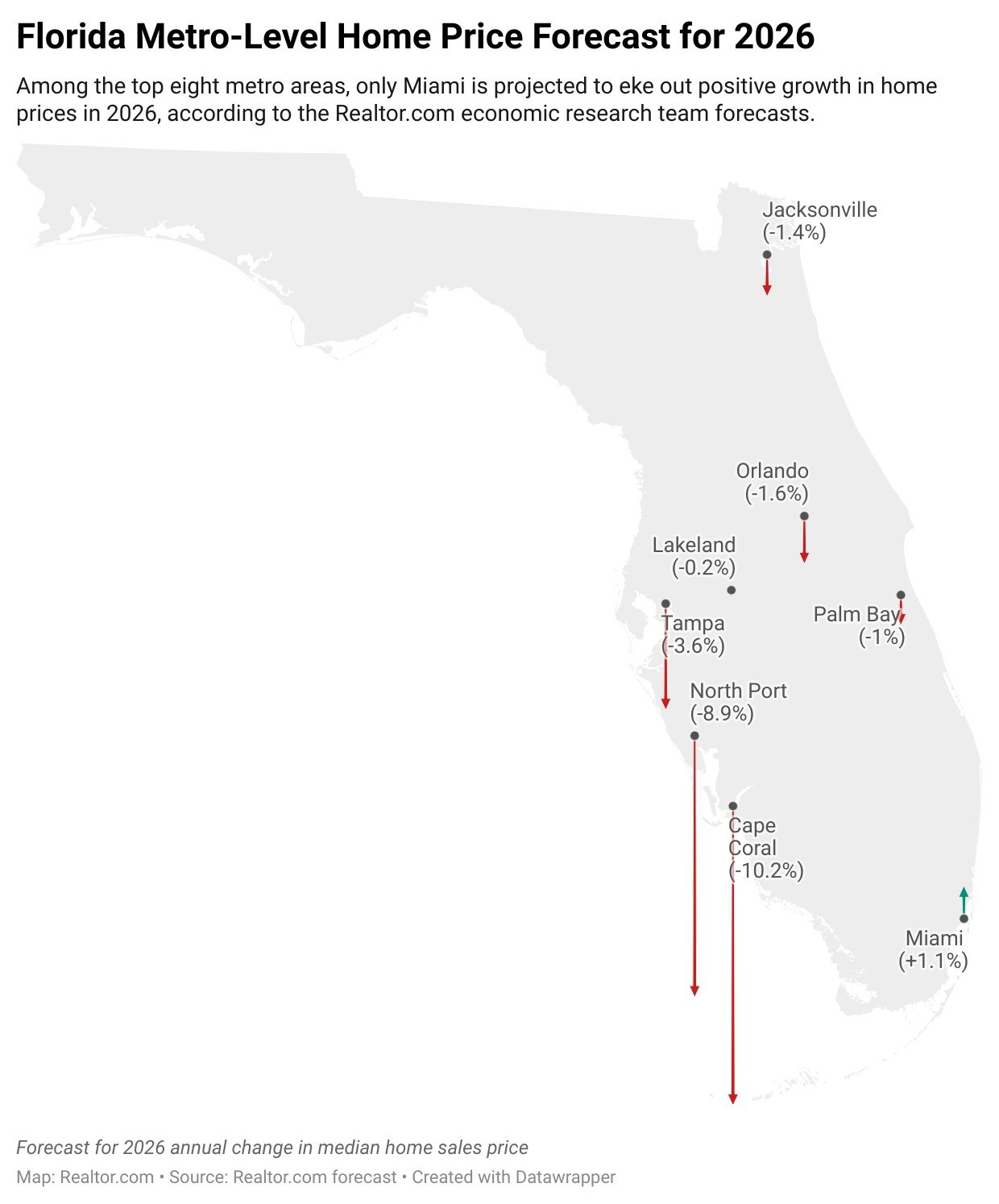

Regional price and pace across Florida

A median-priced house in one Florida metro can cost more than four times its equivalent in another, and price doesn’t track with speed. The table below compares five metros on the same two measures using the same source and month.

| Metro | Median sale price | Days on market | Why it differs |

|---|---|---|---|

| Jacksonville | $300,000 | 67 | Inland market, lowest entry price of the five, steady relocation demand |

| Orlando | $410,000 | 48 | Inland, tourism and relocation driven, faster pace than the coastal south |

| Tampa | $443,000 | 41 | Coastal with a broad inland buffer, the fastest-moving of the five |

| Miami | $652,000 | 113 | International capital and second-home demand push price up while pace slows |

| Naples | $1,300,000 | 83 | Second-home and retirement wealth concentrated in a small, largely built-out coastal market |

All figures: Redfin metro housing-market pages, May 2026 three-month trailing medians; Jacksonville reflects the three months ending April 2026. Miami costs more than 50% above Orlando’s median yet takes over twice as long to sell, a sign of a smaller, more discretionary buyer pool rather than simple scarcity.

