Why Altadena’s Market Is Really Three Markets Right Now

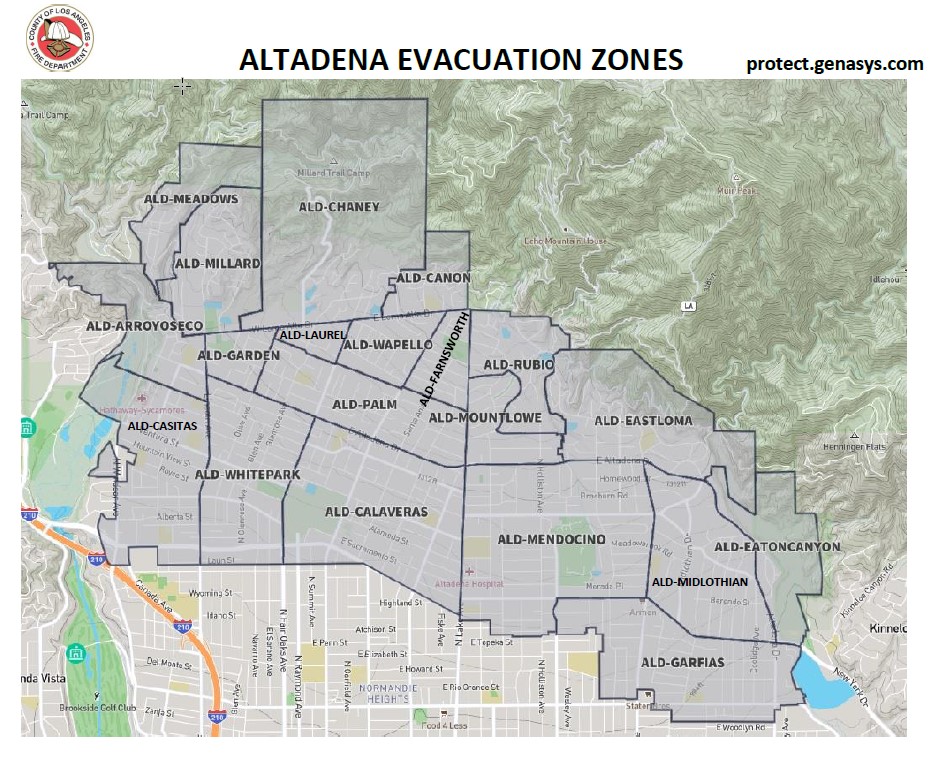

The Eaton Fire’s evacuation orders covered named zones across Altadena, Pasadena, Sierra Madre, and unincorporated foothill areas, from parcels neighboring JPL to Kinneloa Canyon, and left three distinct kinds of property in its wake: parcels where the structure is gone, parcels that survived but sit inside or against the burned area, and parcels the fire never touched. Buyers, sellers, and investors are all shopping the same zip code but effectively three different products.

If your goal is a primary residence and a shorter timeline: Zone C. If your goal is a discount with real upside and you can shop insurance patiently: Zone B. If your goal is land and you’re prepared for a multi-year build: Zone A.

| Zone | Typical condition | Financing implications | Price behavior vs. intact comps | Typical buyer |

|---|---|---|---|---|

| Destroyed | Cleared or clearing lot; structure gone | Cash or construction-to-permanent loan; a standard 30-year mortgage rarely applies to raw land | Priced near land value, well under pre-fire comps | Owner-rebuilders, developers, cash buyers |

| Fire-adjacent, standing | Home survived; inside or bordering the burned area and a high-hazard zone | FAIR Plan plus a DIC wrap usually replaces admitted coverage; lenders require proof before closing | Discounted against untouched blocks; the discount narrows as insurance options widen | Patient owner-occupants, value-focused investors |

| Untouched | Outside the fire’s damage footprint entirely | Admitted-market insurance still obtainable in many cases | Pulling the reported median upward; a compositional shift in what’s selling, not organic appreciation, drives much of this | Move-up buyers, out-of-area buyers priced out elsewhere |

Find the zone for a specific address first, then read the price-behavior column: that single step resolves most of the confusion a townwide average creates.

