| Structural and utility condition | Independent inspection of framing, roofline, plumbing, and electrical | Water damage and sagging floors are the most common source of post-purchase repair costs on resale units |

Skip any one of these four checks and the home can turn out to be unfinanceable through anything but a second chattel loan, regardless of how it looked in the listing photos.

What happens if the HUD tag is missing on a used home? The lender or appraiser will typically require a letter from the Institute for Building Technology Safety verifying the home passed its original HUD inspection. Ordering it has a cost and can take up to two weeks, so factor that delay into any purchase timeline.

Where to Put It: Land-Lease Communities vs. Owned Land

Choosing a rented lot over owned land trades a lower upfront cost for a landlord relationship that state law treats unevenly. A Freddie Mac Multifamily survey of state manufactured-housing statutes against a standard set of tenant protections found substantial state-to-state variation, with some protections addressed explicitly and others left silent or handled only through general landlord-tenant law that may or may not apply when the tenant owns the home but not the land. Two concrete examples show the range: Washington law caps annual lot-rent increases at 5% and requires three months’ written notice before any increase takes effect, while Texas governs manufactured-home communities under a dedicated chapter of its Property Code that mirrors, but doesn’t duplicate, its apartment-lease rules. Monthly site fees themselves run roughly $100 to $800 depending on region and amenities, rising an estimated 3% to 5% a year, per one industry-adjacent buyer’s guide – a wide enough range, thinly enough sourced, that it belongs in a budget as a figure to verify locally rather than a number to plan around.

- Owned land: higher upfront cost, but the path to real-property titling and conventional financing is open from day one.

- Land-lease community: lower upfront cost and no need to own land to get a chattel loan, but rent increases and eviction protections depend entirely on which state you’re in.

- Land co-op / resident-owned community: residents collectively own the land through a cooperative structure, converting some of the lease-vs-own tradeoff into a hybrid, worth investigating specifically in states with weaker statutory tenant protections.

Selling a Manufactured Home Later

Resale friction tracks titling exactly the way purchase financing does. A home still classified as personal property can only be resold to a buyer who qualifies for a chattel loan or pays cash, a much smaller pool than a mortgage-qualified buyer pool for a house on owned land.

Is It Worth It: Appreciation, Depreciation, and Resale

Do mobile homes lose value over time? It depends almost entirely on land ownership: homes on owned land can appreciate, with more volatility than site-built housing, while homes on rented lots typically don’t build resale value the same way, per CFPB research on land ownership and appreciation.

Leave a Reply