Property taxes: what changes after year one

Florida’s homestead exemption removes up to $50,000 from a primary residence’s taxable value. The larger effect is the Save Our Homes (SOH) cap it activates: once granted, a homesteaded property’s assessed value can rise by at most 3% or the change in the Consumer Price Index, whichever is lower. For 2026 that CPI figure is 2.7%, per the Florida Department of Revenue, cited by Pinellas County.

Homestead cap and portability

The cap starts the year after homestead is granted and resets to full market value the year after a home is sold, so a buyer purchasing from a longtime owner should expect the assessed value, and the tax bill, to jump in year two regardless of what the seller paid. Owners moving between Florida homesteads can carry up to $500,000 of accumulated SOH benefit to a new property, a benefit known as portability, but must establish the new homestead within three tax years of leaving the old one, per Florida Statute §193.155(8).

The non-homestead 10% cap

Second homes, rentals, and any non-owner-occupied property get a separate 10% annual assessment cap under Fla. Stat. §193.1554/193.1555, roughly three times looser than the homestead cap. Switching a property’s status resets it to full market value the following January 1 before the new cap applies, a pitfall confirmed in Orange County Prop. Appraiser v. Sommers and detailed by Jones Foster.

Do property taxes go up after I buy a house in Florida? Usually, yes, in year two. The seller’s capped assessed value resets to full market value the January after closing, so the buyer’s first full tax year is typically based on the purchase price, not the prior owner’s bill.

Insurance: the real ongoing cost

Citizens Property Insurance Corporation, the state’s insurer of last resort, held 395,144 policies in the first week of January 2026, down from 936,182 a year earlier and from a peak of 1.42 million in October 2023, according to Florida Realtors, citing Citizens’ own reporting. That decline reflects a state-run depopulation push moving policies to private carriers, not a change in underlying storm risk.

Coastal vs inland variance

Coastal counties consistently carry higher wind and named-storm premiums than inland ones, a direct consequence of hurricane exposure. A buyer comparing a Naples or Miami-area property against an Orlando or Jacksonville one should request an insurance quote before writing an offer, since the gap can run into thousands of dollars a year on comparably priced homes.

Citizens as insurer of last resort

Under Citizens’ binding suspension rule, agents cannot bind new coverage, or add coverage to an existing policy, once the National Weather Service issues a tropical storm or hurricane watch or warning for any part of Florida, and that restriction typically holds until the storm has passed. Flood coverage carries its own separate 30-day waiting period on new policies under the National Flood Insurance Program, waived only at loan closing or within a defined window after a flood-map update. Flood and wind coverage are two different policies with two different triggers, and conflating them is one of the most common first-time-buyer mistakes.

Why is home insurance so much more expensive near the coast than inland in Florida? Wind and storm-surge exposure drive the premium, not property value alone; a $400,000 inland home and a $400,000 coastal home can carry premiums thousands of dollars apart because the insurer prices hurricane risk.

Condos and HOAs: the special-assessment risk

Following the Champlain Towers South collapse in Surfside on June 24, 2021, which killed 98 people, the legislature passed Senate Bill 4-D, now codified at Fla. Stat. §553.899. The law requires a milestone structural inspection for any condominium or cooperative building three or more habitable stories tall, once it reaches 30 years of age from its certificate-of-occupancy date, or 25 years if the building sits within three miles of the coastline, and every 10 years after that. A companion Structural Integrity Reserve Study (SIRS) is required on the same building population every 10 years and sets how much the association must hold in reserve for major components: roof, load-bearing walls, floor, foundation, plumbing, and more.

Milestone inspections and reserve studies

Phase 1 is a visual inspection; if it finds no substantial structural deterioration, the process ends until the next 10-year cycle. If it does, Phase 2 requires destructive testing and a repair plan, which is where special assessments running into the tens of thousands of dollars per unit typically originate.

| Building profile | Inspection requirement | Typical special-assessment risk |

|---|---|---|

| Under 3 habitable stories, any age | Exempt from SB 4-D | Low; driven only by ordinary reserve underfunding |

| 3+ stories, under 25 to 30 years old (coastal distance dependent) | No milestone inspection due yet; SIRS still required at the 10-year mark | Low to moderate, depending on reserve funding shown in the SIRS |

| 3+ stories, at or past the 25-year (coastal) or 30-year (inland) threshold | Milestone inspection mandatory; Phase 2 possible | Moderate to high if Phase 1 finds deterioration |

Before writing an offer on a condo, request the building’s most recent SIRS and milestone inspection report along with the reserve-funding percentage; a building that hasn’t yet crossed its threshold carries materially less near-term risk than one already in Phase 2.