How long before a destroyed Altadena lot becomes a normal purchase? Realistically 2 to 2.5 years from the fire date for an owner who already has financing and a contractor lined up, the fire-to-move-in range reported for full custom rebuilds in Altadena. As of early 2026 fewer than 20% of destroyed homes had received a rebuilding permit, so a Zone A lot bought today is still a longer-horizon bet, not a quick flip.

What the Fire Changed, With Sources

The fire started the evening of January 7, 2025, and was fully contained January 31, 2025, after burning 14,021 acres and destroying 9,414 structures, with 1,074 more damaged and 19 confirmed fatalities, per Los Angeles County’s anniversary fact sheet. That county source is worth naming because at least one widely circulated Altadena seller’s guide dates the fire to January 2026, a full year off; any page still carrying that date should be treated with caution.

Insurance is the second lasting change. The statewide FAIR Plan base premium for an average dwelling runs $3,000 to $3,200 a year, and a $1 million dwelling in a foothill county commonly lands at $5,000 to $9,000. A Difference in Conditions wrap, which most mortgages require because the FAIR Plan alone doesn’t cover water damage, theft, or liability, adds another 25% to 60% on top. The FAIR Plan’s own book of business grew to 668,609 policies statewide by the end of 2025, and a 35.8% average rate increase filed in October 2025 is pending an April 2026 effective date. None of this is unique to burned lots: it applies to every Altadena property the admitted market has declined to write, including many that never caught fire.

Rebuild permitting moved faster than most disasters this size but slower than displaced families hoped. Altadena logged 405 permits in the first month after the fire, 562 in the second, 750 in the third, and peaked at 1,954 permits in October 2025, about five times the town’s 382-per-month pre-fire baseline, with $2.78 billion in permitted construction value across 13 months. Homeowners can get in-person help at the Altadena One-Stop Permit Center, 464 W Woodbury Rd, Suite 210, which combines Regional Planning, Building and Safety, and Fire Department staff under one roof specifically for fire-rebuild applications.

Why do FAIR Plan premiums keep climbing even for homes the fire never reached? The FAIR Plan prices risk across its entire statewide pool of high-hazard properties, not by individual address, so a rate filing moves every policyholder in the pool together. The pending 35.8% increase is a pool-wide filing, not a penalty tied to any one home’s claims history.

Buying in Altadena in 2026

A buyer’s due diligence list here differs from a normal California purchase in a few concrete ways:

- Confirm the zone first. Pull the fire perimeter and damage-inspection status for the specific parcel before comparing it to any listing agent’s price opinion.

- Get an insurance quote before writing an offer, not after opening escrow. In Zone B especially, a stale or missing quote is the detail that most often unravels financing late in the process.

- Ask what “like-for-like” status the rebuild carries, if buying a Zone A lot with existing plans: modifications that stay within 10% or 200 square feet of the original structure move through a faster review path than a redesign.

- Check unpermitted-work disclosures against the county’s post-fire inspection records, since older Altadena housing stock often carries plumbing, electrical, or foundation work done without permits long before the fire.

- Verify oak-tree and historic-resource overlays before assuming a lot is buildable as pictured; LA County treats both as protected in parts of Altadena.

Insurance Before You Offer

A standard mortgage requires proof of adequate coverage before closing, and admitted carriers have pulled back across the foothills, so most Zone A and Zone B purchases end up financed against a FAIR Plan plus DIC package rather than a conventional HO-3 policy. Shop that combination early: a broker quote can take days to return, and lenders won’t clear to close without it in hand.

Which Loan Types Get Complicated Here

The complication isn’t the loan program so much as the lead time it adds. Build extra time into any offer with a financing contingency, since the lender’s own clearance step, not the loan type, is what stalls Zone A and Zone B closings.

Can I still get a standard mortgage on a fire-adjacent Altadena home, and does the loan type matter? Usually yes on conventional, FHA, or VA financing alike; what matters more is that the lender will withhold clear-to-close until a FAIR Plan plus DIC package, or an equivalent comprehensive policy, is fully documented, since the FAIR Plan by itself doesn’t satisfy standard mortgage insurance covenants.

Selling in Altadena in 2026

Selling in any of the three zones starts with the same disclosure package every California wildfire-adjacent sale requires: the Natural Hazard Disclosure statement, Very High Fire Hazard Severity Zone status, and any unpermitted work the county’s post-fire inspections surfaced. Price against the zone table above, not a townwide average. Sellers of standing Zone B homes should expect buyers to ask for a current insurance quote before writing an offer, since that is usually the first thing to fall through in escrow.

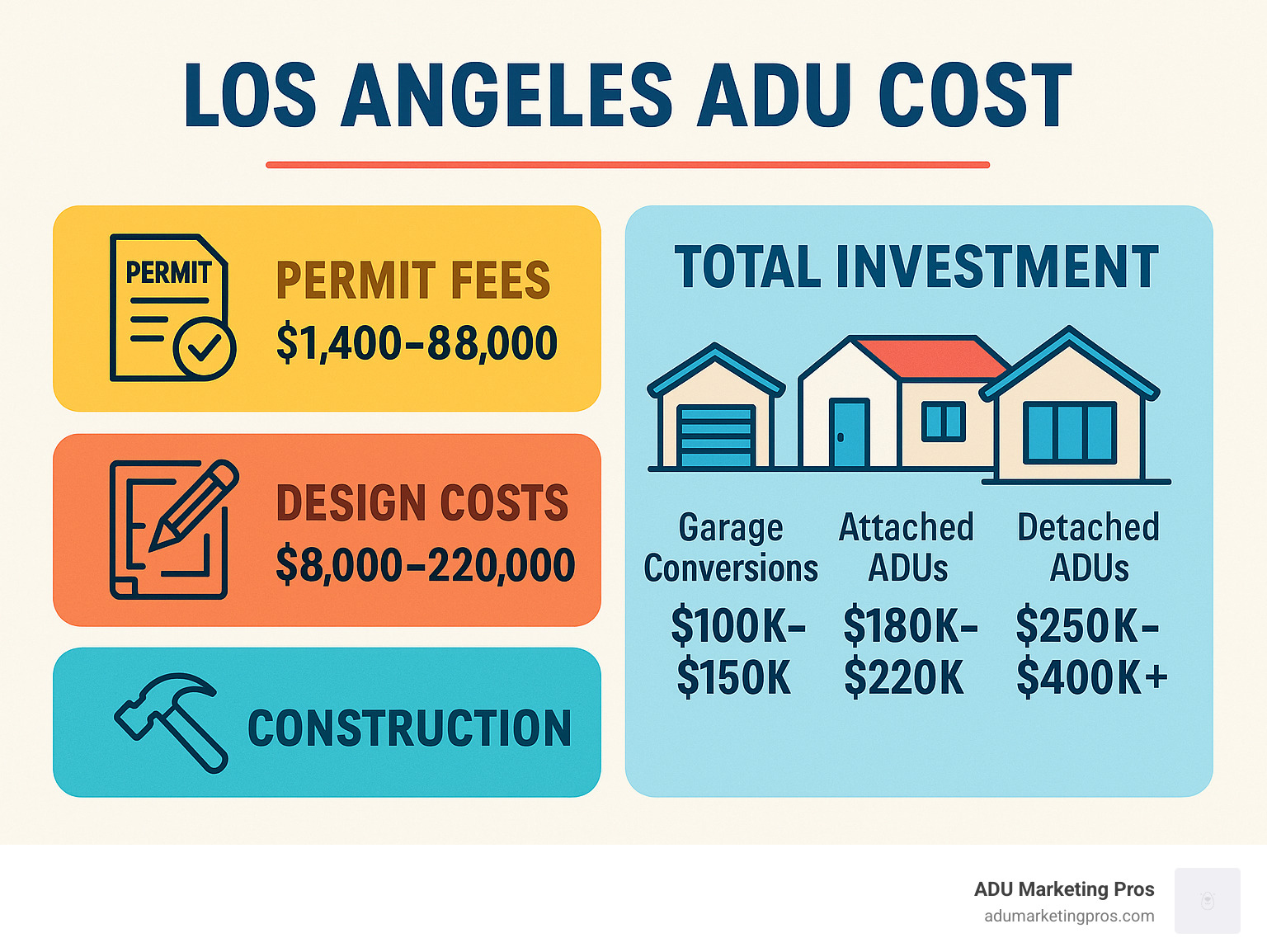

Investing in Altadena: ADUs, SB9, and Rental Economics

Two paths dominate investor interest here: adding a rental unit to an existing lot, and splitting a lot under SB9. Both are more constrained in Altadena than generic statewide guides suggest.