New construction and CDD fees

A Community Development District (CDD) is a special-purpose local government entity, authorized under Florida Statute Chapter 190, that issues bonds to finance a new community’s roads, utilities, drainage, and amenities, then repays those bonds through an annual assessment on the tax bill. Statewide, CDD assessments typically run $1,000 to $3,500 a year, according to a Tampa Bay-area buyer guide, split between a fixed debt-service portion (running 20 to 30 years) and an operations-and-maintenance portion that continues indefinitely, even after the bonds are paid off.

| Cost type | Typical range or mechanism | When it applies |

|---|---|---|

| Property tax (homestead) | Assessed value capped at 3% or CPI (2.7% for 2026) after year one | All owner-occupied primary residences |

| Property tax (non-homestead) | Assessed value capped at 10% annually | Second homes, rentals, investment property |

| Homeowners/wind insurance | Varies sharply by coastal proximity, building age, roof condition | All owners; required by any mortgage lender |

| Flood insurance (NFIP) | 30-day waiting period on new policies unless tied to loan closing | Required in flood zones with federally backed loans |

| CDD assessment | $1,000 to $3,500/year, on the tax bill | New construction in most master-planned communities |

| Condo special assessment | Case by case, often five to six figures per unit | Triggered by a failed Phase 1 milestone inspection |

The tax and CDD lines are the two most predictable costs and the two most commonly missing from a builder’s or agent’s upfront estimate; both show up on the annual tax bill rather than as a separate invoice, which is exactly why buyers overlook them.

What is a CDD fee, and can I get out of paying it? It’s a non-ad-valorem assessment on the tax bill that repays the bonds used to build a community’s infrastructure. Some districts allow individual lot owners to prepay the remaining bond balance in a lump sum, but the operations-and-maintenance portion continues regardless.

Buying from outside the US

None of the analyzed listing portals or overseas-marketplace pages address financing, resale tax, or title structure for a non-US buyer in any depth specific to Florida.

Financing without US credit history

Buyers without a US Social Security number or credit history generally need a foreign-national mortgage program or an all-cash purchase; conventional US mortgage underwriting relies on a domestic credit file that a new arrival typically doesn’t have yet.

FIRPTA on resale

When a foreign person eventually sells US real property, the buyer must generally withhold 15% of the amount realized and remit it to the IRS, per the Foreign Investment in Real Property Tax Act. That rate drops to 10% for an owner-occupied purchase priced between $300,001 and $1,000,000, and the withholding requirement doesn’t apply at all if the sale price is $300,000 or less and the buyer’s family will occupy the property for at least half of the following two years. The withholding is an advance deposit against the seller’s actual tax liability, and any excess can be recovered by filing a US return.

Holding title

Foreign buyers commonly hold Florida property directly as individuals or through a US-based LLC or trust for liability and estate-planning reasons; the right structure depends on the buyer’s home-country tax treaty position and should be set before closing, not after.

Can I buy a house in Florida if I’m not a US citizen or resident? Yes. There’s no citizenship or residency requirement to buy US real estate; financing and the eventual FIRPTA withholding on resale are the two mechanics that differ from a domestic purchase.

Timing: when this market moves

Florida’s hurricane season runs June through November, and an active tropical storm or hurricane watch or warning anywhere in the state can freeze new insurance binding mid-transaction, the mechanic explained above, stalling a closing with no guaranteed timeline. The National Flood Insurance Program’s authorization is currently set to expire September 30, 2026 absent Congressional reauthorization, which would pause new and renewal flood policies statewide until resolved.

Common mistakes and their costs

- Budgeting only the listed price. Skipping CDD, non-homestead tax exposure, and coastal insurance premiums in the initial affordability math is the single most common gap.

- Assuming the current tax bill will carry over. Confirm the post-sale estimate with the county property appraiser’s office, not the seller’s current bill, since the Save Our Homes cap resets at sale.

- Treating HOA dues as the only recurring condo cost. A building approaching its SB 4-D milestone threshold can add a special assessment on top of monthly dues.

- Shopping for insurance after the offer is accepted. Coastal premiums can change the real monthly payment enough to affect the loan amount a buyer qualifies for.

- Closing during an active storm threat without a bound policy. Binding suspensions can delay a closing by days or weeks with no guaranteed timeline.

Is spring or hurricane season a worse time to buy a house in Florida? Hurricane season, June through November, carries the real risk: an active storm threat can freeze new insurance binding and stall a closing, a risk that doesn’t exist during the spring shopping season.

Leave a Reply