ADU Rental Math

Altadena-specific ADU construction commonly runs $160,000 to $350,000 or more, tracking the town’s broader $400 to $600 per square foot rebuild-grade construction costs, up to $800 or more on hillside or custom sites. On the income side, the federal government’s FY2026 Fair Market Rent benchmark for a one-bedroom sits near $1,578 a month across the 50 largest metros.

| Lot size band | Feasible ADU size | Estimated build cost | Estimated monthly rent | Rough payback horizon |

|---|---|---|---|---|

| Standard suburban lot (6,000 to 8,000 sq ft) | Up to 800 sq ft | $160,000 to $280,000 | $1,600 to $2,200 | 7 to 12 years, gross rent to cost |

| Larger foothill lot (10,000+ sq ft) | Up to 1,200 sq ft, the state maximum | $280,000 to $350,000+ | $2,200 to $3,000 | 9 to 13 years, longer on hillside sites |

| Cleared Zone A lot, ADU added to the rebuild | Up to 1,200 sq ft | Added to the primary rebuild’s $400 to $600/sq ft baseline | $1,800 to $2,600 | Tied to the primary rebuild’s completion date |

These figures are gross rent against build cost only, with vacancy, maintenance, insurance, and management left out.

SB9 Lot-Split Eligibility

Los Angeles County’s SB9 program allows up to two units on a single-family lot and an urban lot split into two parcels of at least 1,200 square feet each, in a roughly 40/60 division. The restriction that matters most in Altadena: the law applies only to areas with minimal environmental and hazard conditions, and the county names fire explicitly as a disqualifying constraint alongside coastal and wetland zones. A hillside Altadena parcel inside a high-hazard zone may not qualify without a case-by-case check; a flatter, lower-hazard block has a better chance. Confirm this with LA County Planning before any purchase decision leans on SB9 upside.

Can I use SB9 to split my Altadena lot even though it’s zoned single-family? Single-family zoning is exactly what SB9 targets, so zoning alone isn’t the obstacle; the county’s fire-hazard exclusion is. A lot inside a Very High Fire Hazard Severity Zone, which covers a meaningful share of hillside Altadena, may be ineligible without a case-by-case review, so confirm status with LA County Planning before assuming the upside.

Choosing an Agent for a Fire-Affected Market

“Hire a good local agent” names no criteria. In a fire-divided market, ask instead:

- Has this agent closed a Zone A land sale, not just a standing-home sale, in the last 12 months?

- Can they produce a zone-specific comparable set, rather than a townwide CMA that blends all three zones together?

- Do they have a working relationship with a broker who places FAIR Plan and DIC coverage, so a buyer isn’t starting insurance shopping from zero mid-escrow?

- Are they current on LA County’s like-for-like and Community Standards District rules, if the listing is a Zone A lot with existing plans attached?

What the “Median Price” Headlines Don’t Tell You

Four independent readings of “the median home price in Altadena” currently disagree with each other by more than $200,000 and, in two cases, disagree on direction entirely.

| Source | Reported median | Period | YoY direction |

|---|---|---|---|

| Redfin (city-level) | $1,341,697 | 3-month trailing, May 2026 | +63.6% |

| Redfin (ZIP 91001 cut) | $1,100,000 | December 2025 | −15.8% |

| Zillow (ZHVI) | $1,165,712 | as of May 2026 | −3.8% |

| Homes.com | $1,285,000 | trailing 12 months | −2% |

Two cuts from the same provider, city-level versus ZIP-level, disagree by roughly $240,000 and point in opposite directions. That gap is the clearest evidence that the market’s geography, not its trend line, decides which number is right for a given buyer. A compositional shift explains most of it: more of what’s selling right now sits in untouched Zone C, which pulls a blended median upward even while individual properties in Zone B are trading at a real discount.

Is Altadena’s median home price higher or lower than a year ago? Both, depending on the source: Redfin’s citywide cut says up 63.6%, its ZIP-level cut says down 15.8%, and Zillow says down 3.8%. None of these is wrong; they’re measuring different slices of a market that changed composition, not just price, after the fire.

Leave a Reply